Ethical investing is frankly confusing. There are plenty of good products, but also a number of products whose promoters may not be as ethical as the stocks they invest in...

For me, there are three key issues:

Some Definitions

Ethical investing is often termed ESG: Environmental, Social and Governance.

Investopedia defines this as:

Environmental criteria looks at how a company performs as a steward of the natural environment. Social criteria examines how a company manages relationships with its employees, suppliers, customers and the communities where it operates. Governance deals with a company’s leadership, executive pay, audits and internal controls, and shareholder rights.

This is a pretty common framework, and I'll use it to look at the key issues.

This part is the confusing part. How much investment performance do you give up by being ethical?

Unfortunately, there are plenty of media outlets prepared to muddy the waters in (probably) well-intended ignorance. For example, Canstar published the following:

Do responsible investment funds perform as well?

Yes, and in fact, they often perform better. According to the 2016 update from Responsible Investment Association Australasia (RIAA), responsible investment funds outperformed other funds in the following categories over the following investment timeframes:

This is wrong.

It is absolutely possible for ethical funds to perform better, but if you thinking of investing in ethical funds so that you can outperform the rest of the market I suggest you look elsewhere.

There are 1,600 stocks in the MSCI World Index - a common investing benchmark containing only very large companies. If you give fund manager A the ability to invest in any stock and fund manager B the ability only to invest in 800 of the better ethical stocks, then you are asking fund manager B to beat fund manager A with one hand tied behind his back.

The good news? Reducing the opportunity set that a fund manager has doesn't affect performance too much - especially if you are only cutting out a few sectors. There are plenty periods where fund manager B will outperform.

The bad news? If fund manager A and B have the same skill, you have to expect the ethical one, in the long run, to have a worse performance.

However, it plays out differently in the real world.

For example, over the last few years, the oil price fell from $100+ to $50 and stock prices of oil companies plummeted. Energy is generally negative in ethical screens and so managers who couldn't invest in oil stocks (the ethical managers) outperformed those who could (everyone else).

In the other direction, there are funds that exclude only tobacco, and these funds over the last 10 years have generally underperformed the world index as tobacco stocks rocketed up:

This says nothing about the ability of the ethical managers or does it suggest that tobacco stocks will outperform forever - it simply means that one sector of the market performed well over a period and so anyone who was prevented from buying stocks in that sector was at a disadvantage.

From a quantitative perspective, corporate governance (the "G" in ESG) is a factor that outperforms - i.e. companies with good corporate governance tend to perform better than those with poor corporate governance.

But, as with all quantitative measures, it comes with some large caveats.

It is hard to say with any precision.

The key question is how much of the market you are removing. At Nucleus, we let investors customise to their own needs and exclude stocks that don't fit their own ethics. A common ethical screen at Nucleus is to remove any stocks involved in cluster munitions from the portfolio. The effect of this is only to remove a few stocks from the universe of 1,600 and so is unlikely to have any meaningful effect on performance.

Investors can then choose to remove companies involved in any weapons manufacturing. This will also remove not only a number of large US defence contractors but also stocks like Boeing and so the effect will be greater.

If I run simulations and assume about 25% of all stocks are excluded, sector outperformance is relatively random and that investment managers have some skill then you can pencil in a typical performance hit of less than 0.5% over the long term. In individual years the difference can be much greater, a 2-3% difference in performance would be quite common.

If you cut out more or less the effect changes - but not linearly, the expected performance gets exponentially worse as you remove more stocks. Also, the more skill that you think managers have, the greater the effect is likely to be as well.

There are three different approaches that different ethical funds use to select stocks:

Positive investing is difficult - finding stocks that are good quality and cheap is hard enough. If you find a stock with very positive ethical characteristics that is only average quality and the stock is very expensive should you buy it anyway, expecting a poor return? Additionally, when you buy a stock on the stock exchange you are not providing funds to the company to support their investments, you are providing them to the previous owner of the stock.

Negative screening needs to be customised, which makes investing in an ethical fund difficult. One investor may think that tobacco is a terrible additive product but gambling is an individual's choice. Another investor may have exactly the opposite view.

Best of breed can be similarly problematic. If you don't want exposure to fossil fuels, then holding a gas producer with the view that it is "the least damaging, and it is cheap and so I think I can profit from it" can seem hypocritical.

Nucleus: At my fund, we decided that the best result for our investors would be to incorporate corporate governance screens into our stock selection process, and then to allow investors to add negative screens that customise the ethics to investors own views.

This is possible as we run managed accounts, but is something that you wouldn't be able to do if you invested in a traditional managed fund.

2.1 Issues in defining Ethical stocks

Environmental, social and governance investing, also known as ESG is a common way for investors to look to add ethics to their portfolio. A recent CLSA report highlights that ESG ratings are more akin to snake oil than medicine. The ESG ratings might not do you too much harm, but don't mistake them for medicine.

By way of background, there are a number of fund managers running ethical funds with an investment process of:

i.e. the fund manager basically outsources the ethical part of the job and focusses on the stock picking.

