During May, our Australian equity portfolio significantly outperformed the benchmark, bolstered again by our defensive and underweight resources and bank stock exposures. Over the last year, our Australian portfolio has outperformed its benchmark by almost 9% on the back of that theme. Our international portfolio has outperformed the benchmark by 1.2% over the last year but underperformed in May, mostly because we were not exposed to NVIDIA. Our tactical portfolios underperformed as bonds pulled back this month.

Looking forward, we expect weak stock markets as the central banks raise rates to slow demand, shrinking company profits.

With that in mind, the key factor to watch in the coming months to tell if we are wrong or right is the change in corporate profitability. The recent reporting season in the US showed some signs of weakening earnings, but not enough to confirm our thesis yet. Earnings forecasts were largely unchanged for the month.

Jobs continue to defy naysayers

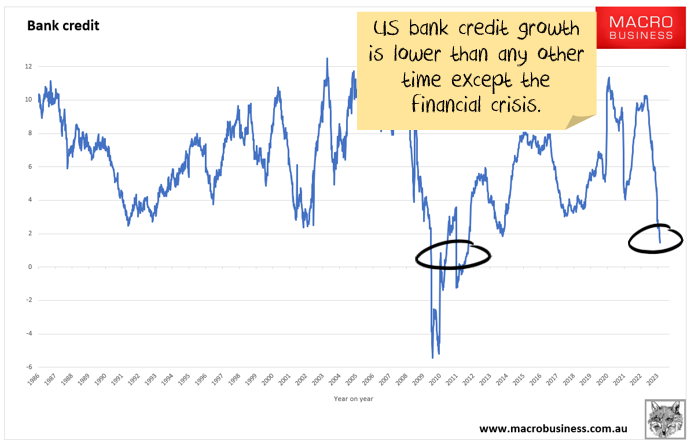

There are a lot of signs that a recession is coming. Bankruptcies are back with a vengeance. Most of the suite of raw materials and commodities have plunged in price. Transport costs are down more than half. Credit growth is running at 20-year lows. Forward surveys are at recessionary levels.

There are two signs, though, that a recession is not here. First, inflation is high, albeit falling. Second, and more importantly, jobs and wages remain strong. And that is where the hopes of the soft landing camp lie. It is all about jobs and wages.

Jobs data

We do need to highlight that data on jobs are a lagging indicator. When an economy enters recession, jobs are usually the last indicator to start falling. Companies tend to cut back on all manner of other discretionary expenditures and plans before finally laying people off.

Globally the story is strong wage growth in most major economies. Australian wage growth is lukewarm, but the central bank is talking like it is hot. Japan and China have weak wage growth. Employment growth is holding up in most countries.

The question is whether continued strength in the jobs market will mean that the economies can plow through the effect of higher interest rates.

Jobs data is not all sunshine and roses. You can paint some "glass half empty" stats:

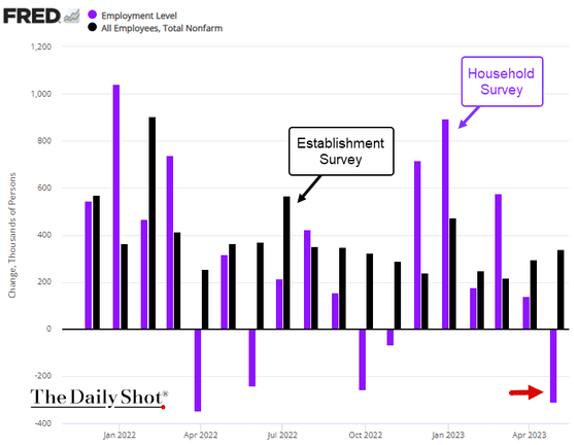

In the US, household survey of jobs looks much worse than the business survey

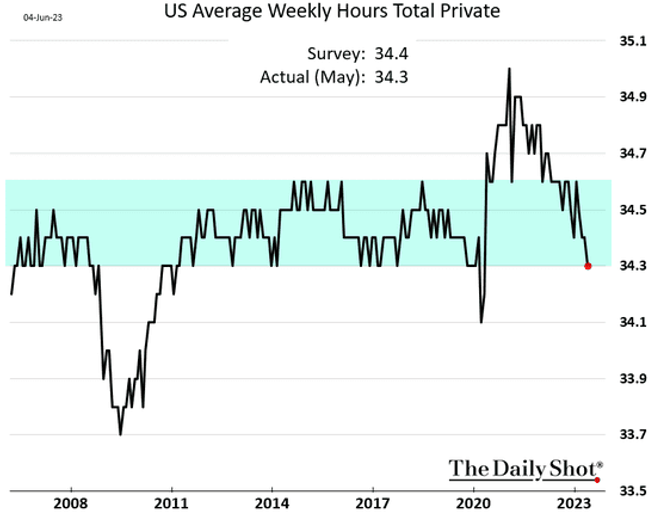

Announced layoffs are high. The number of hours worked is at the lower bound of prior ranges:

