The battle between bulls and bears began in earnest this year. In January, the bears had the upper hand and the ASX 200 dropped 6.4% and the MSCI World fell 5.5% in US dollars and 2.3% in Australian dollars. Our best performing fund was our international portfolio which managed to eke out a small gain through conservative stock selection.

While the bulls have done better in February, the market remains volatile. Movements of 2% in either direction have become commonplace.

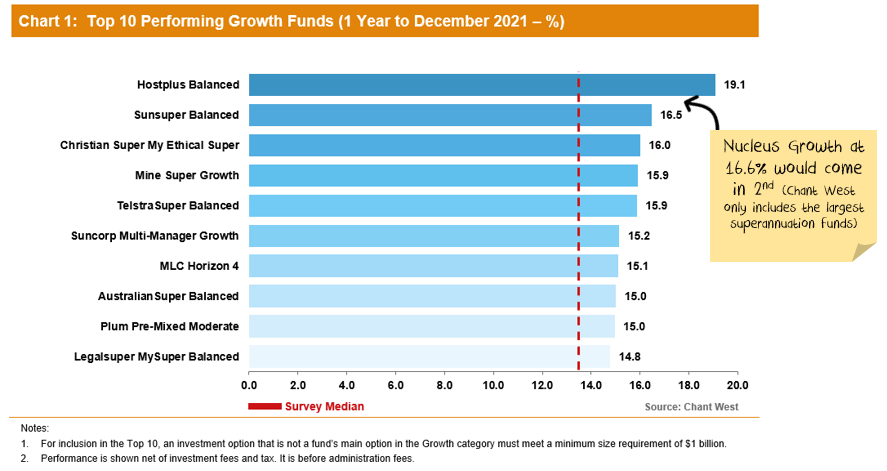

Our growth fund finished 2nd vs other superannuation funds for 2021, so we were no stranger to holding risk assets during 2021. However, that is no longer the case.

One of the hallmarks of our growth fund to date has been our willingness to reduce risk when we believe the risk/return rewards are not appropriate. Now is one of those times. We are holding over 30% cash and bonds.

Morningstar measures the Nucleus Growth fund vs other "Multi-asset aggressive" funds, and while the outperformance is heartening, we are most proud of achieving the performance with half the volatility of others:

Our concern is that central banks are suggesting that they will solve inflation problems, which are largely a result of supply chain issues, by restricting demand. Given the problems that the world has had since the financial crisis, in our view that is not an attractive setup for markets.

We expect international equities to provide some protection from a growth slowdown. While the Aussie dollar is likely to rise if the energy crisis worsens, it is more likely to fall over the medium term. This will hedge the downside under the worst scenarios, whilst still providing some upside in the better ones.

More certainty emerges

Last month, I wrote:

I have some pretty clear ideas about which trends are sustainable and which ones aren't in the long term. However, the short term is far less clear.

I discussed the elevated levels of uncertainty and how our conviction positions were being scaled back.

As soon as I had hit the publish button, events conspired to bring more certainty:

- The Omicron variant looks to be resolving in the direction we expected, ripping through economies without too much harm and leaving behind an acceptance that it is endemic.

- The geopolitical energy crisis in Europe has turned into a military standoff.

- Supply chains have improved a little but are still clogged.

- Demand is challenging to read and distorted by Omicron. Demand held up far better than prior virus waves.

- Governments continue to withdraw (or not replace) stimulus. There will be a fiscal shock in 2022. The question is whether the private economy will be strong enough to withstand it.

- Central banks have made it clear that they will try to solve the Russian induced energy issues and supply chain induced inflation by raising interest rates. The odds of a policy error have increased significantly.

- China still has not bailed out the property sector. China is trying to ensure that houses under construction get built, small businesses have access to credit, infrastructure building continues, and failing developers do not crash the economy. But China is yet to show any signs of turning back to the old days of debt-driven property developer excesses. Unless they change, this will continue to deflate the commodity market.

- Labour markets became more uncertain in January and Omicron boomed throughout the world. It will be months before a clear picture emerges.

It is still not the time for intransigence. Events are still moving quickly. But we have positioned the portfolio towards the most likely outcome and are gradually increasing the weights as more data arrives.

