November saw equity market returns surge on the back of US election result clarity and positive news from a trifecta of COVID19 vaccine results. Markets broke many global records and the US equity indices hit new all-time highs as the vaccines fuelled the rotation into cyclical stocks and regions as well as providing a boost for downtrodden Value stocks.

Six months ago we expressed that the most likely reason for us to miss the upside is if capitalism was successfully suspended, companies and individuals were prevented from going bankrupt and government/central bank stimulus exceeded the hole left by the pandemic.

Capitalism was suspended. And is still suspended. We are now operating under the assumption that it will remain suspended for 2021 if not longer. The scale of stimulus measures now underway are notoriously difficult to reverse. Fiscal policy remains a strong tailwind. Monetary policy is committed to seeing the whites of inflation’s eyes. The pandemic has removed all policy restraint.

If there is no end in sight end to any of these factors, and excellent vaccine results are only going to extend the market's willingness to look past short-term issues, then it is time to position for 2021 upside and we have begun that process.

*****

The 2021/22 profits boom

The biggest opportunity is in company profits. There are three angles to our positive view.

Microeconomic angle

Many companies ceased non-essential spending and laid off staff shortly after lockdowns began.

Typically, during a crisis companies shed the least productive assets and staff, which raises the overall productivity of the company. The productivity increase is however masked by falling sales in the initial stages, and then only appears once sales recover. Often this means that profits recover faster than sales - and we expect this to occur this time.

This is not evenly distributed and tends to favour Value and Cyclical stocks.

Macroeconomic angle

You can look at three parts of the economy being corporates, households and the government. Corporate profits are an outcome of the interactions between the other two parts of the economy.

If we make the assumptions over the next twelve months that

- government spending is going to stay high and interest rates very low then

- the household saving rate (which is very high at the moment) will fall relatively rapidly over the next year.

The result is that the money has to go somewhere and the only place left is corporate profits (technically the money can go offshore, but if we are looking at global equities then this ceases to be a problem).

The 2021 catch-up boom

The third bullish angle is the unleashing of global catch-up growth. The global economy is still operating 8% below capacity. As vaccines roll out, this output will return in a rush, in addition to any added growth. We have already seen this in China where beating the virus combined with a moderate stimulus to trigger boom conditions in recent months. This will come to developed economies next.

There is also a typical post-recession cyclical inventory rebuilding cycle underway globally that will run all of 2021.

These three angles suggest to us that there will be a catch-up profits boom in 2021/22 that mitigates expensive stock prices in the medium term.

