eSports are sexy, but expensive

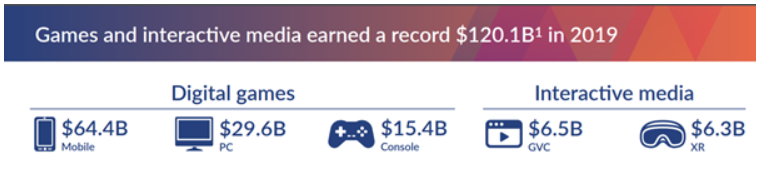

The digital games and interactive media sector is probably much larger than you think and still growing. To put it into perspective, one of the highest rating movies ever, Avengers: Endgame, grossed US$858m during its opening weekend. Grand Theft Auto V's release, earned US$1b in just over three days.

Originally just a PC/console experience, ubiquitous smartphones are now raking in cash as well. And, it is important to clarify, the phone market appears to be a complement to the PC/console experience rather than a competitor.

Source: Superdata

What is driving the growth of gaming?

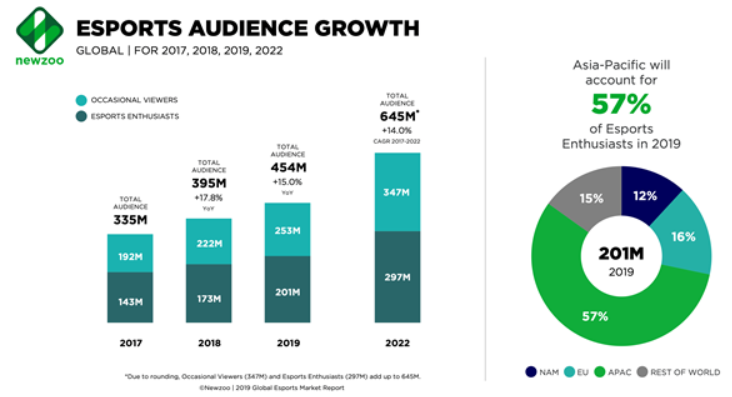

- The emergence of eSports. The global eSports audience grew to 450m worldwide in 2019, up 15% year on year. And this was before coronavirus forced half the world indoors. Kids under 20 are more likely to be watching esports than live sports. League of Legends tournaments routinely beat most traditional sports in viewership numbers.

- The move to mobile. Historically Digital games were the preserve of PCs and then Consoles. Today mobile games generate almost twice the revenue of PC and Consoles combined.

- Broadening of the Demographics. There's a stereotype that the only people who play videogames are adolescent boys. The move to Smartphone gaming has seen games like CandyCrush, and Words with Friends effectively raise the average age of users to around 35. Additionally, women now make up almost 50% of overall gamers.

- Evolution of the business model. Initially, game designers pursued a traditional software purchase model with dollars paid upfront. More recently, free-to-play games which have no upfront costs but use in-game purchases (for decorative items like skins), known as "microtransactions", to generate revenue. Microtransactions accounted for four out of every five dollars spent on digital games in 2019 thanks to strong performances from mobile games like Candy Crush Saga, Honour of Kings and Fortnite.

- Geographic trends. More than two-thirds of digital gaming revenue is generated in Asia. The increase in affluence in China and Emerging markets is another key driver of continued growth.

Australia's largest gamer

There is a dearth of investment options for Australian investors in this space. If we exclude microcaps (under $50M capitalisation), the only real candidate is Aristocrat (ASX:ALL).

Aristocrat provides entertainment from casino-themed games such as Vegas Penny Slots or adventure games such as RAID: Shadow Legends. These are free to play but make money through in-app purchases. This shift to digital games now generates around 40% of its revenue. Recent comments from Aristocrat indicate revenues are up 20% due to COVID restrictions.

What is a gambling company doing developing games? Interesting that you should ask.

As I mentioned, a key driver behind the explosion in gaming revenue has been through freemium games, those that are free to play. Some examples of how these work:

- Fortnite is the world's most popular game. Ask any 11-year-old boy (and increasingly girl) if you haven't heard of it. Fortnite makes money from selling skins (different looks for characters) that have no impact on the gameplay. In other words, you pay to dress-up your avatar. In 2019 Epic games made USD 1.8b in revenue from Fortnite. Before the COVID lockdown.

- Counterstrike is similar. Knives that look different, but make no difference to gameplay sell for hundreds and sometimes thousands of dollars.

- Candy Crush is one of the most popular games for phones, with a higher number of women players. It is free to play, and you can share your progress with friends. And then you can pay to advance levels more quickly than you might be able to do through skill alone.

- Clash of Clans is another popular phone strategy game where you design a base which other players will attack, and you in turn attack theirs. Again, you can pay to advance levels more quickly than you might be able to do through skill alone.

The mechanics of getting paid as a game developer in this area is not dissimilar to the mechanics of getting paid as a poker machine developer. The longer you can get each player to play, the more money you are likely to get. Additionally, the majority of your customers earn you almost nothing, and a much smaller number deliver you most of your revenues. And just as importantly, the basis of gameplay is psychology. How to keep the player in the goldilocks zone: not so easy that they get bored, not so hard that they get frustrated. And how to space out the dopamine shots through rewards to keep the gamers gaming.