Australia side note:

The risk of policy error in Australia appears less than overseas. However, our fortunes are tied to world events from an investment perspective.

In our view, there are four reasons why the RBA does not need to hike rates soon, and that doing so would be a policy error. It remains to be seen whether the RBA will be pressured to hike rates anyway.

First, after six straight years of missing the inflation target because of weak demand, snuffing it out the moment demand lobs into the range reeks of panic. Let the demand overshoot before trying to slow it down.

Second, most inflation is still exogenous via oil and supply chain issues. The 3% wages the RBA needs to see for sustained inflation within its target band has not been seen for a decade. Reopening borders to a flood of immigration could snuff out wage growth overnight.

A wages overshoot would not be disastrous. With the massive debt burden in Australia, getting inflation down can be done at any time.

Third, the number one driver of Australian household confidence and consumption – house prices – is stalling fast. Macroprudential and fixed-rate mortgage hikes have already ended the boom at a brick wall. There are big rate hikes now embedded as fixed rates expire. This will automatically ratchet up household pressure. A price correction is baked-in for Australia's two largest cities. Any rate hikes at this juncture risk an inflation-snuffing downward spiral.

The final reason is exogenous, like most of the inflation is. It is the peculiar combination of moves by the US and Chinese central banks. The Fed is moving to crush considerably worse US inflation. To do this, it will have to risk an outright US recession. This is because Wall Street is encouraging markets to hedge inflation by bidding up commodities, only succeeding in creating more inflation in the process. The Fed will have to kill this trade, most obviously in oil, and the only way to do it is to damage demand enough that commodity prices crash.

Oddly, it will be aided in this endeavour by authorities in China who have embarked on the weakest stimulus program in modern times despite an outright crash in the Chinese property market.

Ending the commodity mania will probably take a few US rate hikes and trigger a US recession panic in markets by mid-year. If it does take longer, then it won't be much. The rout is already underway in global junk debt and equity.

This circumstance is eerily similar to the set-up of early 2008 when the RBA hiked rates directly into the GFC. Then too, it was trying to fight largely imported inflation and only ended up crushing domestic demand instead.

We might see the banks get one or two flexible mortgage rate hikes through before it all falls apart, but hopefully…probably…the RBA has learned the lesson of 2008 and will ignore the inflation peacocks squawking in front of the oncoming Mack truck.

Asset allocation

Stock markets are expensive. Debt levels are extremely high. Government/central bank support continues but is slowing. Earnings growth had been really strong but has come to a halt.

Markets are supported to a great degree by central banks and governments. Policy error is every investor's number one risk.

But, any number of other factors could force this off course and see unexpected inflation. Mutations could disrupt supply chains again. Chinese/developed world tensions might rise further, leading to more tariffs. Or, China might reverse its tightening on property sectors. Biden may get through additional stimulus, driving increases to minimum wages.

We are significantly underweight Australian shares, with the view that the Australian market will be the one most affected by a slowdown in China:

Australian equities have been a good source of investment performance in recent months. We switched out of them and into international equities and cash. For the last few months, the timing has been good. Not so during October when markets shrugged off the China issues. We have largely built the defensive side of the portfolio up, changing out of value winners like resources, banks and cyclical industrials.

Performance Detail

Core International Performance

January saw Nucleus Wealth avoid the market sell-off seen primarily in US growth shares. Japanese stocks came to the rescue and our lower Growth stock weighting meant the portfolio didn't experience the same selldown in US stocks

Currency tailwinds helped all regions as the AUD (considered a risk currency) was sold off. During the month we increased our global bank holdings and down-weighted some growth stocks while transferring our Booking.com holding into Expedia which has performed well for us.

Core Australia Performance

The Core Australian portfolio underperformed, largely due to our underweight to resource stocks as we remain wary of a commodity price bubble. Over January, we down-weighted some growth stocks, up-weighted banks and added some Woodside to protect against growing geopolitical tensions.

Damien Klassen is Head of Investments at Nucleus Wealth.

Follow @DamienKlassen on Twitter or Linked In

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Nucleus Advice Pty Ltd - AFSL 515796.