*****

The biggest short term threats

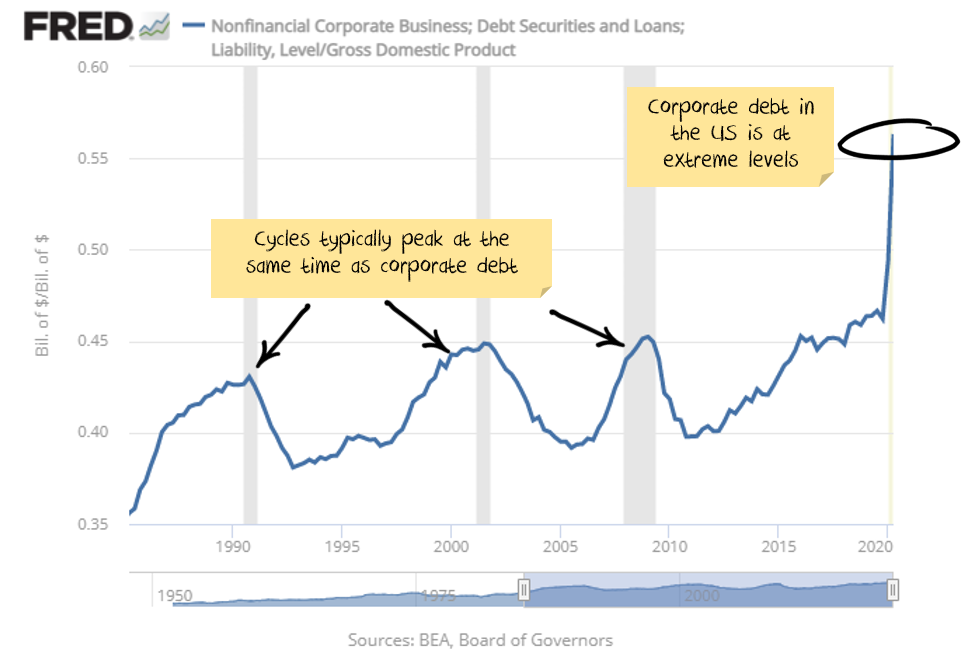

Major Short Term Threat 1: resumption of bankruptcies

Corporate debt was already very high before COVID-19. Now it is even higher, and there are no extra profits to support the debt:

Most countries started with a three-month suspension of bankruptcy rules. That became six months. Then a year.

In many countries, this also extended to consumers, either through preventing evictions or allowing interest payments to accrue.

Now, with a vaccine imminent, we expect the rules to be suspended for longer. Maybe six months, more likely to be all of 2021. If this doesn't happen then there could be significant economic fallout.

Net effect: the odds are low that bankruptcies will resume in the short term. We expect politicians to use the cover of an imminent vaccine rollout to maintain the status quo.

Major Short Term Threat 2: policy error

Either central banks or governments. At the moment central banks will not withdraw stimulus, so I won't go into too much detail.

Governments withdrawing stimulus too early is also unlikely, but in the US it is possible that if the Republicans win Georgia that they suddenly rediscover a thirst for balanced budgets. The $900b stimulus package currently transversing through the government should be enough for the first six months of the year.

Net effect: the odds are low of policy error.

Short Term Threat 3: low genuine credit growth

Since the 2007 crisis, much of the world economy has been driven by credit growth. If this disappears then we have to rely on productivity, wages and consumer demand. None of these has been strong for years, and it is difficult to see what will change that beyond the short-term benefits of cyclical recovery.

We can see government debt growing quickly as Modern Monetary Theory edges into mainstream policy and central banks increasingly monetise it. It is more difficult to see how corporates can borrow more but so long as the rules are suspended then it is always possible for the purposes of capital management. Consumers are in worse shape with Europe and Japan struggling to stimulate borrowing for years. The US is much better placed. Australia has short-term scope of lower savings but will struggle to lift household borrowing henceforth.

This means the weak productivity, wages and consumer demand will take effect before too long. The most likely outcome is thus continued increases in government debt, some increases in corporate debt. Household debt is an open question.

Short Term Threat 4: a new virus variant

Recent days have seen a new virus variant appear in the UK. So far, the scientific consensus is that vaccines will remain effective against it. But it does remind us that once the vaccine rollouts reach critical mass, natural selection will favour mutations that dodge them.

Other Short Term Threats

- Virus shutdowns: While there are significant shutdowns across the Northern Hemisphere, markets have had ample time to price these in.

- Valuation: Markets are expensive on any near term growth measure.

- Unemployment: typically is slow to recover, which means weak demand.

*****

Beyond the catch-up, a zombie lurks

In many countries, “extend and pretend” has replaced the threat of bankruptcy. Someone who can’t pay their rent is not evicted but allowed to accrue debt. Don’t foreclose on those who can’t pay their interest. Instead, build up their interest payments into a larger debt burden.

The end game will be a cohort of zombie consumers and businesses. Weighed down by debt burdens too massive to ever pay off, but supported by interest rates low enough to keep them from defaulting.

US Treasury Secretary Mnuchin is letting several minor lending programs expire at the end of the year, to the loud complaints of many – including the US central bank. Many programs will likely be re-instated once Biden is in power. In other countries, there is very little consideration being given to finishing similar programs.

In short, policymakers have decided on zombification: limit bankruptcies; increase debt and never raise interest rates again. It doesn’t make for a healthy economy. But it limits short-term pain which appears to be the current goal of every politician.

This zombification is inflationary in the recovery phase but deflationary soon afterward as oversupply swamps demand. We are, therefore, suspicious that beyond 2021/22 we are entering a new inflationary cycle, as some have posited. The Value stock rotation lives and dies on this narrative. It can continue with inflation and rising market interest rates or end without it, culminating in a return to Growth stocks. We are positioning for a run to Value that lasts for 6-12 months. For it to continue, we will need to see more policy innovation, especially the putative integration of fiscal and monetary policy worldwide.

