Will commodities really save your portfolio from inflation?

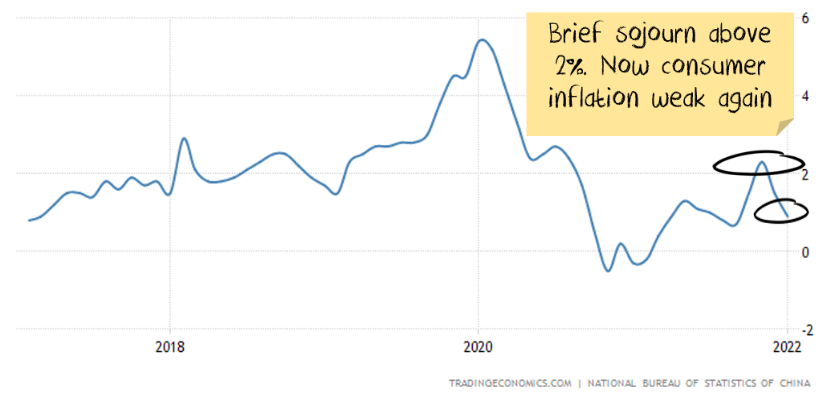

Chinese inflation indexes were weak again yesterday. Consumer price inflation has been weak for more than a year now. Yesterday merely confirmed December's downtrend.

The more interesting action is in producer price inflation. This had been running hot, no doubt fuelling inflation concerns globally:

