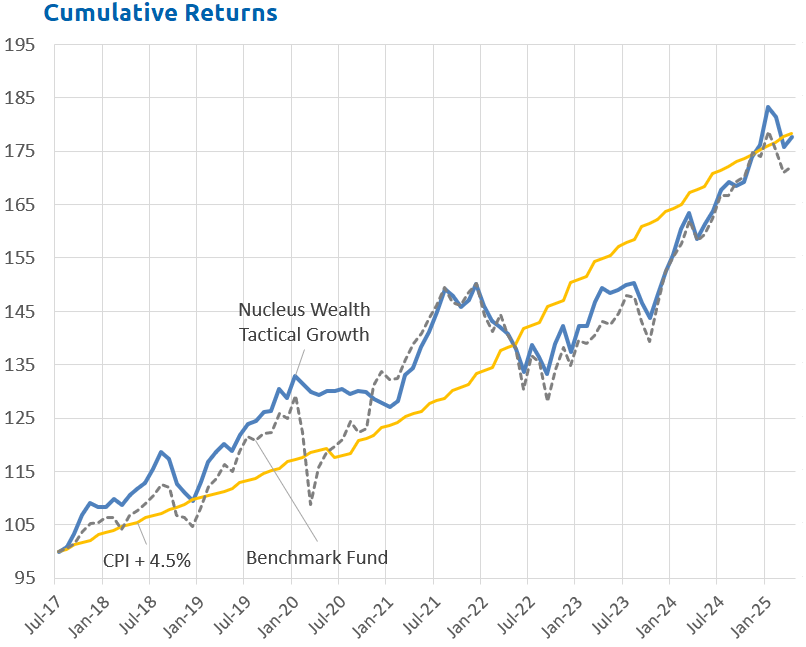

January 2025 Performance

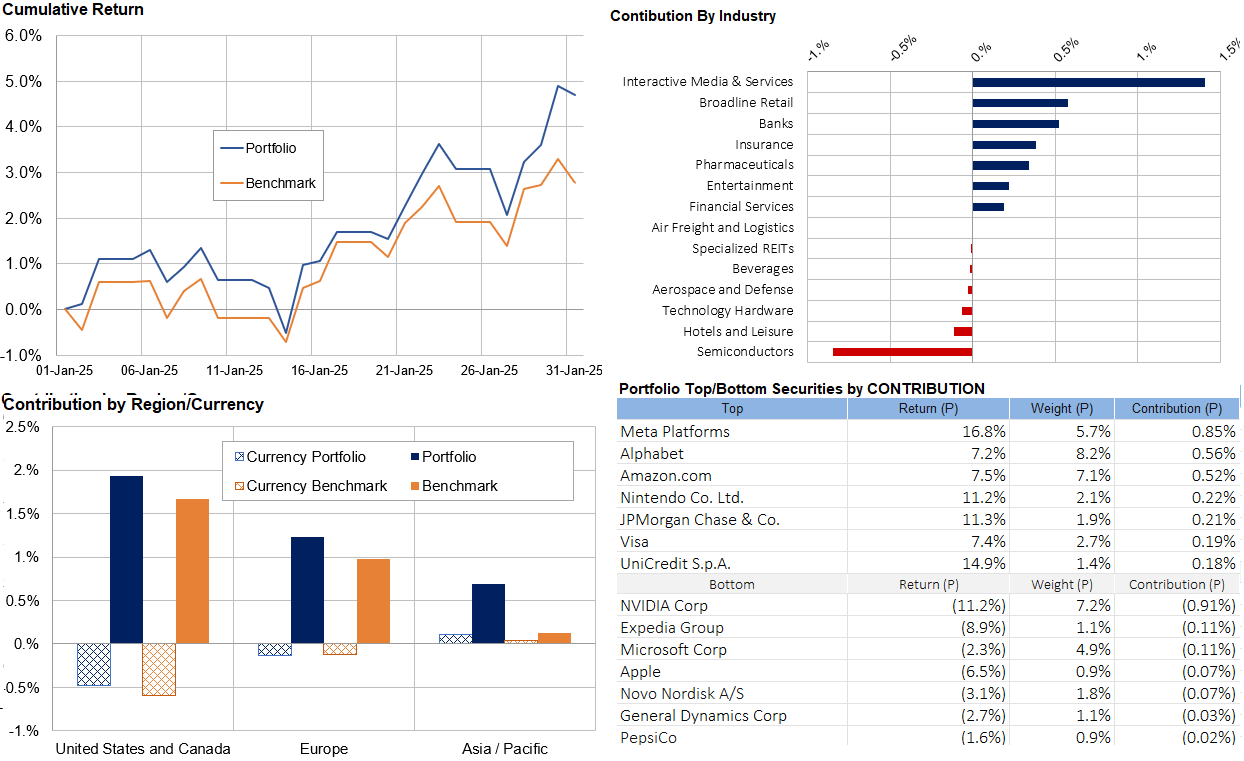

Another big month for markets. Our international portfolio in particular performed much better than benchmark, up almost 5% for the month, while our growth portfolio was not far behind.

Trump: Crash or crash through?

Trump has begun an unprecedented attack on the norms of US lawmaking. The scale and scope of the attack are significant and mostly unconstitutional. The two most likely outcomes are:

- Crash: Trump spends the next few years bogged down in courts.

- Crash through: Trump either bullies, subverts or ignores the courts, creating a more dictatorial system.

The question I am looking at is what this means for investors.

The problem

Most of the issues are the same:

- Trump wants to shut down [INSERT LATEST, foreign aid, education, green spending, financial protection etc].

- Does Trump have the ability? Yes. He would need to draft the removal of the previous laws, pass them through the House and Senate, and then sign them.

- Instead, Trump claims that he has the ability to ignore previous laws. He signs an executive order.

- Someone takes out an injunction. The court issues a ruling preventing Trump from his course of action.

Scenario 1: Crash

So far, Trump's cabinet and appointments have prioritised obedience. He did run on being an outsider, and so he has that right. However, his team is very much lacking in experience (competence?). But if Trump decides to obey the US Constitution, he will need to win legal cases.

At the same time, he is attempting to fire significant numbers from the Department of Justice. Morale from the remaining members is unlikely to be high. They will be asked (ordered?) to make arguments they likely believe unconstitutional. Maybe Trump brings in a bunch of new lawyers who are more amenable or outsources to private lawyers. Either way, his lawyers will be far less experienced in these matters.

Net effect: It is a recipe for being stymied by courts for months or years.

Scenario 2: Crash through

Ideally, Trump wants to get these cases to the Supreme Court. He believes the conservative Supreme Court will give him the wins he is unlikely to get at lower courts. This may be true. It only needs to be true for one case to see him then apply it to every other case.

