Chasing Unicorns

Snapchat is listing shortly, probably early March. It's a unicorn, a start-up with a valuation over $1b.

It's going to be valued at lots (USD25b?), and it loses money, which makes it hard to value. In the end, it's a lottery ticket.

Late last year there was a research paper out suggesting that the investment return on stocks like this are not that different from lottery tickets:

Predicted stock issuers (PSIs) are firms with expected “high-investment and low-profit” (HILP) profiles that earn unusually low returns. Over a 36-year period (1978-2013), average returns to top-decile PSIs are indistinguishable from Treasury yields. We show these firms have lottery-like payoffs, high volatility, and high Beta. They are cash-strapped and most will need additional financing. Top-PSIs generate future average return-on-assets of -30% per year, report disappointing earnings, and experience strongly-negative analyst forecast revisions. They earn especially low returns in down markets, and are nine times more likely to delist for performance reasons than bottom-PSIs. We conclude that top-PSIs, and HILP firms in general, earn low returns because they are more salient (i.e., sexier) to investors and thus overpriced, not because they are safer.

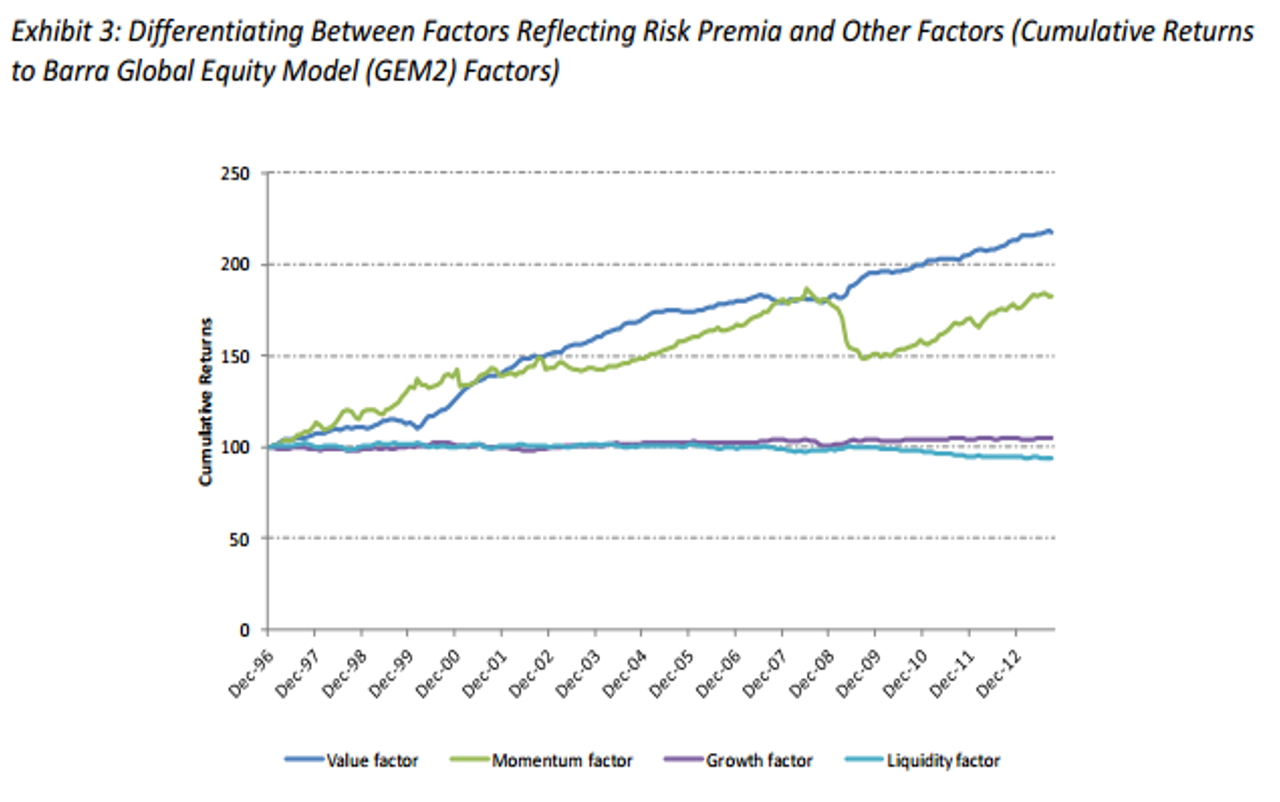

This conforms with my view - and matches the traditional "quant" view - that growth stocks as a group are not outperformers:

Growth Stocks underperform

Growth Stocks underperform

Keep in mind that this group of stocks includes a bunch of fantastic performers. Tesla, Apple, Google - all of these stocks are massive and increased 10x or more over this period. So, for growth stocks generally, you get a few massive winners and a bunch of losers. Many of the stocks do grow sales (and sometimes even earnings). The problem is that investors overpay.

“I love company X, I love its main product, company X is growing sales at 40% per annum, company X is growing profits at 20% per annum, therefore buy the stock”

The above quote is a compelling story for most investors, but the story is missing the key ingredient… price. The company X may be great at $1 per share, fine at $10 per share, but is it still a buy at a $100 per share, and how about at $1,000,000 per share?

I like to use the heady days of the internet boom as context. Investors knew that search was big. Very big. Probably the most important thing. Yahoo, Lycos, Alta Vista, Excite, Ask Jeeves all had nosebleed valuations as investors knew that the winner of internet search would grow to be worth a fortune.

Investors were right. Search was huge.

Only it’s just that the actual winner – Google (now Alphabet Inc.), wasn’t even listed. Didn’t list until 3-4 years after the boom had finished.

The truth is that for every growth stock that justifies its price, there are another 5 or 10 that don’t.

If you are using the market as a “get rich quick scheme” then you want to invest in growth stocks. I hope it works out for you. For most people it doesn’t.

So, will Snapchat succeed? Maybe. I'm not going to say that it won't succeed. But I will say that the odds are against it.

If you want to get rich (or poor) quickly then Snapchat is the type of stock you should buy. I'm more concerned about getting rich steadily, and so am looking elsewhere.