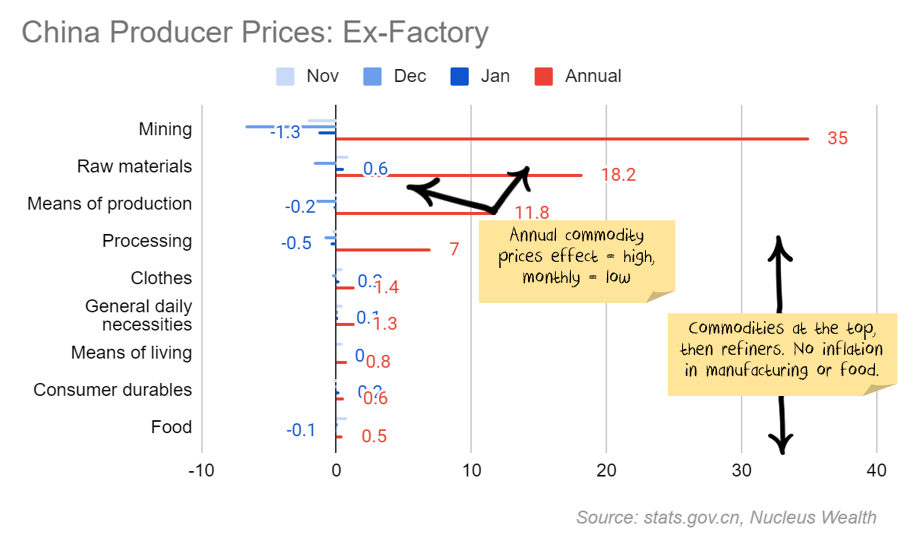

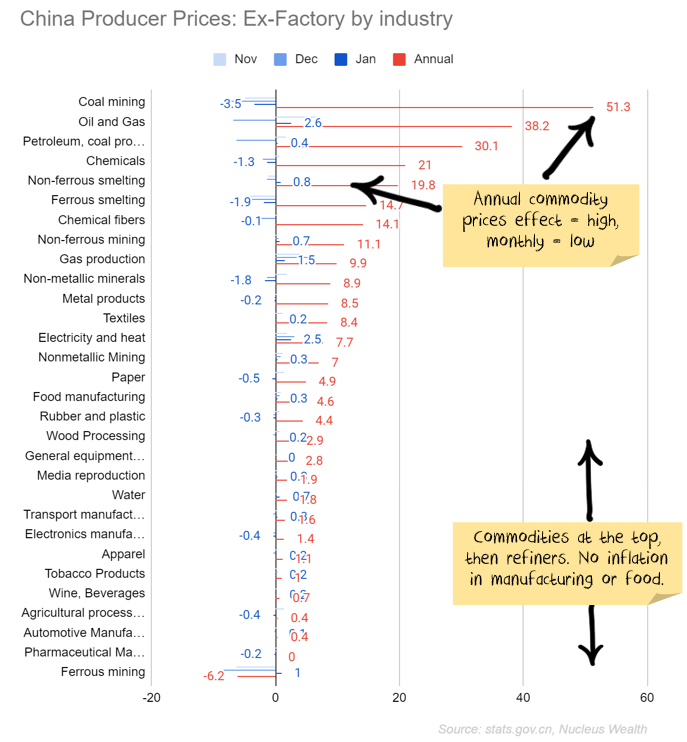

Under the hood is where producer prices become more interesting. All of the annual growth is in energy and commodities. But, even in those categories, the last three months have seen reversals:

If you look deeper again, pure manufacturing sectors haven't seen inflation. The inflation is mainly in the energy and commodity space.

The refiners (who use commodities as an input) are affected to a lesser extent.

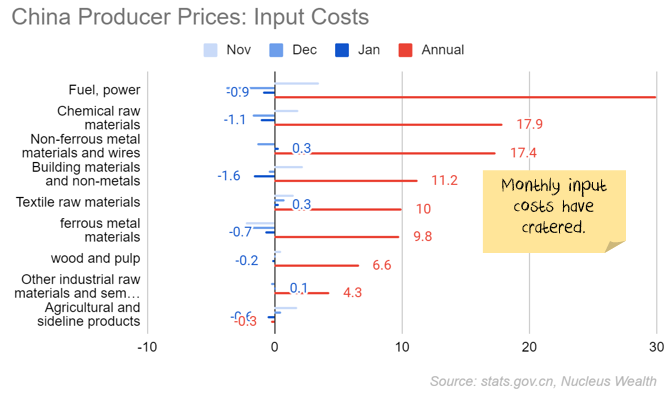

Finally, if you look at input prices for industrial companies, the story is the same. Annual commodity inflation = high. Monthly = deflation.

Wall Street wants you to buy commodities

The Wall Street narrative is that the only thing that will save your portfolio from inflation is commodities.

If you are betting on commodities to save your portfolio from inflation, at least consider these points first:

- Buy high, sell higher? If you adjusted for inflation, most commodities decline in the long term. But, most commodities are close to their all-time highs. So you are not starting from a good place. Effectively, you are buying high and expecting prices will go higher.

- Don't ignore financialisation. Almost all of the producer inflation we have seen in China has been from commodities. i.e. you are buying commodities to protect yourself from inflation mainly driven by commodities. If Wall St can get enough investors to believe the story, it becomes a self-fulfilling trade. BUT, when it goes into reverse, you do not want to be left holding the bag. As you can see from the China numbers above, the last few months are not looking good.

- It may be a price super-cycle. It is not a volume super-cycle. Supply volumes struggle to keep up with booming demand in a real commodity super-cycle. But that is not the case now. Prices for most commodities haven't risen on the back of booming volumes. They have increased because of supply shortages and disruptions. If supply disruptions end and higher prices spark increased supply, prices will reverse quickly.

- Don't ignore the elephant in the room. The largest consumer of commodities in the world is the Chinese property sector. Housing starts are down 30% over the last few months. But slowing starts take some time to filter through to commodity demand. The effects are only just beginning.

- US wage inflation is the most important factor for continuing inflation. That story is not yet determined. But higher US wages do not automatically mean higher commodity prices.

It may be that the "buy commodities to protect from inflation" narrative is so strong that it steamrolls the fundamentals. But that is a speculative investment - buying because you think other investors will keep buying. The other alternative? Anyone who was in the commodity trade over the last 18 months needs to find a buyer to exit the trade before it unravels. And so they want to talk up the benefits of holding commodities in the media. If you are investing in commodities now, you are hoping the former is true rather than the latter.

Damien Klassen is Head of Investments at Nucleus Wealth.

Follow @DamienKlassen on Twitter or Linked In

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an Authorised Representative of Nucleus Advice Pty Limited, Australian Financial Services Licensee 515796. And Nucleus Wealth is a Corporate Authorised Representative of Nucleus Advice Pty Ltd.