Global earnings rocket

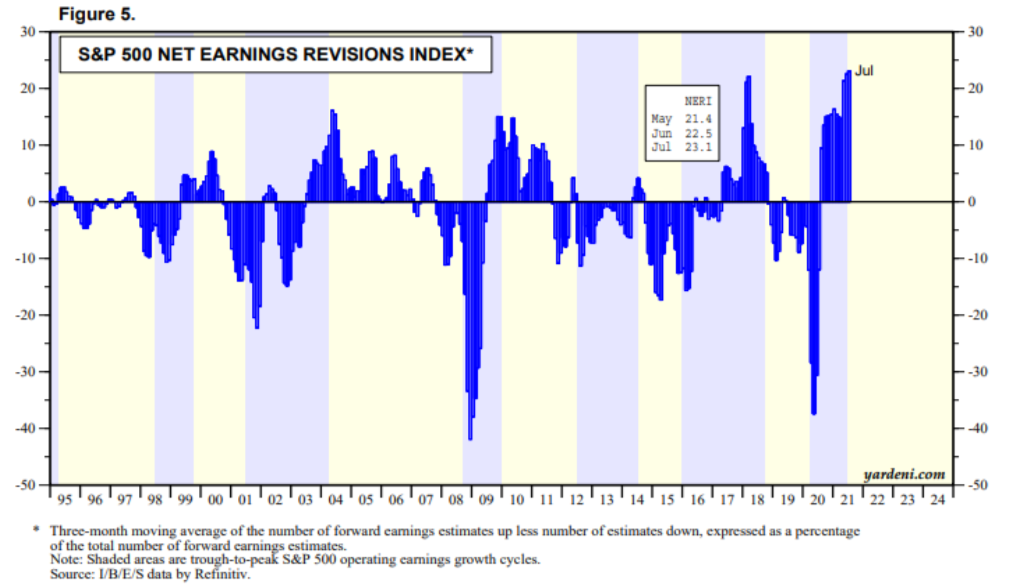

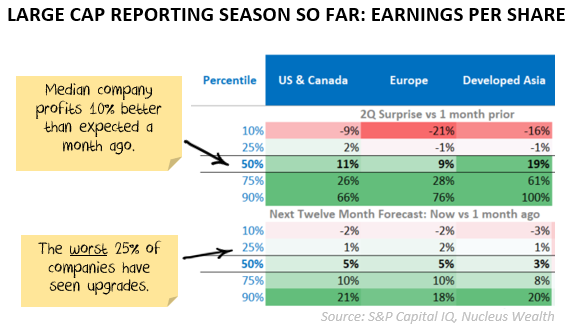

Most of the global reporting season is over before the Australian reporting season has begun. It has been a cracking reporting season; upgrades are running as high as they ever have for US large-cap stocks:

As many of you know, I'm tracking two potential scenarios:

-

- Stock markets grind higher on the back of improving earnings and fiscal support

- A growth "hole" emerges and stock markets fall until more support is provided

Paradoxically, both scenarios received more support over the last few weeks. Conditions in China have continued to deteriorate, and there are reasonable signs of easing growth elsewhere, supporting the second scenario.

But, in this post, I want to focus more on the first, and highlight how strong the reporting season has been.