But, even if it is not true, maybe Trump just ignores the courts. The Supreme Court has already ruled that Trump (pretty much) can't be prosecuted for anything that he does while president. And he can hand out pardons to anyone who might be in harm's way.

He looks to be trying this with USAID.

Net Effect: The US ends up as a dictatorship. In practice, if not in name.

Market impact of the "crash" scenario

Political stalemate can be good for markets. They tend to like the status quo. The S&P 500 has done about 10% better with stalemate (i.e. one major Party with numbers in the House and the other in the Senate) rather than without.

While the Republicans have both the House and the Senate, being stuck in courts for years is probably going to be similar to stalemate.

Effect of moving to a more dictatorial regime: 19th century edition.

There are no real advanced modern country comparisons that make sense. A major issue is that dictatorships usually emerge from economic crises. If it gets there, the US would be one of the few without a financial crisis or war.

If you go back to the early 19th century, there might seem to be some superficial comparisons. From Wikipedia:

Scholars also noted that big business developed an increasingly close partnership with the Italian Fascist and German Nazi governments after they took power. Business leaders supported the government's political and military goals. In exchange, the government pursued economic policies that maximised the profits of its business allies.

But if you look closer, the parallels disappear. Mussolini rose to full dictatorial power more gradually, and by the time he did, the world was deep into the roaring 1920s. Mussolini nationalised industries and spent heavily on education and state assets. That isn't Trump.

In Germany, Hitler took over in 1933 with the German stock market crippled by banking failures and regulation. Then Hitler proceeded to add copious regulations, wealth taxes, and speculation taxes. Companies with rising profits or a return on equity over 6% had to invest in government bonds. Clearly very different.

Effect of moving to a more dictatorial regime: Hungary

Victor Orban is a match politically. Voted out in 2002, he returned in 2010 (post-financial crisis). He immediately got to work changing the constitution, lowering income taxes, weakening the judiciary, reducing press freedoms, making abortions more difficult, and targeting immigrants. Cultural issues are front and centre of political campaigns.

