Winners and Losers from Franking Credit changes

Labour has proposed a number of changes to franking credits paid on dividends. The proposal absolutely has some merit behind it, as a system set up so that people weren't taxed twice has evolved into a system where some people get taxed zero times. But the current implementation has significant issues and creates a lot of enemies.

It has the commentariat confused because there are two separate issues dragging it in different directions:

- The change is bad for all retirees. Retirees lose the benefit of franking credits in a zero taxation superannuation environment. This policy therefore has the benefit of taxing rich retirees who have reduced their marginal tax rate from 49% to 0%.

- The change is bad for poor people. If you don't have other investment income to offset then you lose the benefit of franking credits - increasing the effective tax rate from 0% to 30%.

The intersection of these two groups, poor retirees will lose twice. That doesn't look like good policy or good politics.

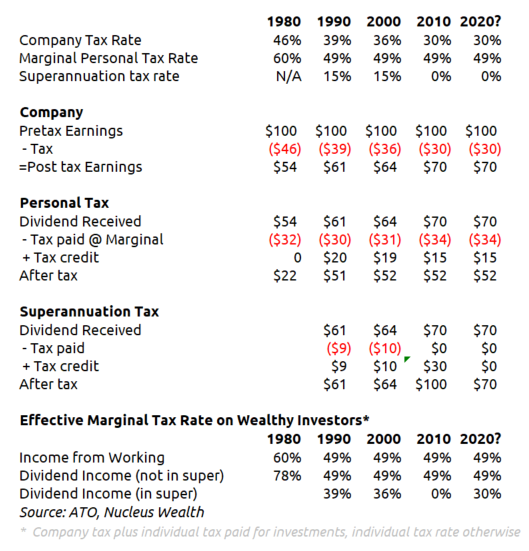

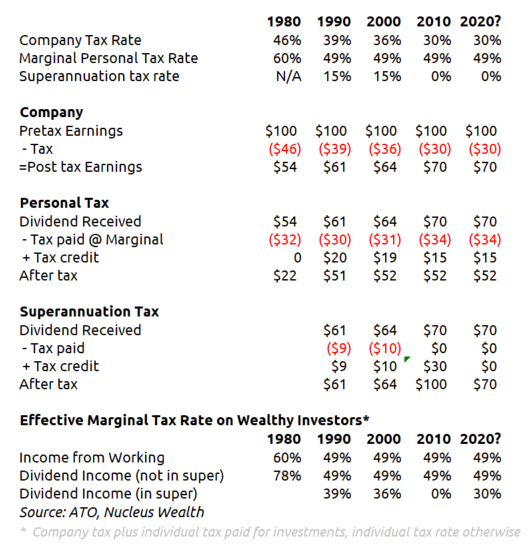

The table below shows the total tax rate (i.e. company tax plus personal tax) paid by various investors over time (a full calculations at the bottom of this post):

Full disclosure: I run an investment fund. We invest in a mix of assets including Australian shares which are negatively affected by the proposed changes. However, we also have a large amount invested in international shares where we will probably benefit. So, I'm not entirely sure which way I'm conflicted! When you are reading commentary, it is worth noting whether you are hearing from a winner or a loser from the change:

Losers

- Australian only fund managers. Franking credits will be less useful and so the benefit of owning Australian shares vs fixed interest or international shares just got worse.

- Self Managed Super Fund providers. Part of the benefit of having self managed super is access to franking credits. At the margin it makes self managed super less attractive.

- Accountants (over the long term). The accounting game works best when you can say "here is a big accounting fee that you won't even notice because of size of the tax return that you just got". The tax return will be smaller. Which means the fee is more noticeable.

- Australian Stockbrokers. The benefit of owning Australian shares directly gets worse (at the margin). One more reason to go to a fund manager rather than a broker.

- Retirees. They will pay more in tax.

- Poor people. They will pay more in tax.

Winners

- Tax Equality. The system was set up originally so that people weren't taxed twice. It has evolved into a system where some people get taxed zero times.

- Industry Super Funds. One of the key reasons that people leave industry super funds (especially retirees) is to access franking credit benefits. Labor generally has close ties to industry super funds, which is probably going to influence the politics.

- Accountants (over the short term). Tax changes? You are going to need to pay for advice.

- Corporate Debt in Australia. Australia's corporate debt market is tiny, and franking credits share some blame in encouraging investors to buy shares rather than corporate debt. At the margin, this change would encourage investors to add to corporate debt.

- Property Trusts and Utilities. Unfranked dividends from property trusts and utilities become more attractive.

- Residential investment property. Looking to get out of paying tax? Residential property is a favourite for Australian accountants.

Net Effect

Despite negative effects on my own business, getting wealthy retirees to pay a tax rate above zero is unambiguously good policy. It doesn't have to go back to the 78% that was paid in the 1980's, but zero is too low.

Getting poor investors to pay more tax is probably not good policy.

Adding carve-outs outs or maximum thresholds for poorer investors would make this policy a lot more attractive.

Footnotes - calculation for a retiree on the top tax rate:

Source: ATO, Nucleus Wealth

Source: ATO, Nucleus Wealth

Damien Klassen is Head of Investments at Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.