Extra superannuation contributions or mortgage payments: Which is better?

I'm going to look at some different options for superannuation strategies:

- Should you put an extra $10,000 of your income into super rather than your mortgage?

- Should you put an extra $10,000 of your savings into super rather than your mortgage?

- Say you have $10,000 in shares with $5,000 of capital gains embedded. Can you transfer that into super to reduce your capital gains?

- Say you don't have a mortgage. Should you put $10,000 into investments in your own name or in superannuation?

The right choice depends on various factors, including age and financial goals. There are also caps on how much you can transfer.

What are the scenarios?

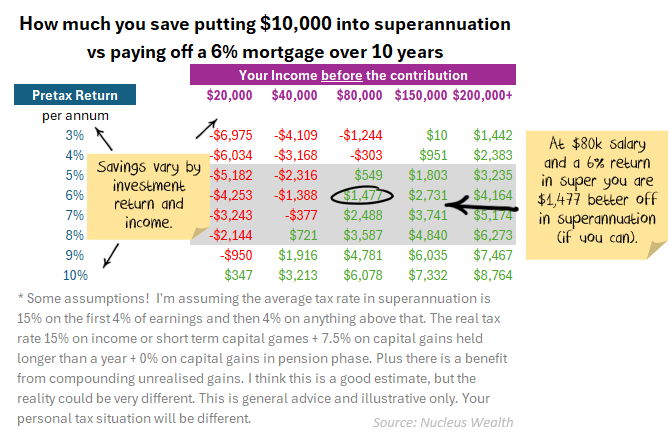

Say you earn $100k and decide to put an extra $10,000 into super rather than pay down your mortgage, which has an interest rate of 6%. I'll do a comparison over 10 years. First, I'll give you one example, then I'll show a table for different returns and tax rates:

-

- At $100k, your marginal tax rate (in 2026) is 30% + Medicare levy = 32%. So, your $10k becomes $6,800 off your mortgage after tax or $8,500 invested in super. i.e., you are $1,700 better off on day 1 in super.

- If you save 6% on your $6,800 mortgage reduction over 10 years = $5,378 in interest avoided, tax-free. If you made 6% in your $8,500 in superannuation and then paid tax on it = $5,155 after tax = $223 worse off in superannuation.

- Net effect = $1,477 better off in super.

- This is shown in the circled figure below:

You can see that the outcomes also change as your income and the return vary.

As you might guess, higher interest rates make using the money for your mortgage more attractive and vice versa. Shortening the time frame makes superannuation more attractive and vice versa.

Net effect: at higher incomes superannuation will almost always end up in front. Below $50,000 in income you stand a reasonable chance of being worse off.

1. Should you put an extra $10,000 of your income into super rather than your mortgage?

Arguments to put $10,000 into superannuation:

- Tax Benefits:

- Concessional Contributions: superannuation contributions are taxed at a concessional rate of 15%, which is lower than most individual income tax rates. This can lead to significant tax savings.

- Compounding Growth: The earlier you contribute, the more time your money has to compound. For a 30-year-old, this can result in substantial growth over time.

- If you have a high income, your returns over ten years would need to be exceptionally bad for you to be worse off.

- Retirement Security:

- For individuals of all ages, boosting superannuation can enhance retirement security by increasing the overall retirement fund.

- At older ages, with retirement approaching, additional contributions can help catch up on retirement savings.

- Behavioural finance:

- For some people, having inaccessible savings is a good strategy to limit spending.

- For some people, having a higher mortgage to pay down is a good "enforced savings" strategy.

Arguments to pay down your mortgage:

- Accessibility:

- Superannuation is locked until reaching preservation age (usually at least 60). For a 30-year-old, this means the funds are inaccessible for decades.

- Even for a 50-year-old, the funds are tied up until retirement age. But the closer you are to being able to access the money, the less this will matter.

- Do you have savings for unexpected events? If not, you might regret the decision. For the sake of a few thousand dollars of tax savings, you might lose the chance to pay for a loved one's medical treatment, wedding or other important event.

- Market Risks:

- Investment returns within super can fluctuate with market conditions. While younger individuals have time to recover from downturns, older individuals, such as those around 65, face more immediate risks.

- Behavioural finance:

- For many people, having a lower level of debt reduces stress.

2. Should you put an extra $10,000 of savings into super rather than your mortgage?

What is the difference between savings and income? On savings you have already paid the tax, so there is no longer an advantage on the initial contribution.

If you are assessing this over ten years, probably pay off your mortgage. For you to be better off, your superannuation returns will need to beat your mortgage interest by about 2%.

If returns are any lower, and you will be thousands of dollars worse off. So, unless you expect booming investment markets, you should pay your mortgage down.

3. Say you have $10,000 of investments with $5,000 of capital gains embedded. Can you transfer that into super to reduce your capital gains?

Most likely: no. If you have a self-managed superannuation fund (SMSF), then I'll give you a heavily (heavily) qualified "maybe". Don't try this at home! Get professional help if you are hell-bent on trying this.

It will probably be a capital gains event, i.e., you must pay tax on the gains when you transfer the shares into superannuation.

So, you are left with the same situation as in option two above but also have a tax bill.

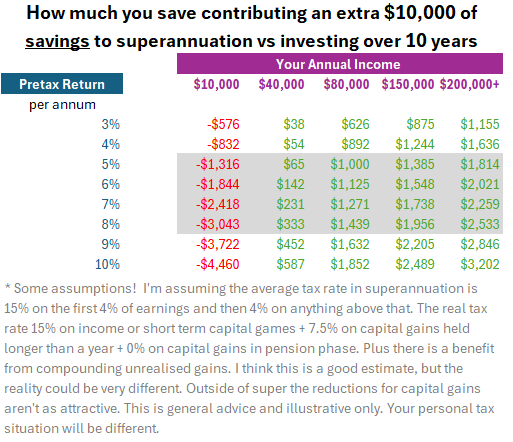

4. Say you don't have a mortgage; should you put $10,000 into investments in your own name or in superannuation?

In superannuation, except if you have less than $20k in income. Over ten years, here are the relative differences (assuming tax rates don't change!):

The differences are meaningful, but you need to contrast them with the accessibility issues.

Conclusion

If you have sufficient savings for unexpected events and are in a higher tax bracket, shifting more money into superannuation is almost always a good strategy. However, there are caps on how much you can transfer.

Transferring savings or other investments is a more marginal proposition vs paying down your mortgage.

But versus investing in your own name, superannuation wins almost every time.