There was another entry into the academic statistical war that makes up the debate between whether asset allocation or stock selection is more important from ReSolve Asset Management earlier this year.

Warning: I’m clearly talking my own book on this one. We run both asset allocation and stock selection, and so I am extremely amenable to ReSolve’s arguments. ReSolve are also talking their own book.

The full paper is technical, full of principal component analysis and the discussion of the appropriate correlations to use both within and between markets (if that sort of thing appeals to you, click here ), but the broad lessons ring true for me.

- All else being equal, an investor with more diverse investment choices should outperform an investor with fewer choices. i.e. Don’t just buy shares, especially not in just one country.

- When you dig into individual markets, the stocks are often very correlated with each other and so don’t provide much diversification. i.e. Don’t just buy shares, especially not in just one country.

- When correlations change, such as periods of market stress, asset allocation becomes even more important. i.e. Don’t just buy shares, especially not in just one country.

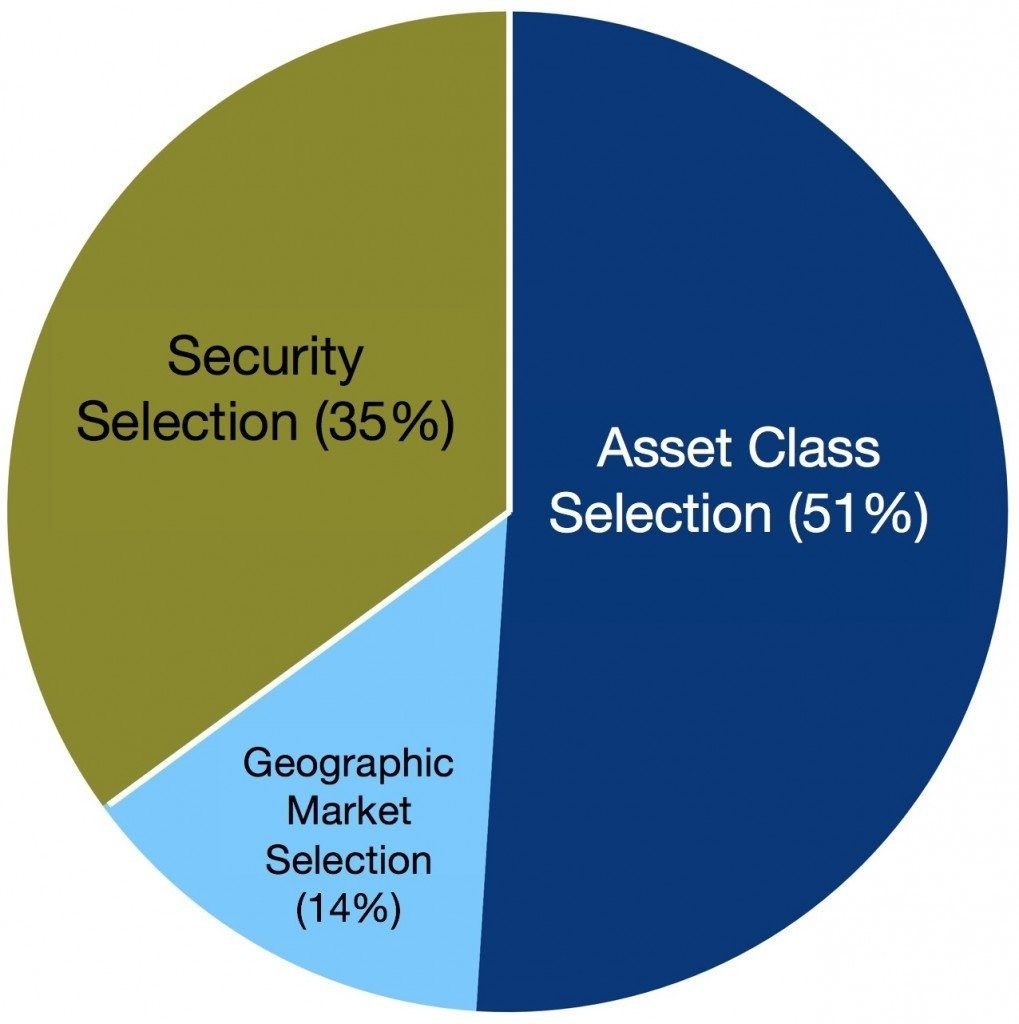

ReSolve generally extend on a paper by Staub and Singer that has the following chart as to the relative importance:

Some key quotes:

How might one interpret this analysis? The broadest interpretation is that when you choose a stock for investment you are actually making several choices at once. You are choosing:

- To invest in capital markets in general;

- To invest in stocks as an asset class instead of bonds; and,

- To invest in stocks in a certain country or region

These are all choices related to asset allocation. Moreover, the three implied decisions above are likely to have a much larger impact on portfolio outcomes than your choice of specific stock. In fact, they explain about 65% of what happens to your portfolio under normal conditions. As such, it doesn’t really matter which stocks you choose if:

- It is a poor time to invest in capital markets in general (i.e. during extremely volatile crisis periods);

- If it is a poor time to invest in stocks vs. bonds; or,

- If it is a poor time to invest in a particular country or regions.

If asset allocation choices have a more meaningful impact on portfolio results than one’s choice of individual securities, where should an investor spend his time to produce better results? Obviously, investors would be better off focusing on asset allocation.

…

Lastly, we highlight the proportional breadth during periods of market stress like 2008, when pair- wise stock correlations have historically converged towards 1 … You can see that at such times of market stress the active asset allocation opportunity may dominate security selection by almost a factor of 4 to 1.

…

In The Usual Suspects, Verbal Kint made the case that global criminal mastermind Keyser Söze had pulled a great trick by convincing the world that he didn’t exist. It seems the asset management industry has pulled a great trick of their own: they’ve convinced millions of investors for many decades to focus on the domain of investing with the least impact on long-term results. That is, investors have been overwhelmingly convinced to focus on stock selection for active returns and ignore the more meaningful opportunities in active asset allocation.

Damien Klassen is Head of Investments at Nucleus Wealth. The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.