There are three main factors we look at when putting together an investment portfolio in the age of COVID-19. Which sectors/types of companies to own, how many shares and what kind of defensive assets to hold based on the answer to the first two questions.

It is the interplay that is important. If you are going to hold a lot of shares, then you probably don't also want to be holding stocks that are extremely leveraged to a recovery, leaving you exposed it everything doesn't go exactly the way you expect.

What this means is that there is no one right answer, holding a small amount of a particularly high-risk share portfolio and lots of defensive assets might deliver you the same outcome as owning a lower risk shares in a higher quantity.

Types of Pandemic Stocks

We (roughly) classify stocks into three categories:

-

- Pandemic agnostic: These are stocks which are relatively immune to the pandemic. Think supermarkets, many software companies, consumer staples like shampoo, cleaning etc.

- Pandemic beneficiaries: Toilet paper, cleaning and hygiene goods are some examples. These are stocks that benefit from the pandemic. The benefit may fade quickly for some, and last longer for others. Kimberly Clark, Essity, Clorox, Gilead

- Pandemic losers: Travel, leisure, oil, personal services, banks, real estate. These are the stocks that lose the most during the pandemic.

The issue is pricing. The pandemic agnostic or beneficiaries tend to be expensive. The pandemic losers are cheap on last year's profit levels, but for many of the losers, they may not see a profit again for some time. And if the losers are carrying too much debt, then they will likely be insolvent before they have a chance to recover.

An alphabet of outcomes

We have been bombarded with various letters describing the shape of the economic outcome: V, U, W, L-shaped plus other more esoteric options.

It is not only relevant which outcome occurs, but also which is priced.

If you are in the "V-shaped" recovery camp, expecting a sharp economic bounce then you probably want to be picking up the pandemic losers at "once in a lifetime" prices. Although, it would be remiss of me not to note that stock markets tend to crash every ten years or so. Which means you tend to get a lot of "once in a lifetime" opportunities in the average lifetime.

The V-shaped recovery crowd do seem to be in control of stock market pricing at the moment. The problem is if you think there is going to be a V-shaped recovery, but stock markets are already priced for a V-shaped recovery. Then, you have almost no upside if you are right and lots of downside if you are wrong.

What if the virus just takes longer?

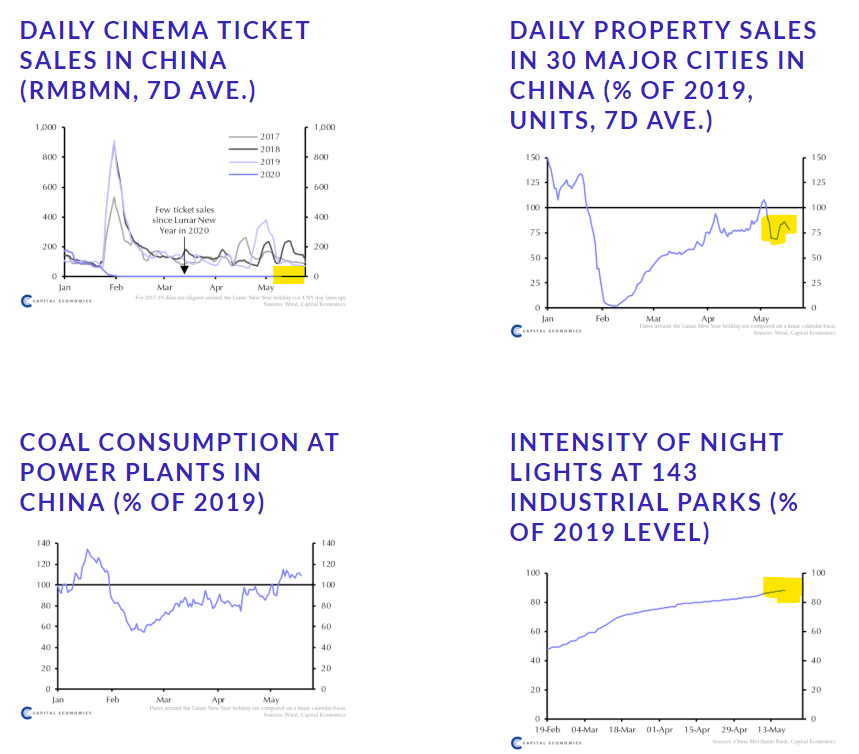

I'm a little more circumspect. China is recovering very slowly.

Singapore and Japan, who thought they had the coronavirus under control, are experiencing second waves of outbreaks.

The countries with the virus seemingly under control (China, South Korea, Taiwan) have tracking measures in place that are aided by a lack of privacy protection. These measures are not legally possible in most developed countries. Singapore (with a high level of government trust) has shown so far that voluntary sign-ups aren't working.