Earnings are strong, regardless of which way you look

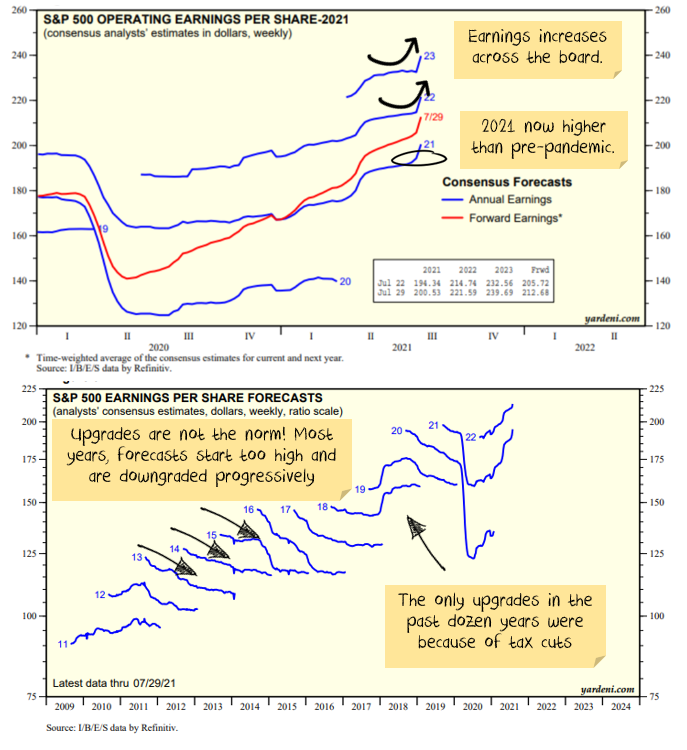

Earnings for future years are being revised upwards across the board:

It is not just the US. The same trends are in place around the (developed) world. Also, it isn't just a few big stocks, the median stock has seen 10% upgrades to 12m forward earnings over the last 30 days:

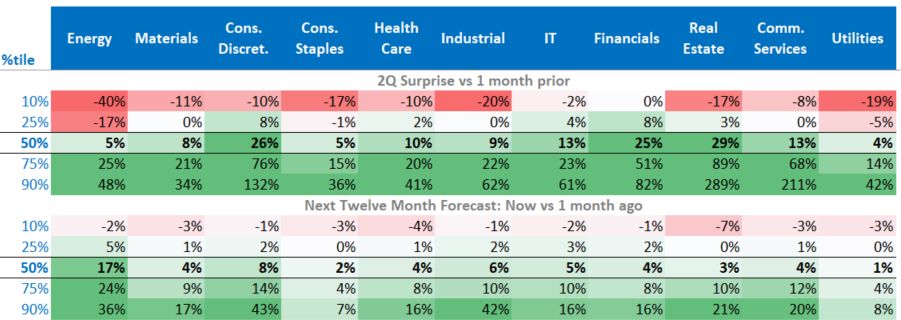

Breaking it down by sector, and it is largely the same story. Utilities and Consumer Staples have been the worst, but only because every other sector has been so good.

Stock stories

Finally, some stock anecdotes I found interesting:

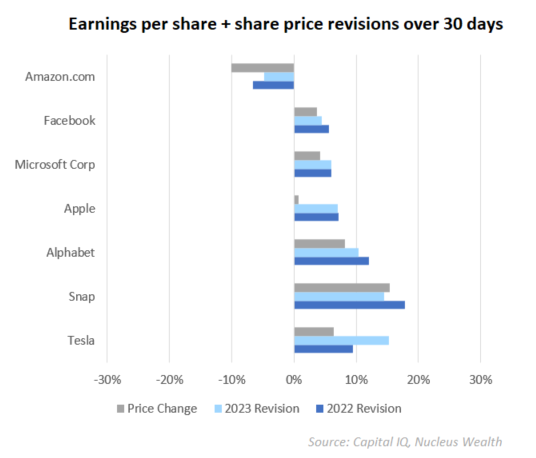

FAANGs+ continue to impress

More earnings results for the market darlings, more upgrades. Except Amazon:

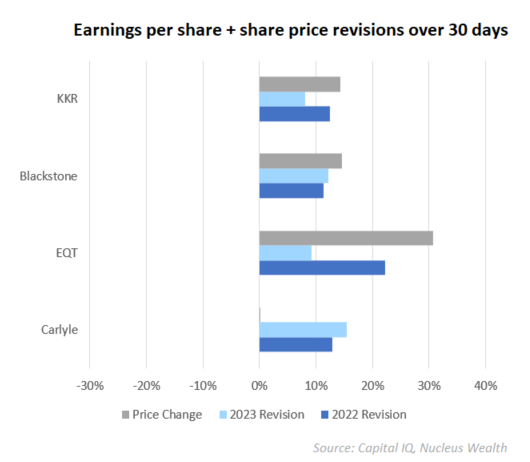

Private Equity - its a boom

When every asset is expensive, and interest rates are low, it pays to be operating a business that loves leverage:

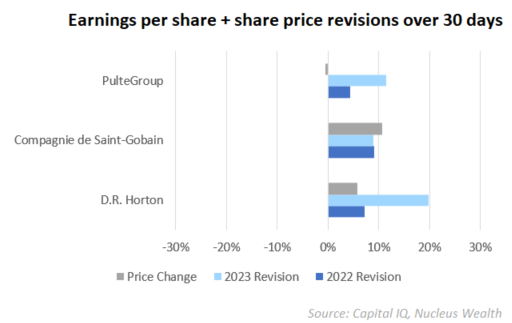

Global housing frenzy - profit expectations still rising

Some of the house building leading indicators have looked like they might be topping recently. Not the stocks. Earnings upgrades continued to flow, even into 2022:

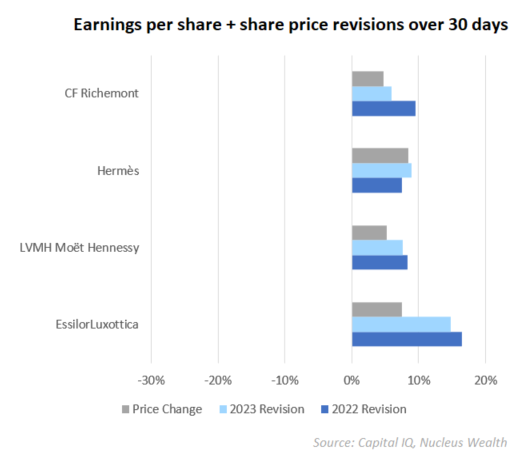

Inequality is going nowhere

Luxury good earnings looking strong:

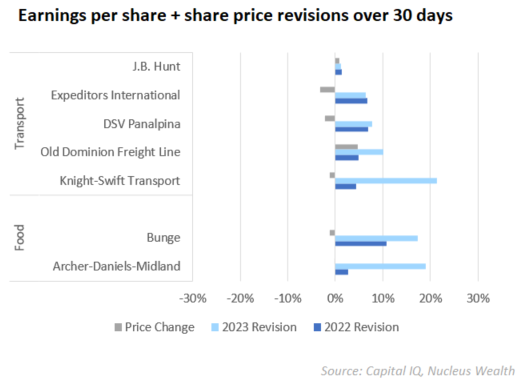

Inflation. Really?

Consumer staples stocks in particular complained about inflation. Some quotes:

"It's pulp, it's paper, it's anything involving oil. Plastic packaging is going up. Trucking costs have gone up significantly. Ocean freight has gone up significantly. You are seeing it in a wide range of cost areas… It's inevitable we will see an increase in inflation. How much? I don't know." -David Taylor, chief executive of Procter & Gamble

Unilever Finance chief Graeme Pitkethly said that since the company issued its guidance in the first quarter, crude oil prices had risen 12%, soy bean oil 21%; while freight and transportation costs had risen and 4% and 7%, respectively.

"We are facing significantly higher input costs and a reversal in consumer tissue volumes from record growth in the year ago period," warned Kimberly Clark CEO Mike Hsu.

My thoughts on inflation being transient and it being an inventory supercycle are well documented. The above comments suggest I might be wrong. The below charts suggest that I'm right:

Basically, you have food and transport companies telling customers: "sorry mate, got to put up prices, all that inflation". At the same time, they urge investors to upgrade earnings as fast as possible. Something doesn't match.

