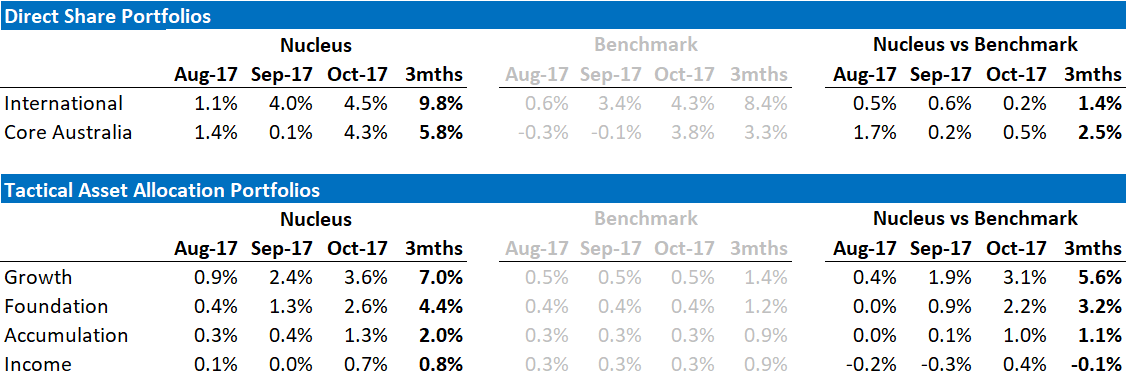

One of our core investment themes is that international stocks are the best asset class for Australian investors at this point in the cycle. To date, this has been the right call, with our international portfolio increasing almost 10% over the last 3 months on the back of a weak Australian dollar, favourable stock selection and strong international markets.

The question going forward is whether its time to switch to a different asset class. At this point, the answer is still no. There is still significant scope for the Australian dollar to fall, and while share markets are getting expensive the risks appear manageable for the moment and so we are maintaining our overweight international share / underweight Australian share stance.

Having said that, at the margin we are taking risk off the table – we are not currently re-investing cash from our dividends and we are looking to trim a few positions that have run particularly hard. Additionally, during October, our bond positioning started to bear results, reversing most of the losses from August and September. We continue to expect bond yields to reduce as inflation and wages growth remain low.

At the bottom of every post, ASIC requires us to say “Past performance is not an indication of future performance” – and we would re-iterate that for September/October – 4%+ per month should not be your expectation for performance. But it is a reminder that markets rarely make steady gains, they often make little headway for long periods before moving rapidly. Our take continues to be that investors need to position their investments early rather than trying to be too cute timing the market.

Source: Linear, Factset

Source: Linear, Factset

The returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees.

The Way Forward

As a reminder, we look at the key themes facing our portfolios as being:

- China: Rebalancing is occurring, the question is how fast Chinese authorities allow it to occur

- Trump: Taxes are the next key decision point, and after failures in healthcare he is looking for a win. We are expecting there to be 2 facets – tax cuts and encouraging companies to bring back cash. Both are USD bullish.

- Europe: Grinding recovery. We are not expecting great things, but note that the number of political risks has reduced in recent months. The major long-term issue is still the significant imbalances between Germany and most of the rest of the Eurozone, but no real flashpoints at the moment.

In China, we saw a number of speeches and new data points.

The most important came from the Chinese National Congress, where, in a deviation from past speeches, we saw no new growth targets. Our view is:

- the shift to consumption-led growth rather than investment-led growth will require a greater shift than many recognize. This shift will be a significant negative for commodities/the Australian dollar

- current growth rates are unsustainably high, inflated by rapidly increasing Chinese debt. The increase in debt has been required in order to hit the growth targets, so removing the growth targets will help refocus local party officials to more sustainable policies

- Activity still seems to be slowing, although the next few months are going to be more difficult to get an accurate read on economic activity as the Communist Party Conference in Beijing has led to the shutting down of a considerable amount of industrial manufacturing, in particular, steel production. We would expect that some of the strong commodity prices in July/August reflected the bringing forward of production in front of the shutdown. Then, the weakness in September represents the shutdown, which we expect to continue for the next couple of months. Finally, there is likely to be a bounce in Q1 2018 due to “catch-up” production. So, the true trajectory is going to be difficult to ascertain accurately until we are through this period.

