This is a little embarrassing

Last week I published our monthly performance report. I addressed the question of when do we look to start deploying our cash & bonds back into stocks. My throwaway line was effectively "wake me up when the stock market is down 30%". Embarrassingly, we arrived at this point a little faster than I expected. From our monthly:

The decision at the end of January was relatively easy: markets at highs not seen since the tech-wreck, no earning growth, a looming supply and demand shocks, and a possible pandemic. Sell. There was no need to put an exact figure on how far markets would fall as they were clearly too expensive.

The decision this month is still easy in my view. All of the above factors have gotten worse, markets only fell a little over 10%. If you made the heroically bullish assumption that earnings will only fall 10%, then share markets can fall another 20% and still be slightly expensive. So there is no reason to buy yet.

The case for becoming bullish will depend on:

- How severe the outbreaks are in the US and Europe.

- Whether there is a corporate debt crisis.

- How significant and well targetted the fiscal stimulus is from governments, particularly the US, China and Germany.

With the drop in the US overnight, we have reached the levels I was discussing. I'm not yet ready to buy.

I'm sure some traders are willing to buy on the back a reversal. And they will probably be right. Some days.

For longer-term tactical investors, it is different. Without a resolution on the three main unknowns, I would need lower stock prices before deploying cash and bonds back into the stock market.

Unknown 1: How severe the outbreaks are in Europe and the US

It is sad. Everyone knows China was lying about the case numbers, but their actions showed the severity of the crisis. China showed the rest of the world what needed to be done and the rest of the world ignored them.

If you do not lockdown infected cities immediately, then hospitals become over-run with patients and the mortality rate will be 5x higher. And that doesn't even account for higher mortality in any other patients with different issues that can't be properly treated because the hospital system is swamped.

Northern Italy is now Wuhan. Same M.O. Same outcome.

It is not "just the flu". Who would have guessed?

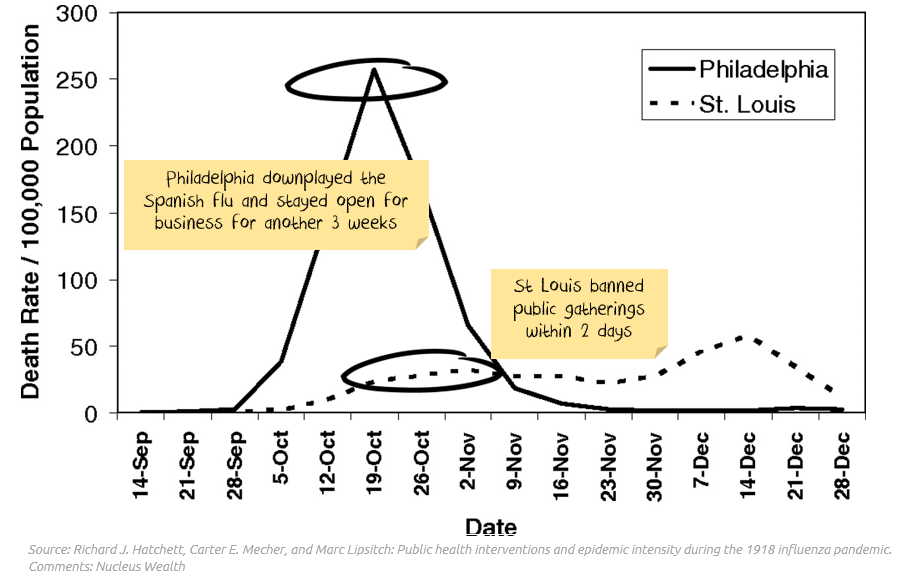

The most instructive chart comes from the Spanish Flu comparing the effect on Philadelphia with the effect on St. Loius:

Philadelphia had a parade in late September in the above chart. In an unrelated note, Melbourne planned a grand prix party in the middle of a pandemic. Inviting everyone from infected countries to visit. Why does it look like it will take a team revolt to cancel the grand prix?

The US healthcare system and its incentives are probably the worst in the developed world for dealing with a pandemic.

There is no resolution on this front yet.

