Richard Bookstaber recently put out an interesting post on sectors that he thought had problems on a 30-40 year view. Richard is the author of a number of good finance books - I liked A Demon of Our Own Design: Markets, Hedge Funds, and the Perils of Financial Innovation![]() and I have his new one The End of Theory: Financial Crises, the Failure of Economics, and the Sweep of Human Interaction

and I have his new one The End of Theory: Financial Crises, the Failure of Economics, and the Sweep of Human Interaction![]() on my reading list.

on my reading list.

Besides writing books with extremely long titles, he also works for a pension fund, and so likes to talk about very long-term outlooks and risks - see here for his full post, below is an abridged version with my comments:

General propositions

The key drivers of what to short are developments in the following areas:

- Increased reliability of products. Already, many of the things we consume are more reliable and last longer than any time in the past. Take computers and LED screens. And soon, it will be electric cars.

- Less consumption of goods. In the sense that most of our time is spent on fewer things – like those highly reliable computer items.

- More commodity items. Which means less demand for advertising. Compare advertisements today with those of a generation or two ago. Almost everything was driven by brands. Now we are not as focused on brands, and as far as brands go, there are so many brands that are hard to differentiate that they may as well be commodities.

- Meanwhile luxury goods are moving toward items that are inherently scarce, like art and real estate -- items that do not require production.

- More efficient production. And part of that efficiency is that what we produce requires less labor

- Increased demand for personal space and privacy. We will circle the wagons around our personal space and privacy. We are going to draw the line when we find that companies know more about us than we know about ourselves.

I think the reliability is generally right, but I would also counter that given the low cost of production that fewer and fewer things are worth fixing. Loose screw in your toaster? Just get a new one. I suspect in 30-40 years time this logic will apply to a wider and wider range of goods.

I hope he is right about more commodity items meaning a lower demand for advertising... although the electricity market in Australia would suggest the opposite. Are you selling exactly the same product as all your competitors? Better spend more money than them on advertising/sowing confusion then.

I disagree on the brands. I actually have the opposite view - people (unfortunately) like to impress other people with showings of wealth. I think driverless cars will lead to fewer people will owning cars. So, if I don't own a Ferrari because everyone uses driverless Google taxis, and anyone with a full-time job can own the latest iPhone, how will I be able to convince everyone how successful and cool I am? Luxury brands.

Increased demand for personal space and privacy. If when he says "we" he means baby boomers then I think he is right. I'm not so sure this applies to Gen Y or younger. Most don't seem to care.

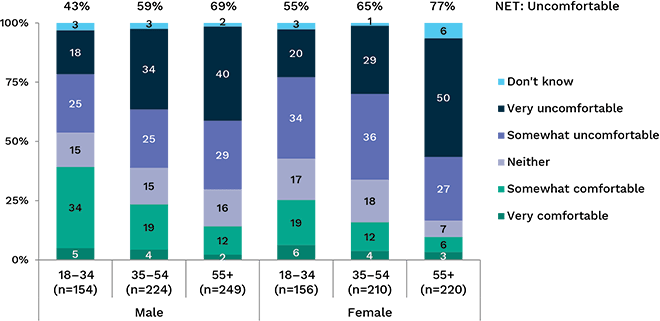

Level of comfort with search engines and social media sites targeting advertising based on online behaviour

Source: Australian Community Attitudes to Privacy Survey 2017

Source: Australian Community Attitudes to Privacy Survey 2017

Let's start with the easy ones, where there is a clear consensus, and work our way down from there:

Energy

Oil. We all know that fossil fuel is a goner. And the more obvious it becomes that oil remaining in the ground will be a stranded asset, the more oil will be pumped out in the shorter term. So between growing renewables, flowing oil, and more efficient technologies, energy will be abundant.

Will the oil jobs be replaced by renewables. Is it only a matter of retraining of those working in this sector to work with renewables? No, because even ignoring the higher economies in production, the capital plant of renewables lasts a lot longer and requires less maintenance per kilowatt-hour produced.

Yep - preaching to the converted on this one.

Transportation

Trucking. Trucking will also clearly be altered from an employment standpoint by self-driving vehicles. We got a taste of this a few weeks ago when Tesla unveiled its semi truck. Whether you like Tesla's odds or not, self-driving trucks are coming, especially for runs along the interstate.

Things will also change at the local level, for example for package delivery. A new household appliance, already in the works, will be a lockbox that can be opened for securely delivering packages, as ubiquitous as mailboxes. In the limit there will be one run per day of an autonomous vehicle to each residence and business. (How the packages get from the vehicle to the lockbox is the weak link in taking humans out of the loop in this scenario.)