The pandemic has pushed fiscal and monetary policy closer together with a whole range of developed economies now using central banks to monetise public debt. This will reach a short-term crisis test in the Georgia senate run-off in the US in January. If the Democrats win then that integration is likely to accelerate towards a truly MMT future in which central bank funded debt forgiveness and styles of universal basic income become the norm. If not, then we see this process slowing down and, beyond a short-term catch-up and commodities boom, deflation and Growth stocks will return to the detriment of Value.

*****

Performance Detail

Stocks opened the month strongly, climbing throughout US election week as bargain-hunting followed a weak September and October, then accelerated with the triple announcements on excellent COVID19 Phase 3 trial vaccine results from Pfizer, AstraZeneca, and Moderna. Stocks that had been hurt by economic lockdowns surged on the news, while the stay-at-home stocks suffered steep declines. Bond yields and oil prices both moved higher on expectations of increased economic activity. The month was unique in that Global Value stocks returned 15.1%, outperforming growth, which returned 10.9% while in fixed income it was the riskier high yield and emerging markets that outshone the higher quality markets. Domestically the ASX 200 especially benefitted from the rotation into Cyclicals given the weighting to Financials and Resources. After a strong performance, by the end of the month, the ASX 200 had scraped into positive territory for the year (+0.2%).

This rapid rebound in the equity markets over November caught our defensively positioned portfolios by surprise. We consequently underperformed our Benchmarks as risk-on meant Defensive assets suffered. Core portfolios made some gains but we were underweight oil, Cyclicals and long gold. Currency proved a headwind for all portfolios with the weakening USD as it lost some of its recent safe-haven shine and AUD benefitted from the risk-on sentiment.

For us, the November miscalculation was not so much the election, but the rapid progress and high efficacy of the new vaccines and the market’s aggressive discounting of the contemporaneous third wave Atlantic pandemic. We had looked for markets to sell the new lockdowns in some measure but they went the other way.

Consequently, we undertook moves to increase our Tactical allocation to equities and repositioned our equity portfolios to benefit from a vaccine roll-out.

*****

Core International Performance

Our international portfolio saw a 2.7% gain over November but underperformed its benchmark, reflecting our underweight Cyclicals position. The underperformance was more pronounced in our US stocks where our overweight Technology and Pharmaceuticals suffered from the sectorial rotation and our defensive underweight oil and overweight gold proved a further detractor. The rising AUD continued to be a headwind on performance, especially versus the weakening USD.

During the month, we switched HP for Intel and picked up some Visa, a quality financial stock that had finally moved into our buy range. Post the vaccine announcements we took some positions in stocks with travel exposure (Southwest Airlines, Booking.com, Expedia) that we expect will be early benefactors of a resumption of travel. We also took profits in an energy stock (Vestas Wind) that has done very well for us but is trading at lofty multiples; and exited some of our COVID19 defensive stocks (Essity, Gilead Sciences).

*****

Core Australia Performance

The Core Australian portfolio saw a small gain over the month but our underweight resources and banks meant we didn't capture the strong rise in the ASX. The strongest performers in the index were energy (28.5%), financials (16.1%) and industrials (12.3%). Nearly all sectors had positive returns for the month, with the only exception being consumer discretionary (-0.7%).

Toward the end of the month, we repositioned the portfolio to increase energy-related stocks (adding Woodside, Worley) and travel-related stocks (Sydney Airports, Qantas, Flight Centre). We down-weighted defensives, removed AGL, Ramsay Health Care and Medibank and took profits in our Coca Cola which is currently subject to take-over.

Some of these Cyclicals have since pulled back but we are comfortable that they are the play for the 2021 catch-up profits boom so will add more on the dips.