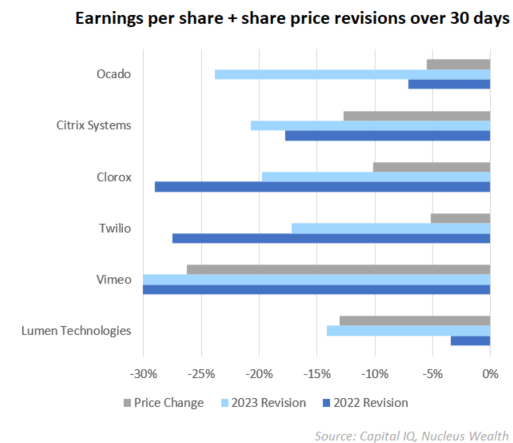

Analyst's got too far in front of the facts

A range of lockdown heroes came back to earth. Ocado (online groceries), Clorox (household disinfectants), Vimeo (online videos) and a range of cloud computing stocks had earnings forecasts slashed:

Clearly, the story got too far in front of reality.

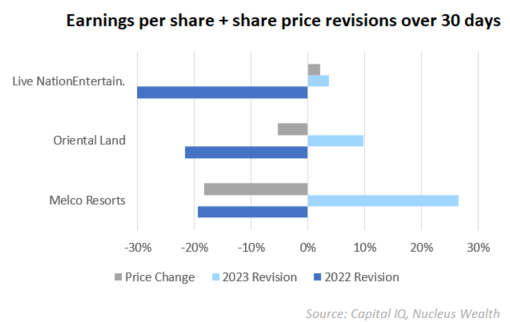

Just wait until next year!

Reopening stocks like Live NationEntertainment (entertainment ticketing), Oriental Land (Tokyo Disney) and Melco Resorts (gaming/hotels) ended up in the "not yet" category:

Earnings downgraded for 2021 markedly, but then sizeable upgrades to 2022. Usually, I treat the mix of near term downgrades and later year upgrades with a healthy amount of cynicism. But this time, I really want to believe...

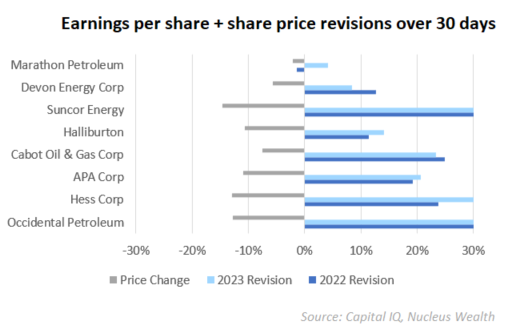

Energy stock earnings diverge from prices

Energy earnings boomed and there were meaningful upgrades to both 2021 and 2022 earnings. But prices declined:

The energy sector also has the highest proportion of analyst buy recommendations. So, the market telling the energy analysts that the market does not believe the earnings or the recommendations... have a look at David's commodity price crash piece from last week for a macro view of the sector.

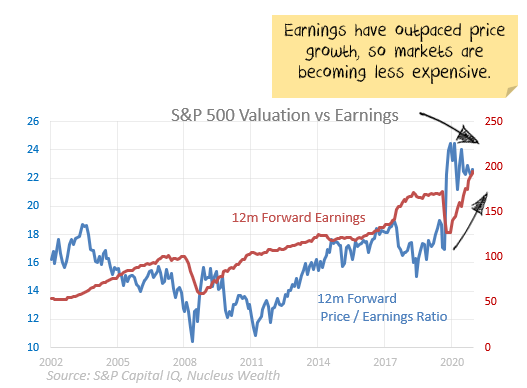

Net Effect

Despite the rapid rise in share prices, the US market has actually become cheaper as earnings increases have outpaced prices rises:

Markets are still not cheap, and there are genuine concerns about the growth slowing. But, it is hard not to be impressed by earnings.

.jpg)