Autos. Another no-brainer is that the automobile-related industries will be far smaller. Gas stations will disappear. And most mechanics. Cars will last far longer and require less maintenance, garages, which are already on the downswing, will largely disappear as well. (New tires from Costco.) Once production is scaled up with a few rounds of efficiency gains, electric cars are not complex, and are cheap to build. The cost of cars will be a fraction of what they are today. With low maintenance, low fuels costs, low purchase price, and autonomous driving, transportation will be far safer and less expensive.

People will be traveling less; fewer trips to the mall. People will have less need for a dedicated car because they will summon an autonomous car that can be running people one place or another nearly 24/7. And most people won't care as much about style because they will be treating them as what they are, transportation services -- which gets to my point about more commodity-like products.

Ditto - here is a webinar we recently did on this and a blog post from last year.

Casualty Insurance

It is a mixed bag; some lines will dwindle, others will grow.

Auto. Autonomous vehicles are safer than people-driven vehicles, especially when all cars are autonomous. Fewer accidents means less need for casualty insurance.

Liability. Less high-risk labor.

Property. Things will be looking up here, due to the effects of climate change.

These sound right to me.

Real Estate

Commercial. Stores will become less prominent as the efficiencies of delivery improve. And as many items last longer. This leads to issues for commercial real estate. There will be construction for warehouses and "fulfillment centers." These are cheaper to build and maintain than commercial retail space. So less construction and maintenance. With the move toward renewables, there is a drop in construction of large-scale fossil fuel plants, and the plant for renewables will not require as much construction and maintenance demand.

Residential. Demographics and lifestyle will change the demand for housing. There will be less demand for large houses with living rooms and dining rooms that are not used, and for four and five bedrooms. This means a glut for some zip codes. And it also means fewer construction jobs. Houses will have solar cells and batteries to be increasingly self-sufficient, so less energy use.

So chalk up the construction industry -- one that is more immune to technology -- as another casualty.

Commercial property I agree.

Residential I'm not so sure about. Without cars to spend money on to impress the circle of friends, I'm thinking that spending on residential housing could easily be more rather than less. The key question then is whether it all goes into land values (i.e. spending up big to get a spot on the water) or into construction quality (i.e. bigger and/or better houses). If it is land values then Richard might be right. If it is quality then he won't be. With driverless cars (and a long shot at hyperloops or flying cars) improving transport over the next 40 year, people might be able to live further away from cities, limiting land values by increasing supply. I'm not sure if he will be right or wrong on residential construction, but its not an obvious short in my book.

Basic Materials and Mining

With less demand for new cars, less construction, and key goods that are replaced less often, there will be a drop in demand for many raw materials. Though others, like those that are needed for batteries and computers, will increase in demand. Or maybe not. Who knows what raw materials will be in demand, and how great that demand will be with the changes in technology that we might see over the course of the next generations. And because these products last longer, and finally meet the needs for various functions, they will not be the same engine of production.

Construction is the key assumption here.

Advertising (and Facebook and Google)

There is a feedback loop between advertising and the information and social network companies that depends on advertising. This feedback leads to a self-destructing business model, with the information companies and advertising going down together. The information companies depend on advertising, and yet they are information engines that reduce the need for advertising.

And advertising for non-luxury and non-status goods (luxury and status goods are not the fodder of Google or Facebook) will drop for the reasons I mentioned above: less advertising because we will demand fewer goods, and many of the goods will be commodity-like. Few of us care about which chargers we buy for our phones.

I hope he is right. I strongly suspect he is wrong - companies will revert to the "confusopolies" we see in utilities and telcos where there needs to be more marketing to hide that they are selling the same product as their competitors rather than less marketing.

There are other pressures that might build for social networks such as Facebook. We will still need search engines, but Facebook is already tiresome to some of us, and we are getting the first whiffs of the toxicity at its root. With the world veering toward an impersonal dystopia, we will guard our privacy, we will circle around our real relationships. Here are recent articles from Wired that give a flavor of where things might be going, one a truly harrowing saga of overcoming malicious cyber attack, and another one of any number you can find, appearing with increasing frequency, on privatizing Facebook. From the perspective of forty years out, Facebook and social networking in general will have been a flash in the pan.

How do you stop media companies that prey on people's insecurities? Unfortunately, whether these are old school like Cleo and Cosmo or new school like Facebook, they have readers. Some of the readers even know they are being manipulated but read anyway. And companies looove to advertise to people that are insecure.

Chalk this one up as another one where I hope he is right but suspect that he is wrong.

Damien Klassen is Head of Investments at Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.