- we are probably 6-12 months away from being able to see whether the removal of growth targets makes a big difference or not – they have the potential to foreshadow a seismic shift to a more sustainable growth model. I suspect the outcome will be that with the Communist Party Conference done now the impetus will switch to slowing the economy as much as possible, but with any sign of unrest, the debt taps will be turned back on.

In actual data releases, Chinese credit remains unsustainably high, although it slowed a little in September data. GDP statistics were out, with the September quarter numbers growing at 6.8% - in line with most forecasts. Within the GDP we did see a shift to higher retail sales and lower investment which is a step in the right direction. We expect GDP to continue to fall and a continued shift to consumer-led growth vs investment growth.

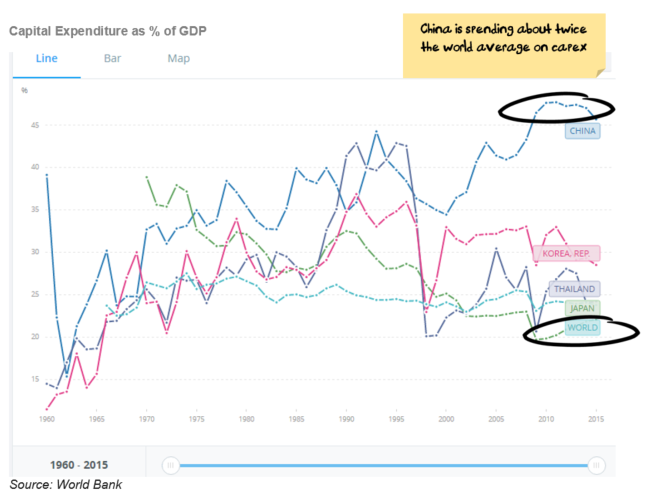

Our expectation is that China is going to continue to “glide” lower to try to normalize the capital expenditure to consumption in-balance:

It is our view that the Chinese economy will continue to slow over the coming years – Japanese style lost decades, and low inflation/deflation remain more likely than a dramatic bust, which means a grind lower for commodities and the Australian dollar.

Our portfolio positioning on this basis remains:

- considerably underweight Australian stocks from an asset allocation perspective

- underweight resource stocks within equity portfolios

There was lots of noise but still little detail to assess on the Trump taxes.

Our core position is that Trump is trying to engineer a boom. It will not be sustainable and will likely be followed by a bust that leaves the US economy in a worse position but that is a future problem – positioning the portfolio for the boom is the current issue.

The proposed tax cuts are badly targeted by giving most of the benefit to the rich and to companies, trickle down is unlikely to work, the tax cuts are unsustainable, and they are only a short-term “sugar hit” for the US economy, I understand all the negatives. But if it is anywhere near Trump’s promise then it’s going to be such a huge stimulus that you don’t want to stand in the way of it as an investor.

So, we continue to play the boom but keep a sharp eye on the bust.

Our portfolio positioning on this basis remains:

- overweight international stocks from an asset allocation perspective

- overweight stocks with US exposures – subject to valuation. The practical implementation of this has been buying non-US stocks that are exposed to the US.

Asymmetric Risks

When running portfolios that represent core holdings, there is a focus on capital preservation and risk control over chasing returns. Part of the portfolio construction process is an assessment of both the probable path and the potential outcomes – we are looking for investments where when we are right we profit, but if we are wrong the consequences are not significant for the portfolio.