Australian job ads are down 20%+ on last year. Many other markets are showing similar trends. This is what I would expect to see in a typical cycle, the forward jobs indicators turn down, and then jobs follow a few months later.

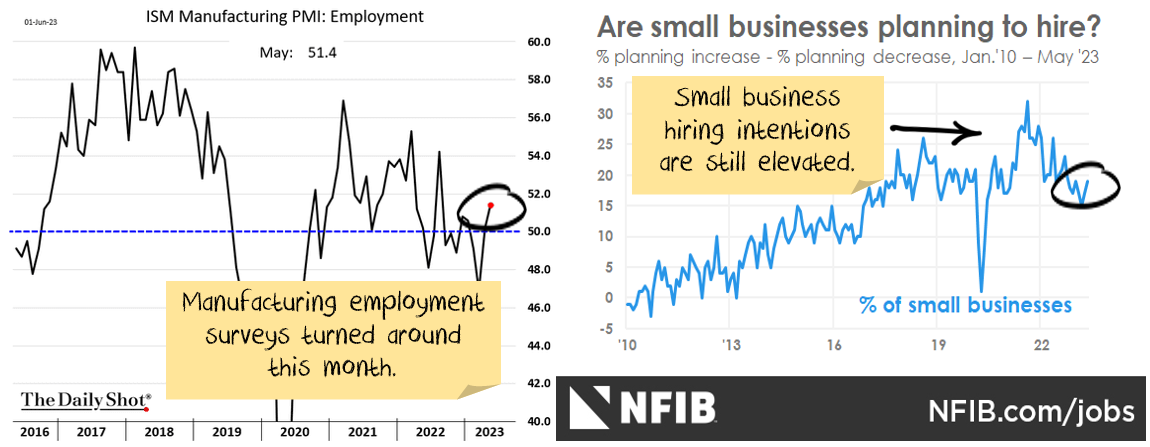

Then again, there are some "glass half full" signs as well that jobs might stay strong:

Is something different this time? Or is it merely a sign that jobs and inflation are following their typical path and are lagging the cycle? The second explanation still seems the most likely.

Is the Reserve Bank of Australia boxed in by immigration?

Australia is running record levels of immigration. Governor Lowe made the point in recent testimony that this is contributing to inflation as infrastructure and housing can’t keep up.

What he didn’t explicitly connect is that interest rates work best to cool demand. Australia is suffering from supply-side issues in two ways:

- Immigration will keep wage growth down as the supply of labour booms.

- Immigration creates demand for housing, but supply in housing is not flexible and will take years to catch up.

Then, energy prices in eastern Australia remain incredibly high by world standards. Whatever policies the government are suggesting it will put in, they aren’t working.

Raising interest rates does not fix either problem. Except if rates rise so high that something in the Australian economy breaks. Which seems to be the plan at the moment.

Could the forward indicators be wrong?

Sometimes, it is different. The forward indicators signal a problem, but something intervenes, and the potential problem doesn’t progress into an actual problem.

The latest market hope centres around artificial intelligence stocks. The short version is that a nascent boom is going to drive spending and productivity to offset the higher interest rates. I have two problems with this view:

- A productivity boom will come. But there simply isn't enough time. The improvements will occur over a decade, not six months.

- It is simply not big enough. Total global spend on artificial intelligence last year was around USD 100 billion. About 0.25% of GDP. If that tripled overnight, you are still only adding 0.5% to GDP growth.

The bond market believes the forward indicators, it has a recession by the end of the year. Equity analyst forecasts do not:

And the stock market is priced for a boom, not a bust:

Credit Crunch

A banking crisis has been playing out over the last few months. I'm still not expecting the banking crisis to create major issues. But, I am expecting the credit crunch following the banking crisis to create major issues. So, it is a question of “when”, not “if”.