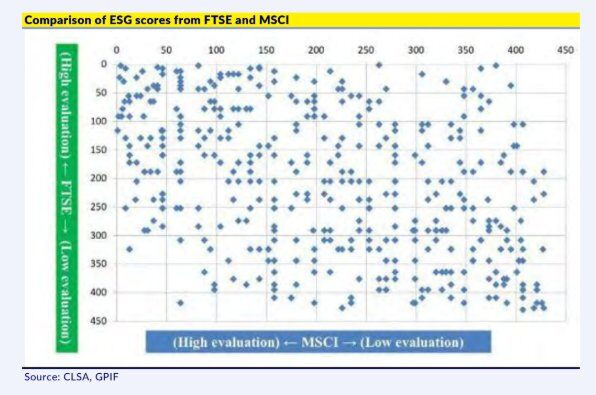

The problem is there are a number of different providers out there who sell ESG rating scores, and CSLA just put out a report showing how the ESG scores from two different researchers (FTSE and MSCI) compare:

Key comment from the report:

We believe that these studies do not discredit ESG data or the practice of scoring

I beg to differ.

The chart above clearly shows there is little relationship between the two, i.e. there are lots of pristine ethical stocks by one methodology that are pariahs under the other methodology and vice versa. Tesla was a stock CLSA highlighted as:

Having spent a lifetime with quantitative scoring systems I can tell you that most of them have significant problems as soon as you start trying to combine different measurements - for example Alphabet (Google) has a broadly diverse and independent board (good governance) but a shareholder structure that gives some shareholders more votes than others (bad governance). Which is more important? How can you combine those into a meaningful score?

Add to that the problem of measurement. Measuring something like board diversity is difficult enough, but reading about how a company rates on "social" impact can sometimes seem to have the same intellectual rigour you would expect to find in your horoscope.

Then you get to the ethical side. Some people think tobacco is horribly addictive and unethical but gambling is each person's own choice. Others have exactly the opposite view. Some people are happy to own Boeing as most of its business is from passenger aircraft, others don't want any company involved in warfare (Boeing supply planes to the US military).

Rather than letting an ESG ratings company make these choices, I prefer to let investors make the ethical decisions - I'll knock Boeing out of the portfolio for some investors but keep it in for other investors.

For governance scores, I prefer to use them as a negative screen rather than a positive one. i.e. bad governance can make a quality score worse (and therefore the company needs to be cheaper before I buy it), but I'm not deciding to buy the company with 42% gender diversity over the one with 35%. Many of the governance scores are like that - there is a clear "bad" option, but there is little sense trying to rate the difference between two good options.

2.2 Effects of these ethical scoring criteria

The Wall Street Journal highlights the effects of ratings like this

Funds with a focus on socially responsible investing are enjoying a record year of inflows in 2019. But many such portfolios aren’t as clean as investors might expect.

Eight of the 10 biggest U.S. sustainable funds are invested in oil-and-gas companies, which are regularly slammed by environmental activists, according to a review of the funds’ public disclosures.

...

Vanguard Group’s FTSE Social Index Fund is meant to track an index excluding companies with “significant controversies regarding environmental pollution or severe damage to ecosystems.” Both that fund and another large ESG fund operated by Xtrackers include Occidental Petroleum Corp. , which in 2015 paid Peruvian indigenous villagers an undisclosed sum to settle a suit accusing it of contaminating the Amazon.

If you are going to invest ethically, you should pick a manager charging fees that also would be considered ethical!

Have a look at the fees before you invest. There are a number of large, well-known brands that charge up to 2.5% for ethical investment. If you need to add a financial planner for another (say) 1% then you are down 3.5% every year before you even start. Ouch.

In comparison, a Nucleus portfolio tailored to your ethics would be 70% cheaper (around 1%). We have a number of competitors that charge a similar amount or a little more. You can get ethical Exchange Traded Funds (which invest in a basket of stocks based on fixed, pre-determined rules) costing somewhere between 0.5% and 1.3% per annum.

Look at the fees before you invest.

According to SuperRatings, Lonsec has sustainable (AKA ethical or ESG) super funds charging high fees and underperforming:

the median performance of ‘sustainable’ investment funds is lower than the median performance of the SuperRatings SR50 Balanced (60-76) Index, comprised of traditional balanced super funds. Furthermore, the ‘sustainable’ funds have higher median fees. The combination of the two means a sizeable number of ‘sustainable’ funds produce sub-optimal returns at relatively high fee levels.

Source: superratings.com.au

As I already mentioned, finding a company that is good quality, cheap and will positively benefit society is incredibly difficult - it is rare to find two of those qualities and so getting all three together is next to impossible.

My weakness with positive ethical investing is that I'm a sucker for a good biotech or green technology story. Hearing these companies talk about how they are curing this disease or that, seeing the pictures of the kids who will be saved if their drug/device works, hearing about how this new technology will produce cheap, clean energy can be an uplifting experience.

"Not only will my investment make me money, I'll be saving sick kids/the world from global warming!"

If you ever get the chance to hear some of these presentations, it's hard not to be moved.

But the focus is rarely on the value of the proposition, its all about the technology/good that it is doing. And that's a recipe for losing money on an investment.

If there is a cause you are passionate about and you want to support companies in that area, there are four ways you can support that cause, in order of most helpful to least helpful:

In my view, investment performance problems with positive investing make it a difficult proposition. And, to me, best-of-breed seems insincere.

Luckily, in recent years investment technology has moved on from the one-size-fits-all ethical funds being the only option.

At Nucleus Wealth, we decided the best result for our investors would be to allow everyone to add their own negative screens. For example, some people like nuclear power for efficiency and carbon reduction benefits. Other people believe the risks to the environment and contamination are too high.

So, we run relatively large portfolios in separately managed accounts, and let each investor decide what to exclude for their own portfolio. We then run systems over the top of client investments to make sure that the portfolio is still appropriately diversified. This can even be done in superannuation accounts without needing an SMSF.

Damien Klassen is Head of Investments at Nucleus Wealth.

{kind=link}