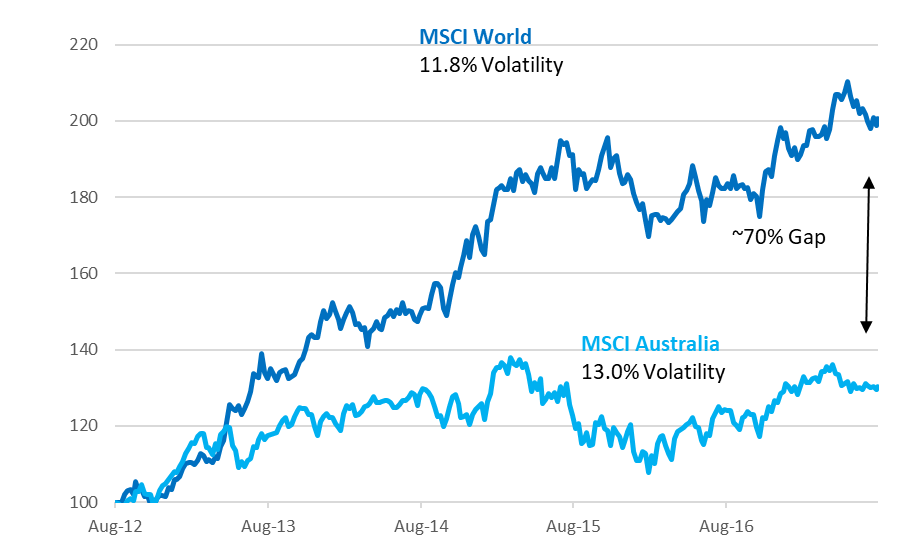

With that in mind, we continue to treat international equities as holding the best risk/return equation. If share markets continue to grind higher then we expect international shares to do better than Australian shares (mainly on the back of a better earnings profile) but when share markets retreat on increased risk we tend to see the Australian dollar also falls which offsets any losses on international stocks.

What this has meant over the last five years is that not only have international stocks significantly outperformed Australian stocks over the past five years but that they have done so with less volatility.

Source: Factset

Source: Factset

Now, I hasten to add that this is historical and relationships do change. But this is not a relationship that we expect to change over the next few years.

Tactical Asset Allocation Portfolio Positioning

In our tactical portfolios, we own cash, bonds, international shares and Australian shares.

The broad sweep of our asset allocation over the last 12 months was to ride the Trump Boom, switch into Europe in March / April as the US became overvalued and then switch back into the US as the Euro rallied and the USD fell.

We remain underweight shares in aggregate, but that headline view hides the underlying exposure – we are significantly overweight international equities and significantly underweight Australian.

Over / Underweight positions by portfolio

Source: Nucleus Wealth

Trading was very limited in October. There are a number of successful positions we are considering exiting, but we continue to struggle to find viable replacements.

International Equities

In our direct international portfolio, markets are expensive, returns look low, and risks are building. So, for the most part putting together our international portfolio, it has been about finding novel ways to get the exposure that we want.

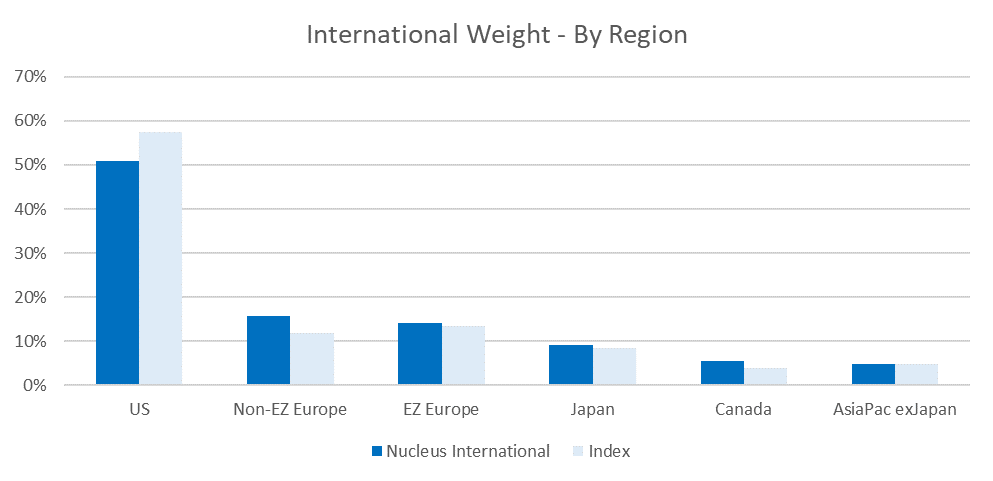

Country Allocation

Based on growth and relative valuations, we are country agnostic at this point, if the USD keeps falling we will be looking to pick up more US stocks – that is the market where the growth remains the highest but valuations are more expensive.

While “technically” we are underweight the US, many of the stocks we own in other markets have significant exposure to the US. Basically, we are finding stocks listed in the US to be relatively expensive, and so we have been looking to other markets to find stocks that are exposed to the US at a cheaper price. For example, Unilever is a UK listed stock, but Unilever’s actual sales exposure to the UK is only a little over 5% – its biggest markets are actually the US and China. Vestas Wind is listed in Denmark, but the US is its biggest market.

We have been hunting for value in non-Euro European markets in particular.