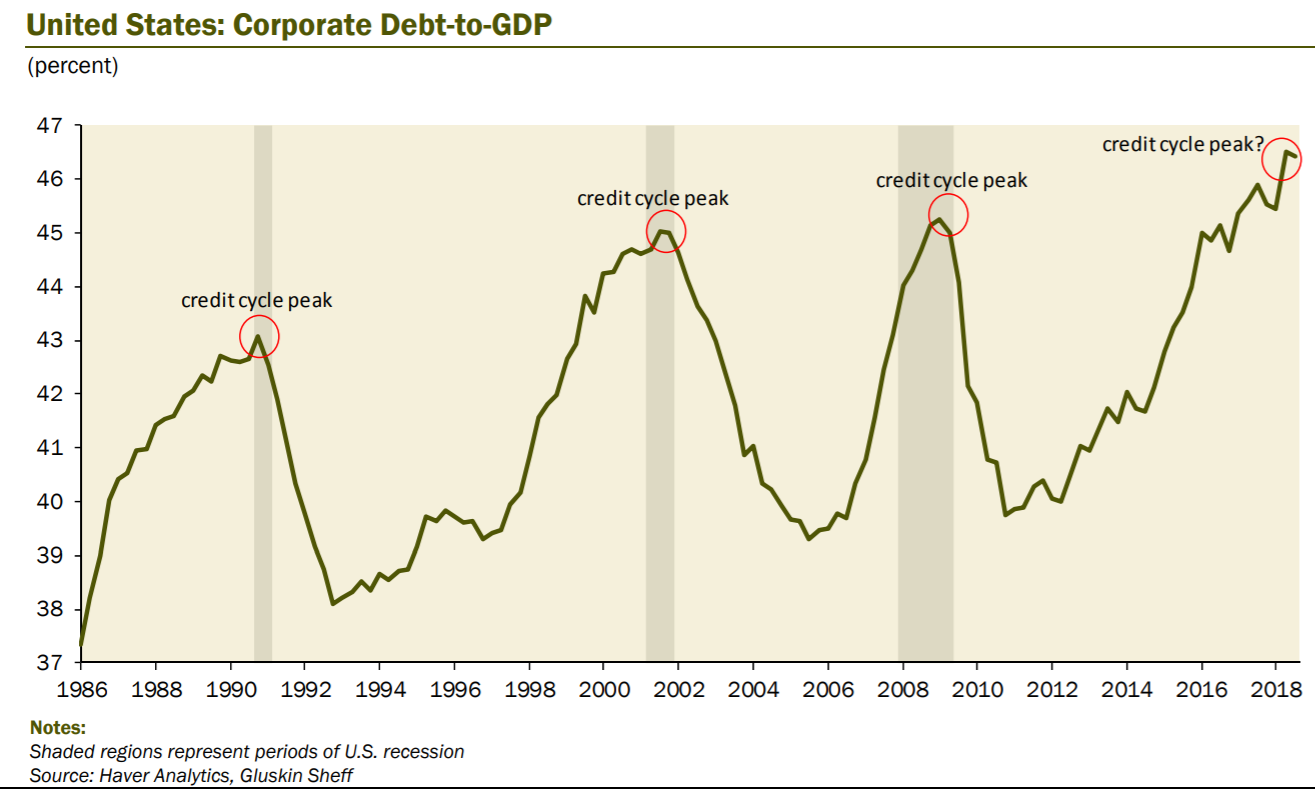

Unknown 2: Whether there will be a corporate debt crisis

Yes. It looks like there will be. At the moment, debt markets are welded shut like the door of a Wuhan apartment building.

Central banks and governments will need to pry debt markets back open in the coming days if we are to avoid a depression. I expect they will, but it is going to mean tearing up the traditional rulebook and some truly unconventional monetary policy.

But this debt cycle is over. There is no putting that genie back into the bottle:

Unknown 3: How significant and well targetted the fiscal stimulus will be

I can't believe the coverage this has gotten in Australia. I think the press... likes it?

My initial thought:

I'm not sure what else I need to say. The whole idea of the stimulus package should have been two-fold: (1) incentivise people to stay home to reduce the spread of the virus and (2) support the economy AFTER the threat has passed.

Australia has it ass-backwards. We seem to be encouraging our poor and elderly to get out of their houses and either catch or spread the disease. Then, by the time we are through, and the economy will need support to get going again, the stimulus ends.

A quick aside. Italy and the UK have implemented support for mortgage holders. I have no doubt our housing obsessed polity is licking its lips for more of the same here. Once again, that would be extremely poorly targetted. Most mortgage holders are fulltime, many can work from home. Those who can't work from home and casuals are far more likely to be renting. So, mortgage support would be great policy to target Lib voters, but shocking policy to actually help keep a quarantine intact. With that ringing endorsement, you can probably expect it to Australia.

We are still waiting on the US.

The Upshot

Expect a global recession.

Expect central banks to step in imminently to arrest rising bond yields.

Expect action on the corporate debt markets to prevent disaster.

Expect governments to stumble onto the right policy after all other options have been exhausted.

Wait for clarity before deploying cash.

.jpg)