Many virus outbreaks come in multiple waves.

I think it is too early to be wedded to any single virus recovery path.

For rapid economic recovery, treatments are more important than vaccines

While a vaccine is more positive for society's longer-term resilience, a vaccine has a significant testing period. The medical hurdle is understandably higher: you give vaccines to healthy people and you need to make double sure the vaccine doesn't make them sick.

A treatment, in contrast, is given to someone who is already sick, so the hurdle is lower. If (say) the Gilead treatment proves safe, then it could be in widespread use much more quickly to treat patients who would have otherwise likely died.

What about the economic damage?

Just as important is the damage already done. Even if we found a cure tomorrow, we are facing:

- Mass unemployment. Unemployment tends to take years to recover.

- Depressed wage growth, held down by high unemployment.

- A demand shock from consumers looking to increase savings.

- Our economy has been driven for a decade on the willingness of consumers to increase debt at growth rates far in excess of income growth. We are expecting low debt growth at best, more likely to be negative.

- Companies that are looking to deleverage. Meaning lower profits.

- Companies that are looking to increase the slack in their supply chains. Meaning lower profits.

- Companies and governments looking to repatriate supply chains to reduce reliance on imports of critical medicines, food or equipment. Meaning lower profits.

- Small and medium businesses going broke.

- Banks increasing credit checks and decreasing credit availability.

There will be offsets. There will be government stimulus. But these will reduce the depth of the downturn, not prevent a downturn.

How we are positioning our share portfolios

To reduce risk, we have a core of the pandemic-agnostic stocks. The issue is these tend to be expensive relative to other stocks, and so the strategy within this cohort is looking to rotate out of the more expensive stocks and into the cheaper ones as opportunities arise. In this cohort, we own software stocks like Microsoft, online shopping companies like eBay, and supermarkets like Coles, Woolworths and Ahold Delhaize. There are also some unexpected beneficiaries, for instance, we have done well from pet food supplier JM Smucker. While we did expect pet food to hold up, we weren't expecting the increase in pet numbers and pet care driven by the isolation.

One pandemic agnostic stock we held through the crisis but recently sold down was Johnson & Johnson. It is a massive US stock that is in many ways a lot like a healthcare managed fund: quality operations across almost the entire health spectrum. While we like the exposure, Johnson & Johnson is back trading at pre-crisis levels and management guidance (in our view) reflects a "V-shaped" recovery that we believe is unlikely. I'm more than happy to own this stock, but it looks like its already pricing a full recovery which leaves little room for growth and a reasonable amount of room for disappointment.

We also have a lot of pandemic beneficiaries - which is why both our Australian and International portfolios outperformed by so much last quarter. We are generally holding on to these stocks (subject to not being too expensive) with the view that an extended crisis is more likely than a sudden solution. Within these stocks, we have a time-frame within which the effects will fade. For example, toilet paper manufacturers like Kimberly Clark have benefitted in the short term, but we are not expecting a permanent change in demand. On the other hand, some of the hygiene and cleaning manufacturers may see a number of years of increased demand before returning to trend. Essity, a large Swedish company that supplies hospitals globally with sanitiser and hygiene products, is a core holding for us in this space.

Clorox, the leading producer of bleach and other cleaning products in the US, is also likely to see years of increased growth. However, while Clorox made our clients a lot of money over the past two months, it has risen to valuation levels more appropriate to companies with far more intellectual property than a formula for bleach and some marketing. So, Clorox is another we are happy to own at the right price, but almost 30x earnings isn't that price.

We hold hardly any pandemic losers. However, we do have a shopping list of our favourites that we would like to buy when the recovery is clear. There is a lot of nuance within this group. Some stocks will recover quickly once lockdowns are eased, many, like international travel, will take years to return to trend growth. I'm not that keen to front-run my own purchases in this cohort, so I can't give you direct names. What I will say is that we have a shopping list ready and relative pricing metrics where we will likely buy these stocks regardless of the pandemic situation. While debt levels are important if you want to buy these stocks early, the debt level will be less important once the recovery is in full swing. We don't really play in the high-risk/low-quality stock space, but they will be the ones that bounce the most. The best returns will come from the oil companies, airlines and banks that almost go broke but don't.

With volatile share markets, within each cohort we are continually looking to increase the quality of the portfolio where possible. As some of the stocks become expensive, we look to trade into cheaper or better quality stocks.

The plan is that if effective treatments or widespread exits from the lockdown appear likely then we are ready to switch out of the pandemic winners and into our pandemic losers.

But, for the present, we are taking the view that market has already priced in a V-shaped recovery. Therefore, there is far more downside from a V-shaped recovery not occurring than there is upside if the recovery is faster than we expect.