I’m expecting bank funding costs to increase. Deposits to flee the smaller banks. Both have already started.

As a consequence, banks scale back their lending. Interest rates charged are higher. Corporates bear the brunt, the US falls into recession and default rates spike. Inflation is no longer a concern.

Net effect: a mini-banking crisis, followed by a credit crunch, possibly followed by a traditional banking crisis.

The forward data continues to indicate economies are in the early stages of a credit crunch:

Earnings are still too high.

One of the key features of the last year has been the ability of companies to expand margins, using inflation as a cover to push through price increases. But that is coming to an end.

Sales growth remains relatively good, but this is largely a function of inflation:

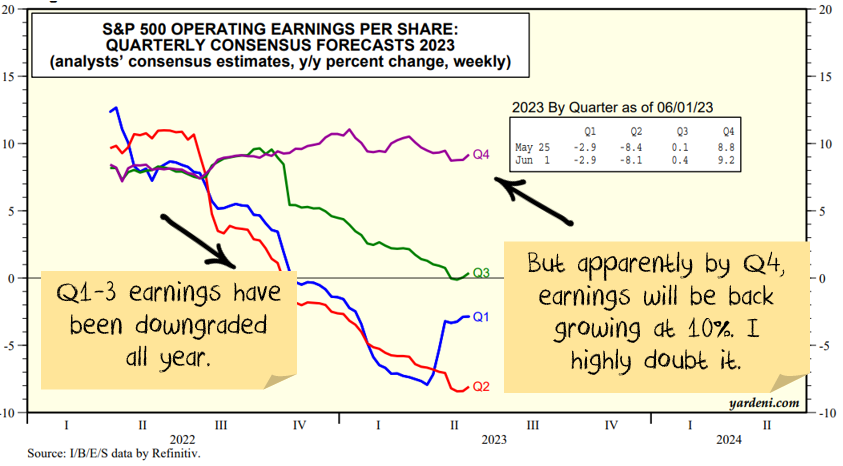

Analyst forecasts are still too optimistic.

Add in that a host of forward indicators (soft data) are pointing to significant weakness. Capital expenditure intentions, financial conditions, CEO confidence, sector downgrades all point in the same direction. Earnings forecasts are too high.

Is something different this time? Or is it just that analyst forecasts are too optimistic at macro turning points, as they usually are. My money is on the second.

China finally holding its nerve?

China is in the middle of its fourth attempt in the past dozen years to wean itself off its property construction addiction. They lost their nerve on three prior occasions.

In November, China issued a sweeping directive to rescue its property sector. At face value, it was a major recalibration of its property crackdown. We did not interpret the announcements as a resumption of the property building boom. In fact, for the most part, you can categorise the elements as either (a) directives to various banks to lend more to developers, mostly focussed on completing existing projects (b) reduced debt constraints or rules on individuals buying houses.

The plan is to avert catastrophe rather than return to the old normal.

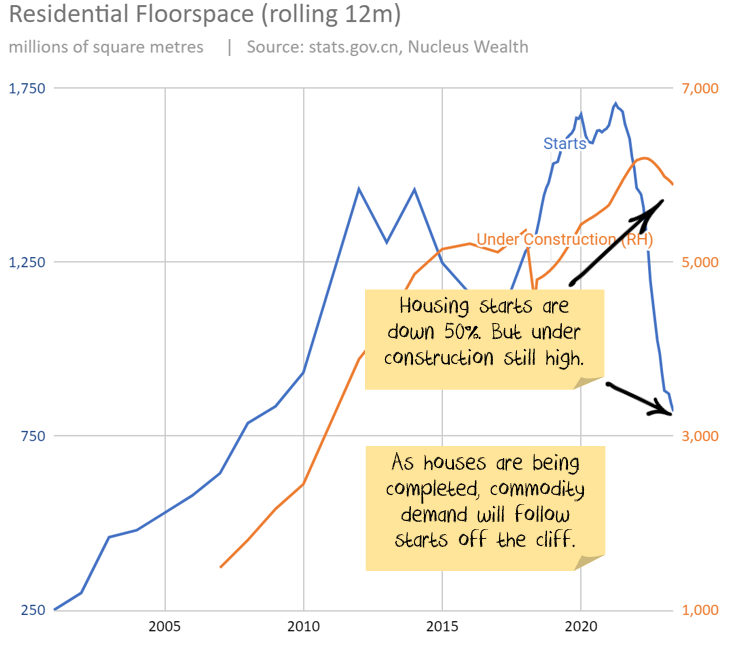

China's housing starts are down 50% on prior years. But, because apartments take a long time to complete, the amount under construction has only fallen slightly:

The reduction in new housing starts will eventually flow through to construction. And, given the immense size of the Chinese house-building bubble in recent years, starts would need to halve again to get down to levels that are consistent with other economies.