There is (disturbingly?) a lot closer links than you might think between gambling and gaming.

How else can you access gaming stocks in Australia?

Source: Newzoo

At the microcap end of the ASX market, several companies offer exposure to the gaming landscape. However, most of these are at a very early stage and are capital hungry. They should be regarded as options/ venture capital stage opportunities, not dissimilar to listed biotechs, where the risk to capital is high. i.e. you are more exposed to the success or failure of an individual game than you are to the growth of the entire industry. We only invest in large caps, so I haven't looked at these companies in any detail:

-

- iCandy Interactive (ASX: ICI) Mkt Cap $9M: Development and publishing of mobile games and digital entertainment for a global audience. iCandy Interactive runs a portfolio of mobile games that are being played by over 350 million mobile gamers.

- eSports Mogul Asia Pacific (ASX: ESH) Mkt Cap $29M: An esports media & software business with an initial focus on Australia, Asia and Latin America. At the core is an esports tournament and matchmaking platform, Mogul.

- Emerge Gaming (ASX: EM1) Mkt Cap $23M: an eSports tournament platform and lifestyle hub Arcade X.

- SportsHero (ASX: SHO) Mkt Cap $6.6M: a social media company engaged in the development of real-time fantasy sports app and social prediction platform 'SportsHero'.

What about international gaming companies?

For a pure-play exposure to this growth, investors need to invest in US-listed video game companies like Activision Blizzard, Take-Two Interactive, and EA.

For a more diversified exposure, you can get access through Sony, Google, Apple and Microsoft. All four of these companies have significant exposure to the growth of gaming. Even Amazon has a finger in the pie, hosting some of the biggest streaming events.

For a more targeted Asian focus investors could target some of the big Chinese stocks like Tencent Holdings. But buyer beware. There is political risk in these stocks, as the situation currently unfolding with TikTok highlights.

With global COVID restrictions, all of these companies have seen significant share price appreciation since the March lows.

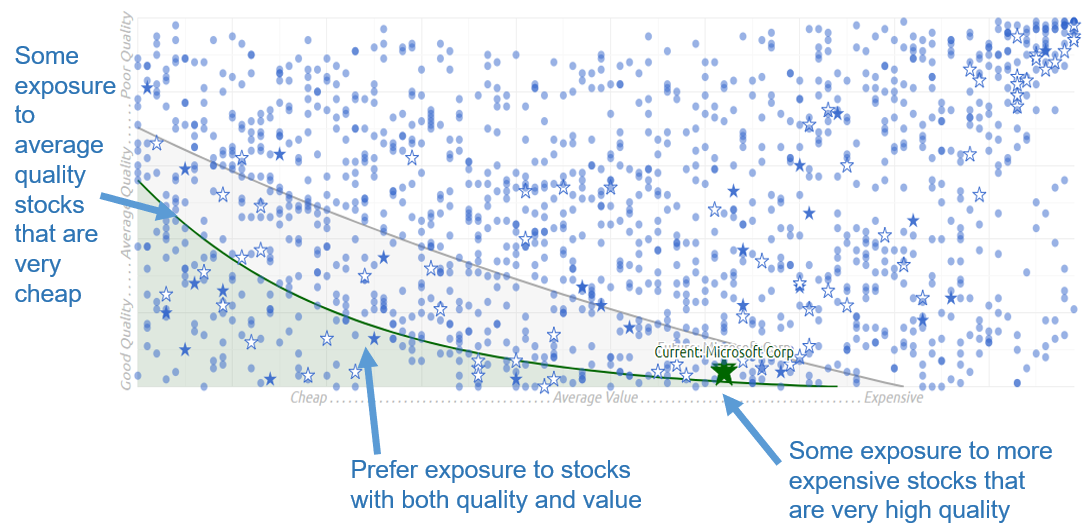

The pure-play stocks generally rate well on our quality or growth criteria but look expensive to us on our value criteria. So it becomes a question of how much do you pay for growth?

What does Nucleus own?

Our philosophy is to purchase quality companies at the right price. I.e. we will pay a little extra for high-quality companies, but average quality companies need to be cheap.

We do own the diversified names such as Sony, Google, Apple and Microsoft - although we have been lightening our exposure recently.

In Australia, we have exposure to Aristocrat, but internationally the pure-play gaming stocks look too expensive for my tastes. We want to buy them but can't justify the current prices. In a market pullback, these stocks are high on our shopping list.

Make no mistake, there is a generational shift underway. The average age of an eSports viewer is 23, the average soccer fan is 42. eSports viewers tend to be richer and better educated than non-viewers. It is an interesting market segment.

Damien Klassen is Head of Investments at Nucleus Wealth.

Follow @DamienKlassen on Twitter or Linked In

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Nucleus Advice Pty Ltd - AFSL 515796.