A Fast Guide to Ethical Investing & Negative Screening in Australia

Ethical investing has a noise problem.

Give yourself the freedom to invest

like a pro.

Go beyond standard funds with a portfolio designed to match your principles. We combine the low costs of passive investing with the flexibility of active management, giving you full control over where your money goes and how it grows.

With detailed breakdowns of investment & trading fees, platform costs and no hidden layers, remove the ambiguity that costs investors thousands over time.

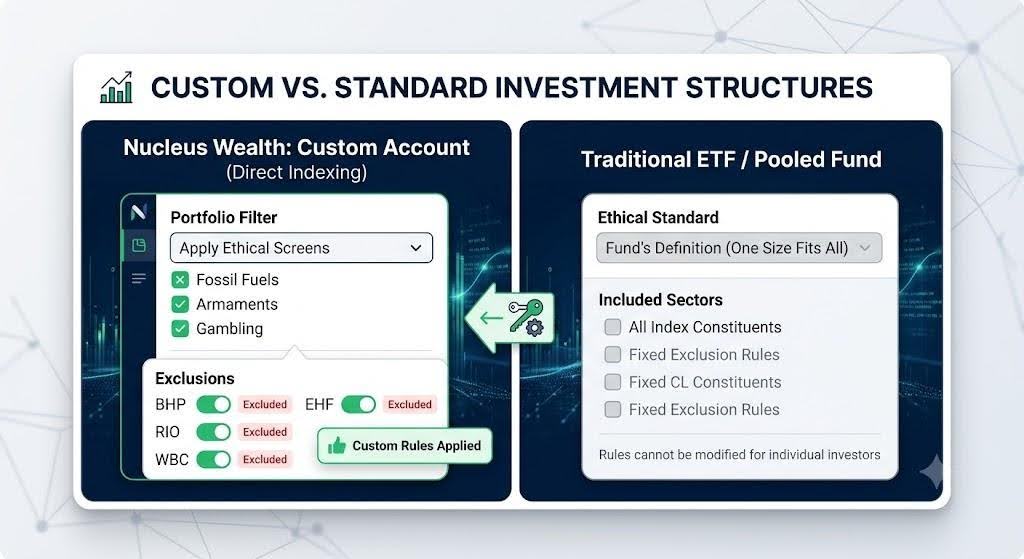

We provide a wealth management solution tailored to your goals and preferences, offering both active and passive investment portfolios.

Invest only in high quality securities to reduce risk. Your investment will only hold blue chip international and Australian shares, cash and government bonds.

Our assets are held by trusted, independent providers—Interactive Brokers, Praemium, and DASH—safeguarded by global custodians including J.P. Morgan, HSBC, Deutsche Borse AG/Clearstream and Macquarie Bank.

PROFESSIONAL SERVICES

75+ years of combined

financial expertise

Our investment team believes everyone deserves transparent, customised access to high-quality investment management, not just high-net-worth investors. By leveraging technology and partnering with leading global professionals, the team focuses on controlling costs and delivering superior investment outcomes for you.

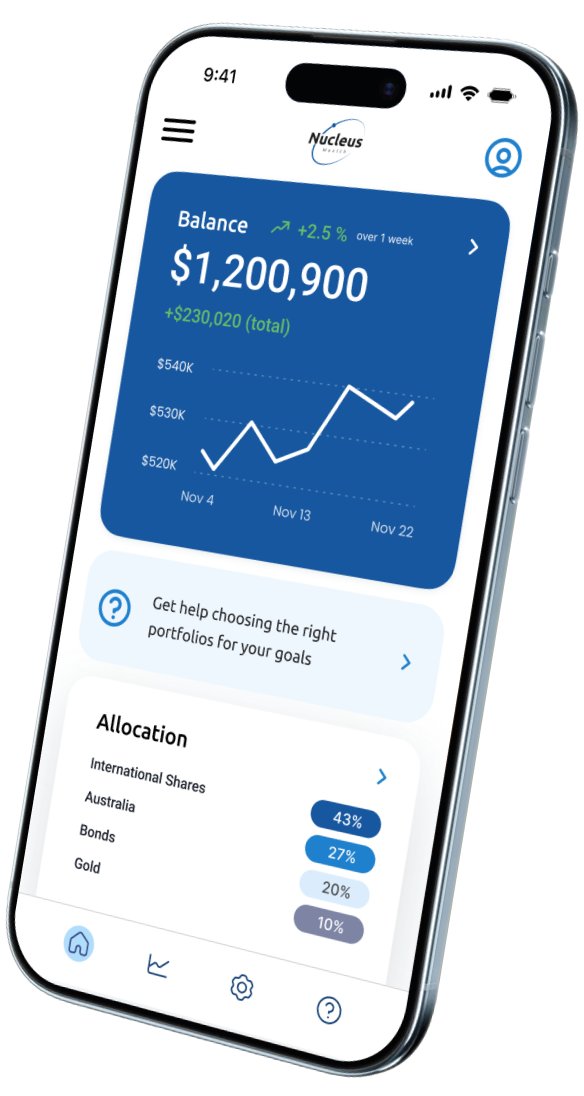

Build a portfolio that reflects your principles and life goals in just minutes.

Create your account

Create your accountRegister your account on our platform in less than 15 minutes.

Fund your account

Fund your accountAdd money to your account via bank transfer to get your investment journey started.

Personalise

PersonaliseExplore screens and tilts, or select between passive or active investment. The platform is yours to explore and modify.

Get weekly insights and practical strategies from the Nucleus Wealth team delivered straight to your inbox.

.jpg)