But economically, Hungary is no comparison. It is a tiny, developing country. In the positive column, Hungary's economic growth has been pretty good. GDP per capita has improved from ~50th in 2010 to ~40th in 2023.

The Hungarian stock market is really not relevant. If you are looking for a moral angle, it substantially underperformed the world index during Orban's second term. But it largely performed in line with emerging markets - and Hungary is an emerging market. More importantly, just 3 companies make up 85% of the Hungarian index by market cap. So, stock-specific issues skew any conclusions.

Additional scenario: decreased regulation

Regulatory bodies are being defunded or closed, and inspectors or watch persons are being fired. There is likely to be considerably less regulation in the US.

In the past, fewer regulations have been a good thing for company profits. We expect the same this time.

Regulation is a pendulum. Over time, economies oscillate between too much and too little. There are reasonable arguments that the pendulum has swung too far toward overregulation in some sectors. If true, rolling back regulations will yield productivity gains.

Are there dangers that the pendulum swings too far in the other direction and we see under regulation? Yes. But the consequences tend to take years. For example, the Consumer Financial Protection Bureau has had all activities suspended and its headquarters temporarily closed. If this results in another financial crisis, it will probably take years (and probably some sort of boom) to eventuate.

Additional scenario: increased corruption

I won't go into every example. However, I will say that the behaviour that saw Trump impeached the first time is likely tamer than a number of his current conflicts of interest.

Despite that, it would appear highly unlikely that Trump would be impeached by the current House, almost regardless of the conflict of interest. The Supreme Court has already given Trump the green light to do just about anything as long as it has a whiff of presidential responsibility.

Trump has already suggested removing the constraints preventing companies from paying bribes internationally.

Does that lead to an increase in corruption within the US? Almost definitely. If so, increases in corruption will slow economic growth, although that typically takes some time.

Market impact: outcome

We can definitively say that moving to a more dictatorial regime, with the associated increase in corruption and decrease in regulation, wasn't so bad for a small European economy and stock market over 15 years. But we have a sample size of one. Does that translate to the world's largest? That will be the trillion-dollar question facing the stock market.

Maybe we don't get there though, and Trump is bogged down in courts on major issues until the end of his term.

Morally, many investors may feel that it must end badly. That is usually true for more dictatorial countries with fewer freedoms in the long term. But the short term can be different. We have never seen it occur in such a large, advanced economy. And there will (probably?) be midterm elections in two short years.

Our take is that positive effects are more likely in the short term. There are significant adverse risks into the future, but (a) there is time for the US population to vote differently or (b) those risks to be overcome by other events.

But it is an uncertain time. I reserve the right to change my mind!

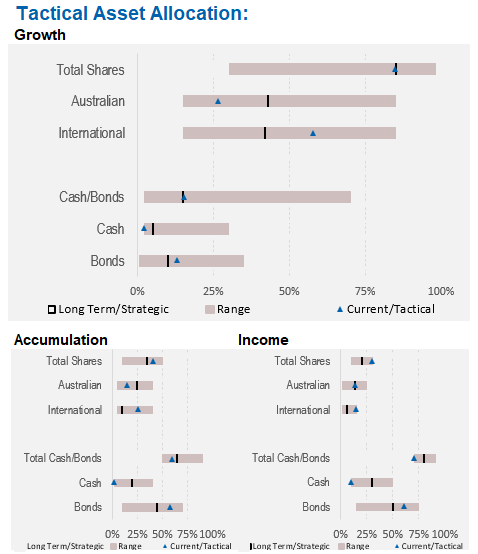

Asset allocation

Earnings growth looks to have turned positive. When you add corporate tax cuts and some margin expansion through lighter regulation and a quite expensive US market becomes merely expensive.

We are underweight Australian shares, significantly overweight international shares, with the view that the Australian market is more affected by interest rates and less affected by an AI boom:

Performance Detail

Core International Performance

January saw the bull market return with our portfolio doing particularly well as interactive Media and Banks drove the results. Pleasingly we outperformed in all geographic regions, Currency was a detractor this month as the AUD recovered from recent lows. We removed CDW and topped up Nvidia following the overreaction to DeepSeek.

Core Australia Performance

Australian equities also had a strong performance especially toward the end of the month driven by Technology, Banks and Gold.