*****

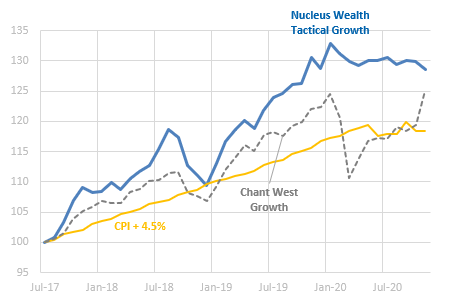

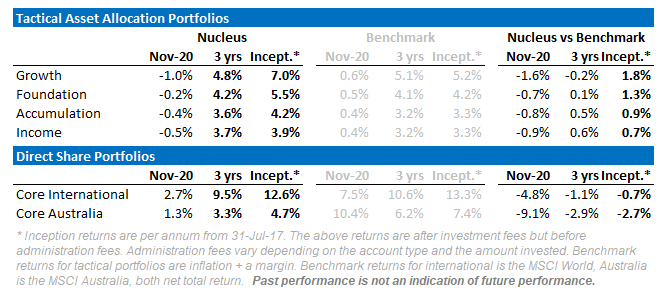

Tactical Portfolio Performance

The performance of the Tactical portfolios over November reflected our defensive stance leading into the uncertainty of a contentious US election and rising COVID19 second/third wave dynamic in both in the US and Europe. The bad news (and good news!!) is that events proved us wrong with a seemingly clear-cut US election result and the early release of effective vaccines giving markets hope of a rebound in 2021.

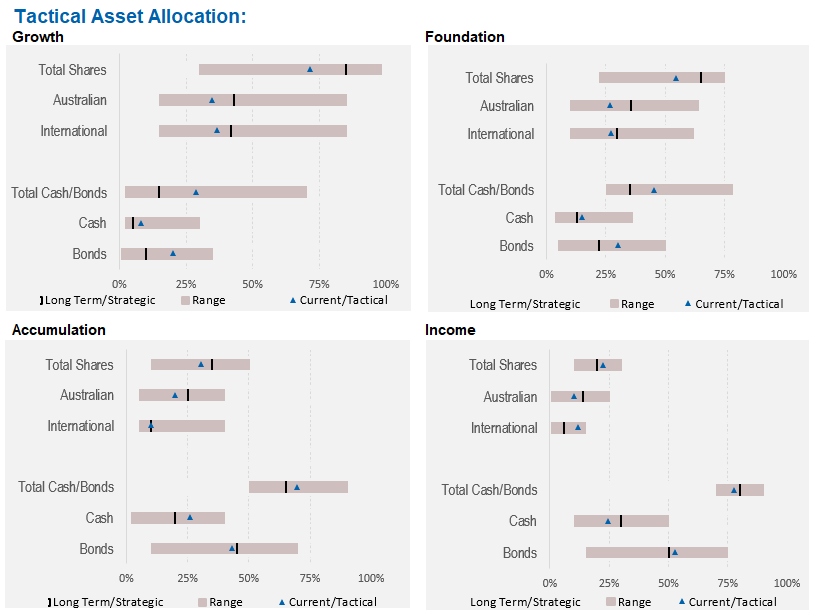

Over December we repositioned the portfolios, decreasing our USD exposure and increasing our weighting to both domestic and international equities. We also enacted the stock changes we have mentioned in the Core portfolios above. In the Growth portfolio, we have gone from a 60:40 Bond: Equity mix to a 30:70 mix to capture the 2021 catch-up growth profits boom. In the Income portfolio, we added some domestic equities which hereto now we had avoided. However, we remain both cautious and vigilant on developments.

Reflecting upon 2020, annus horribilis, I am pleased that we preserved investors from much of the COVID-19 pain. As the year draws to a close, we have missed some recovery upside but caution was warranted given the unprecedented nature of the virus risk.

We can now look forward to a much better 2021 and are positioning for good early-cycle recovery returns.

Whether this can evolve into a longer and more robust cycle we have our doubts. Aware, as always, that although risk can be suppressed it cannot be eliminated, only transmuted, hidden or shifted.

The pandemic is no different.

__________________________________________

Damien Klassen is Head of Investments at Nucleus Wealth.

Follow @DamienKlassen on Twitter or Linked In

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Nucleus Advice Pty Ltd - AFSL 515796.