Industry Allocation

Our biggest call is underweight energy. In particular oil producers. We have blogged a lot about the oil price, but the thumbnail sketch of the sector is that:

- the short term is not positive for the sector with oversupply and OPEC needing to cut production to try to prop up the oil price.

- the long term is not positive with increasing electrification of cars and falling battery prices limiting the upside

- the mid-term might be good if an undersupply emerges and before electric cars put a dent in oil demand and assuming US shale costs don’t keep falling

Meanwhile, oil stocks are pricing $60-$70 oil prices in perpetuity. The mid-term is going to have to be spectacular to justify current share prices, let alone getting any share price growth.

Having said that, it is a big risk to our portfolio being underweight energy. If there are geo-political ructions, particularly in the Middle East, we would probably underperform. October saw the oil price rise once more, largely on the back of hurricane-related supply constraints, but we remain comfortable with our holding and expect much of this to be a short-term issue.

Our sole holding in the energy sector, Neste Energy rocketed up over 30% in October, which made up for any potential underperformance from being underweight with a rising oil price. Neste is a Finnish oil refiner, and at its interim results during the month provided an upbeat assessment of its future prospects leading to a range of analyst upgrades. Additionally, Neste is making a significant investment in green technologies and is well regarded (usually the top energy company globally) by a number of sustainable ratings firms including being in the Global 100 most sustainable companies, the Dow Jones Sustainability index and CDP.

We have been overweight a range of automotive stocks and suppliers. This was largely a value play as most of the sector trades on low multiples over growth concerns. We spent a considerable amount of time looking through our holdings following strong performance in September looking to replace some of the stocks that had increased the most. However, we are struggling to find stocks that offer the right mix of value and growth and so haven’t pushed the button on any of the trades yet.

We are underweight financials – mainly as we can’t find US financials that are cheap enough to justify purchasing. We have been trawling the European banks for value, and October performance was led by Singaporean bank DBS Group which rose 12%. There was some bounce back in insurance company share prices after a hurricane affected September.

We have a reasonable tech / IT exposure. Apple continues to attract the lion’s share of the press and rose 12% in October. We are still looking at its 4th quarter results (released this morning) but the stock hit new highs following the result suggesting the market approved.

There are a number of smaller tech stocks that we own, in particular, a range of semiconductor stocks where we like the growth outlook. It is worth noting that part of the reason for Apple increasing the price of its latest phone is an increase in memory and components. This is a positive for semi-conductor stocks more generally, especially if a “feature war” breaks out in the smartphone space. We current hold a range of stocks that should be helped by this trend (Lam, Applied Materials, Skyworks, and to a lesser extent Cisco).

Defensives are expensive. REITs, Utilities, Telcos and Infrastructure are the usual places to look for defensive exposure but (just as the central banks intend) lower risk investors continue to “shuffle up the risk spectrum”, and they have bid the price of traditional defensive sectors to levels that make investment difficult.

So, again we have positioned the portfolio to benefit differently. We are looking for a mix of the more stable industrial, consumer staples and healthcare stocks to get a similar defensive exposure without having to pay the nosebleed prices in the traditional defensive portfolios.

Click the below for a heatmap of stock performance in September:

Source: Factset

Source: Factset

Australian Shares

The Australian share market had a stellar month. In our portfolio 29 of the 30 stocks in our portfolio rose. We are not expecting this to continue.

Source: Factset

Source: Factset

Once again, our underweights to resources and banks and our overweights to internationally exposed industrials saw the portfolio beat the market return, this time by 0.5%.

We are underweight both banks and resources, and given the highly concentrated characteristics of the Australian market, we are overweight just about everything else.

We are only just managing to keep a number of the international stocks in our portfolio - on a valuation basis Treasury Wines, CSL, Cochlear are all getting expensive after performing well.

As we are limited to the large capitalization stocks, we are struggling to find viable replacements.

Epilogue

In summary, our view continues to be that Australian investors are better off holding international investments at this point in the cycle. The past thee months have obviously taken a big step in this direction, with international stocks providing almost 10% in just three months. We believe this has a lot further to run, but it is unlikely to move in a straight line.

Our intention is that our portfolio is positioned to take advantage of our key themes but minimise risk in the event that our themes take longer than expected to resolve themselves.

We usually find that big picture macro themes take a long time to resolve themselves in financial markets, but when macro theme resolve themselves they do so quickly – usually too quickly to reposition your portfolio if you are not already invested.

Register your interest now (if you haven't already): Damien Klassen is Head of Investments at Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.