Correlation doesn't equal causation. But sometimes it does.

Is it possible the board of Qantas are Freakonomics listeners or just unwitting participants in a glass cliff experiment - Australian edition.

The ABC sets the scene (emphasis mine):

Qantas' new CEO has issued a public apology for a series of scandals that have damaged the airline's reputation, acknowledging it has been "hard to deal with" and promising to make changes to rebuild customer trust.

Vanessa Hudson took over the top job earlier this month after former CEO Alan Joyce stood down following 15 years as one of the country's highest-paid executives.

And for those unaware of the glass cliff, I'll hand over to Freakonomics. First some background:

RYAN: In November 2003, the Times in London printed an article that was looking at how women were performing in the top companies on the London Stock Exchange. And what they were saying is that companies that had more women on their boards of directors tended to be worse, in terms of their average annual share price, compared to those companies that had less, or indeed no women. And their conclusion was that women were wreaking havoc on company performance.

RYAN: And instead of looking at how many women were on their boards of directors, we looked at when women were appointed, and then also when men were appointed as well. And then we could look at the performance beforehand and afterwards.

RYAN: If the Times article was correct, we should see that after women were appointed to these boards of directors, share price should go down. But actually what we found was the opposite. What we found was when companies had been doing poorly, when their share price had been declining, they then appointed women to their boards of directors. So what we found was a really different causal problem. Rather than women wreaking havoc on company performance, what we found was when companies were doing badly, they were much more likely to appoint women. It was a very different narrative from the one that the Times was putting forward. But it also opened up more questions than it actually solved.

So, in stepped Christy Glass to research this further:

GLASS: We found that white women and people of color are significantly more likely than white men to be promoted C.E.O. to weakly performing firms.

For instance, when a firm went looking for a new C.E.O., what was their return on assets and return on equity looking like? Did Glass and Cook find — as Ryan and Haslam had found — that women are more likely to get the top job when a firm is in trouble? They sure did:

GLASS: We found that white women and people of color are significantly more likely than white men to be promoted C.E.O. to weakly performing firms.

“Weakly performing firms,” which, if the female C.E.O. didn’t turn them around, often replaced her with a man.

GLASS: We termed this the “savior effect.” In other words, the firm experimented with this nontraditional leader, perhaps trying to signal it was headed in a bold new direction, that it was aggressively going to address performance declines. And if that doesn’t happen, these leaders tend to be blamed and replaced, back to normal — bringing in the white male, typical leader to then navigate the firm out of crisis.

This isn't just limited to stocks

Other researchers began looking for evidence of the glass cliff beyond the corporate world. They found it — in education, where women were more likely to have leadership positions in failing school districts. They found it in political elections, where women are more likely to run in unwinnable contests; and in political leadership, where women are more often elevated during periods of political instability. So there’s plenty of evidence for the glass-cliff phenomenon.

Some of the experiments used a clever trick.

RYAN: We had two incredibly well-qualified candidates for the job, one man and one woman. We gave their C.V.s, and descriptions of their experience. We gave photos of them, and we’d very carefully made sure that they were absolutely equally qualified for the job. And in fact, what we had was, we had two C.V.s, and we just switched their names on them, really, for every second participant in the study. And then we said, “Okay, who do you want? In a scenario where everything is doing well, who do you want: the man or the woman? And in a scenario where things were going badly, who do you want?”

And what’d they find?

RYAN: What we found was when everything is going well — when share price was going up, or when everything is hunky-dory — they were almost 50-50 likely to choose the man or the woman. But when things were going badly — when there was crisis on the horizon, where there’d been criticism, and where there was risk involved in the leadership position — they almost exclusively chose her. So we can conclude from that there’s some sort of preference for women when all is going badly.

But Ryan does not interpret this preference as a willful sabotage of the female candidates.

The podcast goes into a lot more detail, but the guts of it is that when a company is either in trouble or about to be in trouble that appointing a female or minority is a natural reaction for boards.

I wish Vanessa Hudson all the best - Australia has a dire need for more diversity in CEO ranks. And for her sake, I hope that the Qantas board isn't running a glass cliff experiment.

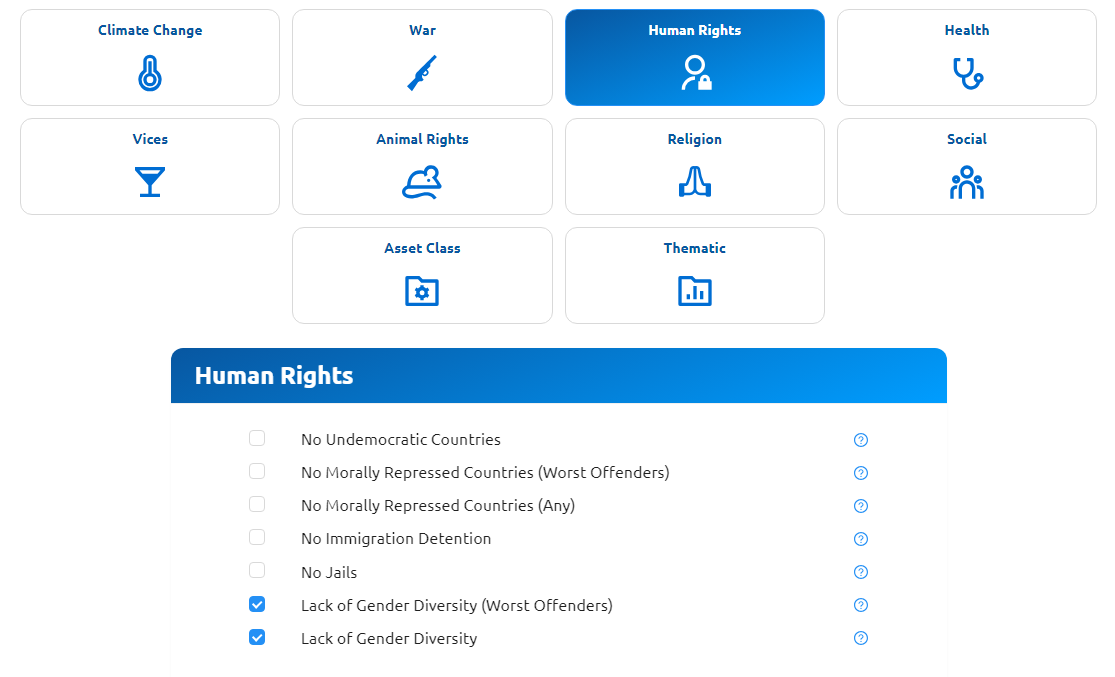

Apply gender diversity screens to your portfolio

Some consider it a risk to invest in companies with poor gender diversity. Some reasons include missing out on a vast pool of talent and potential reputational damage or legal consequences for failing to adapt to societal and regulatory pushes towards gender equality.

Numerous studies have demonstrated a positive correlation between gender diversity and financial performance, suggesting that companies with better gender diversity are more likely to be financially successful in the long run. Diverse teams have shown to be more innovative and effective, bringing a variety of perspectives that can lead to better decision-making.

There are two ways you can apply Gender Diversity Screens to your portfolio at Nucleus:

Lack of Gender Diversity (Worst Offenders): Removes companies that have less than 10% of their board or board + top 5 executives being female. Note: This will remove many Japanese stocks from your portfolio

Lack of Gender Diversity: Removes companies that have less than 20% of their board or board + top 5 executives being female. Note: This will remove many Japanese stocks from your portfolio

Damien Klassen is Head of Investments at Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.