China is not coming to the rescue through housing and infrastructure. Stimulus, if it comes, is much more likely to be focused on renewable energy and semiconductors. Particularly as the US expands the number of advanced chips that China has been cut off from.

Australia was a major beneficiary of Chinese construction through commodities. That is not the case for semiconductors.

Net Effect

The credit crunch is growing, bankruptcies are climbing, company earnings are sliding lower, and China is not coming to the rescue.

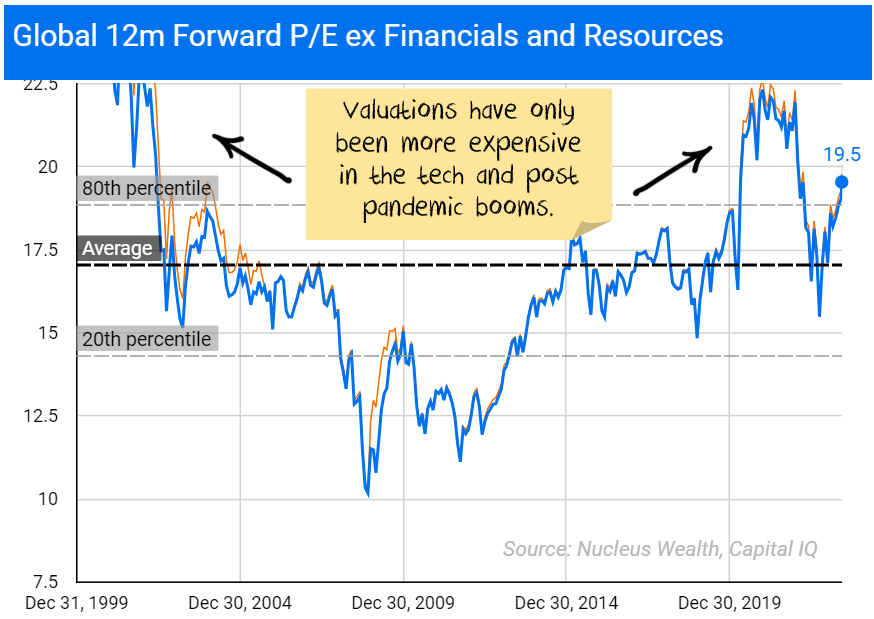

Valuations are in the most expensive 20% of historical ranges. None of those factors encourage me to buy more stocks.

Jobs are the lone bright spot. They are usually the last domino to fall, so it is not atypical at this point in the cycle to see jobs yet to weaken. But the continued strength of jobs and wages is the one factor that bears could prove bears wrong.

Investment Outlook

I have some pretty clear ideas about which trends are sustainable and which ones aren't in the long term. However, the short-term is far less clear:

- The banking crisis is morphing into a credit crunch. This is the number one issue over the next few months.

- The sanctions on Russia are unlikely to be lifted anytime soon. The short-term effect was commodity shortages. In the longer term, it seems likely that we will see a re-orientation, Russia will supply more to countries like China and India, less to Europe. For some commodities (oil, wheat) this will be easier. For others (gas) it will be extremely difficult.

- The geopolitical energy crisis in Europe has eased on the back of much warmer weather. Australian energy price caps have pushed down energy prices. There will be a rush to alternative energy sources in the mid-term.

- Supply chains continue to improve.

- Governments continue to withdraw (or not replace) stimulus. There will be a fiscal shock into 2023. The question is whether the private economy will be strong enough to withstand it. Leading indicators suggest profits will be lower.

- Central banks have made it clear that they will try to solve the Russian-induced energy issues and supply chain-induced inflation by raising interest rates. The odds of a policy error have increased significantly.

- China still has not bailed out the property sector. Last year's changes are not a bailout... but they may morph into one. China is trying to ensure that houses under construction get built, small businesses have access to credit, infrastructure building continues, and failing developers do not crash the economy. China is yet to show any signs of turning back to the old days of debt-driven property developer excesses. In the short term, commodities have been booming. If China doesn't continue to roll out new measures, the commodity market will deflate again.

