Q3 Earnings. Recovery gets pushed another quarter out

I've spoken about the next couple of reporting seasons being crucial in working out the path for stocks. Earnings have been coming in negative for the last few quarters, but forecasts imply an earnings boom.

As each quarter comes in and disappoints, the recovery simply gets shifted out. Maybe that is the path to a higher stock market? You can justify higher stock prices if you always expect an imminent earnings recovery.

The problem comes if we get capitulation at any point. If the 25% growth forecast over the next two years becomes 5%, look out. Until then...

Third quarter results

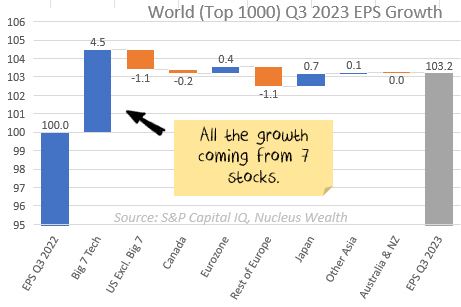

The first and second quarters saw profits down around -5%, but the third quarter was much better. However, the third quarter was mainly about a couple of individual stocks. And we've seen significant downgrades to the fourth quarter.

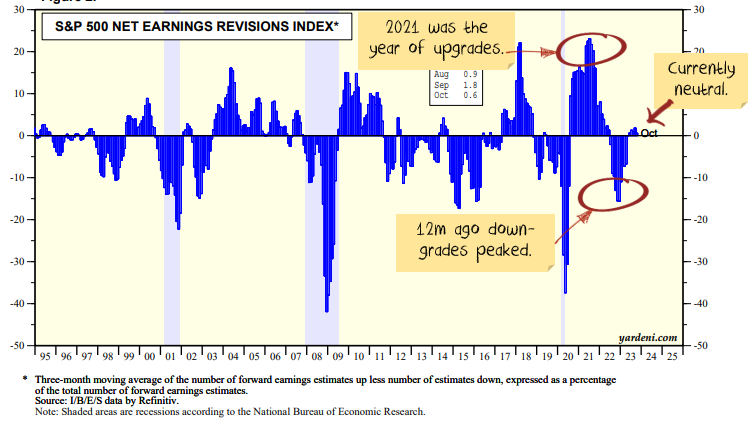

Earnings revisions are neutral.

Two factors affect this. First, actual earnings keep getting downgraded. But, earnings growth expectations have been upgraded by more than the downgrades.

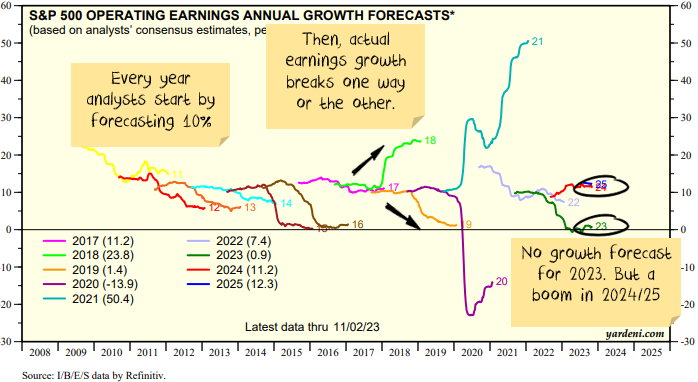

Analyst forecasts almost always start at 10%...

But 2024 forecasts have been persistent. Usually, if 2024 growth was going to be lower it would be falling already.

2023 had a similar pattern, starting at 10% and ending at zero. It remains to be seen if 2024 will hold firm at the 12% growth rate or break down.

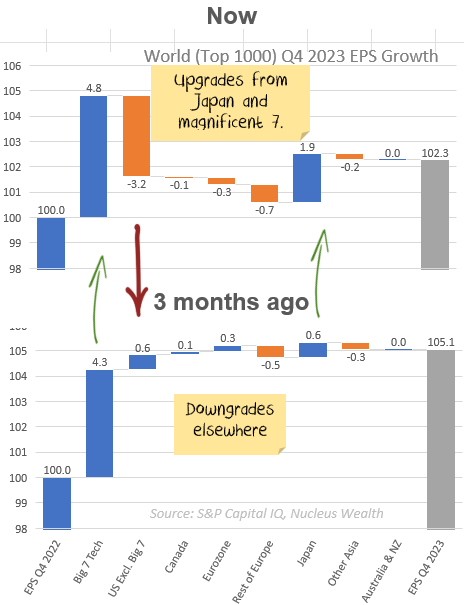

Q3 results were good. It looks like growth will be about 3%, up from expectations of -2% two months ago. But at the same time, we saw significant downgrades to Q4 numbers, down from 5% two months ago to 2% now.

Most of Q3 growth comes from the "magnificent seven".

Other stocks detracted from growth in aggregate:

The story is the same for Q4. Upgrades over three months to the magnificent seven and Japan. But big falls everywhere else.

Biggest upgrades/downgrades to 2024 forecasts

If I look at the top 1,000 stocks globally, 19% upgraded 2024 earnings forecasts vs 31% downgrading (using +/- 3% as the cut-off, measured in USD over the last 90 days). So, the individual skew was toward downgrades. However, the larger companies were more likely to upgrade, so the average 2024 growth held up.

Transport was among the hardest hit. Companies such as Maersk (shipping); Knight-Swift, CH Robinson (both trucking) and UPS (parcel delivery) saw particularly meaningful downgrades. Spot delivery prices have already crashed, but the companies often have longer-term contracts, so the impact is delayed. We recently ran a podcast on when we might get to the bottom in transport. Conclusion: not yet.

Semiconductors are mixed. Big NVIDIA upgrades pretty much swamp the rest of the sector. Intel helped as well. But many big names saw significant downgrades. Cisco, ASML, AMD, ON Semiconductor, Teradyne, Western Digital.

China is building a lot of capacity in this space, particularly for "lagging edge" chips. Prices are going to be lower in that part for years.

"Leading edge" chips are looking better. But if China was a big customer, US regulations may ban sales. So, a challenging environment.

Healthcare - especially the more "tech" end saw big downgrades.

Financials - Blackrock, Charles Schwab, and Morgan Stanley all had 2024 downgrades by more than 10%.

Energy stocks generally saw upgrades. The war in Israel caused an oil price spike, and we are now seeing the oil price fall. The next batch of changes will probably be downgrades.

Low profitability/loss-making tech stocks saw significant upgrades. DraftKings, Twilio, GoDaddy, Block, Door Dash, SoftBank, Shopify, Splunk, Live Nation, Okta, Data Dog and Crowd Strike, just to name a few.

I'm not sure how to read this trend. For some, they are finally becoming profitable. On the other hand, raising capital is more challenging than a year ago. So, it might be more about these companies pulling back on costs (and losing less) because they don't want to run out of money.

Japanese car makers Suzuki, Honda, Subaru and Toyota have also seen reasonable forecast upgrades.

There is still lots of optimism for 2024

There were downgrades to Q1. But upgrades to the rest of the year.

I can't put my finger on the broad optimism. My impression from company conference calls was that companies expect their own price rises to continue but lower cost pressures.

Which has some cognitive dissonance at the macro level: "All my suppliers will have to lower their prices, but I'll be fine". This will be true for a few companies, but it can't be true for everyone.

Higher quality stocks can generally hold on to margins when everyone else's are falling. A good reason to up the quality of stocks in your portfolio for the next year or so. See our podcast for more.

.jpg)