It is still not the time for intransigence. Events are still moving quickly. But we have positioned the portfolio towards the most likely outcome and are gradually increasing the weights as more data arrives.

Bond yields have risen significantly. If the world heads for a recession this is a buying opportunity. In the short term the narrative "high inflation, central banks raising rates = sell bonds" seems to be coming to an end. Although there may be another last hurrah as the US central bank looks to rein in the stock market optimism.

The mix of higher volatility, leading to deleveraging of risk parity trades and momentum means yields could yet go higher. We are invested for bond yields to reverse.

Asset allocation

After being very expensive for a number of years, stock markets are now merely expensive. Debt levels are extremely high. Earnings growth had been really strong but has come to a halt. There are signs it is starting to reverse.

Markets are supported to a great degree by central banks and governments. Policy error is every investor's number one risk.

But, any number of other factors could force this off course and see unexpected inflation. COVID mutations could disrupt supply chains again. Chinese/developed world tensions might rise further, leading to more tariffs. Or, China might decide again to supercharge property investment.

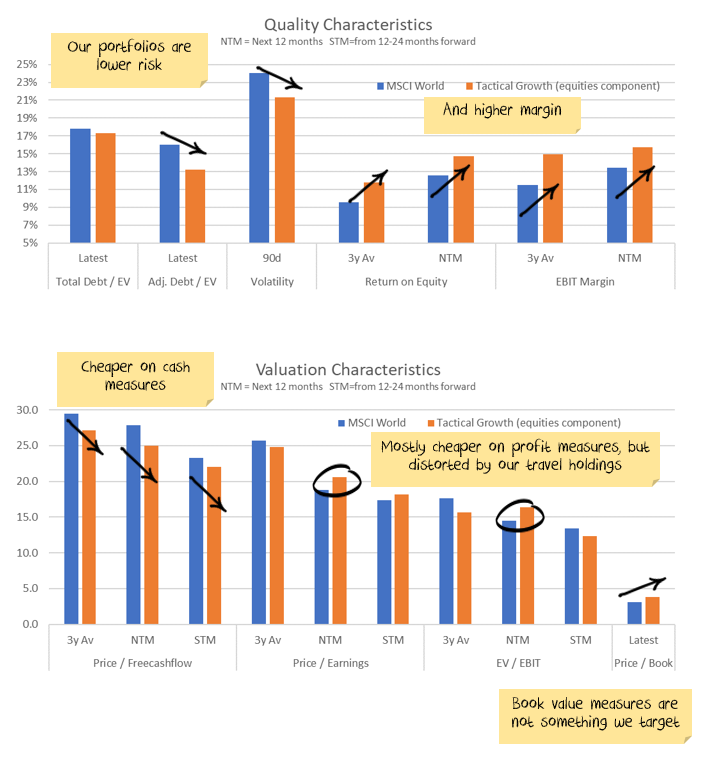

We are significantly underweight Australian shares, and as noted above, overweight bonds, with the view that the Australian market is more quickly affected by rising interest rates and more affected by a global recession:

Performance Detail

Core International Performance

May saw global equities recover from an initial sharp decline. Our portfolio outperformed the benchmarks most of the month but the end-of-month NVIDIA inspired rally overtook us at month's end. Regionally Europe was the key detractor as Luxury Goods retraced some recent strong gains. The strong interest in AI which followed the NVIDIA revelations meant our Software/Internet Hosting exposures were key drivers of this month's performance. The weakening AUD versus the USD helped returns from the US but otherwise currency detracted. With the strong Tech performance we trimmed some of our exposures, reinvesting in some Pharma stocks.

Core Australia Performance

Australian equities were on the back foot all month with falls accelerating. Our tech exposures were caught up in the AI driven resurgence but commodities and defensives suffered. This month we took some profits from our gold exposure replacing it with a Nickel/Lithium miner (IGO), exited Qantas and used the funds to upweight some defensives and Xero.

Portfolio Yields

This month we have added a table showing the income yields of our various portfolios, including their proportionof Franking and Foreign tax paid over the past 12 months. We also include an estimate of forecast yield (next 12 months), assuming no change in current tactical allocations and stock composition. Most portfolio yields are expected to rise with greater income contribution from cash and bonds with the global interest rates rises. However, Australian equity yields may fall as commodity-driven mining companies are expected to have lower profits to pay out. Our underweight Resource position in Core Australia portfolio should help maintain its yield.