Save on Tax: Your "before 30 June" superannuation checklist

The first question:

Why do you want more money in your super?

You can save on income tax now. Your superannuation is taxed at 15%for contributions up to a limit. There are also various government incentives.

- Earnings on investment returns are tax-free in retirement. And prior to retirement, you can save on the tax paid on investment earnings. Investment earnings in superannuation are taxed at 0% in pension mode, and only 15% (10% for capital gains held longer than 12 months) otherwise.

If you are saving for a first home, you can use the tax rate in your superannuation account to save faster. You get a discount on income tax (if you earn more than $45,000). This can be worth thousands.

The May 2026 proposed tax changes only increase the attractiveness of superannuation relative to other investment vehicles.

What are the downsides?

You might not live long enough to enjoy it. Balancing your spending before retirement with your spending after retirement is important. When younger, it may be better to pay down debt rather than accumulate money for retirement.

There is an effective inheritance tax in super of up to 17% (mostly) on money that your employer adds. Some strategies that can reduce this.

Your money is (mostly) not accessible before you turn 60. Extreme hardship is likely an exception, but there are a range of other reasons you might want to access this money but can't. Between 60 and 65 it is relatively easy to access. After 65, the government will actively start making you take money out.

CHECKLIST: How do you get more money into Super?

-

You can instruct your employer to make additional payments from your pretax pay for the FY2026 year (and think about FY2027).

Benefit: You pay 15% rather than whatever your marginal rate of tax is. If you are (say) earning $200,000 on a 47% tax rate, then $1,000 pretax = $850 in super or $530 outside of super. That is a 60% return on day 1.

What to do: check your limits. You can contribute up to $30,000 year to 30 June 2026 plus potential catch-up contributions. Speak to your employer about salary sacrifice into superannuation. The tax will be done for you. -

You can make a payment yourself using after-tax money, and then claim a tax deduction. This is called a concessional contribution.

Benefit: When you do your tax return, you get back the tax that you paid. Your super fund will pay 15% of the amount you deposit in tax.

What to do:-

Check your caps. Simple version is $30,000 (including employer contributions) plus catch-up contributions from prior years. See below for more.

-

fill in a form with your superfund and deposit the money. Many superfunds have cut-off dates, so do this early June. For Nucleus investors, login to https://portal.nucleuswealth.com, choose your account, click on the deposit link for exact instructions.

- Your super fund will then send you an acknowledgement and now this will be classified as a Concessional Contribution. You can also do this as an SMSF.

- include this amount in your 2026 tax return

-

- You can make a payment yourself using after-tax money. This is literally just moving money from your own bank account into your super fund with no tax penalty.

Benefit: More money in your superannuation fund, where it will probably pay far less in tax.

What to do:- check your limits. You can contribute up to $120,000 in the year to 30 June 2026, with the option to bring forward up to three years. There are age and balance limits.

- fill in a form with your superfund and deposit the money. Many superfunds have cut-off dates, so do this early June. For Nucleus investors, login to https://portal.nucleuswealth.com, choose your account, click on the deposit link for exact instructions.

- If you are in a relationship and one partner is earning a very low salary, there are opportunities to get money into the low-earning partner's account.

Benefit: When the higher earner does their tax return, they get a tax offset.

What to do: The higher-earning partner can make contributions from their bank account of up to $3,000 into the partner's superannuation account and get up to a $540 tax offset. Check with your super-fund for instructions on how to deposit.- The receiving spouse must be under 75 years old.

- The receiving spouse's Total Super Balance must be under $2.0 million at 30 June 2025.

- When the higher earner lodges their personal tax return, declare the amount under the "Superannuation contributions on behalf of your spouse"

- Full $540 is available under an income of $37,000 then tapering up to $40,000.

- If you earn less than $62,488, then you can make a voluntary, after-tax contribution into your own super account. The government will add up to $0.50 for each dollar if you earn less than $47,488 and a partial amount between $47,488 and $62,488. The maximum you can deposit is $1,000 to get $500.

Benefit: More money in your super fund.

What to do: This is the same as (3) above. Note that at least 10% of this money must come from employment (rather than investments or benefits), you must be under 71, your total super balance needs to be under $2.0m at 30 June 2025. The Australian Tax Office will automatically calculate this for you and deposit the amount into your super fund.

Catch-up Contributions

The pre-tax contribution limit for this financial year is $30,000. However, if you have not used up your whole cap for this year or the last five years you can contribute any unused cap amounts providing your total super balance at 30 June 2025 was below $500,000. These unused concessional contribution caps are on a rolling 5-year basis and any unused cap amounts will expire after this rolling 5 year period.

To check how much available unused concessional contributions you have available you can check this via the ATO through MyGov (see below for how).

You can do this as a lump sum personal deductible contribution and reduce your taxable income and claim a tax deduction.

This can give you more flexibility around making concessional contributions into super, especially if you have some spare money or come into a lump sum, have broken work patterns or cannot contribute in some years.

After-Tax (Non-Concessional) Contributions

The non-concessional cap is currently $120,000 p.a. and these are contributions made from your after-tax income. These contributions are not taxed (not subject to the Super contributions tax of 15%) when making the contribution, as you have already paid tax on that money.

Additionally, if your total super balance is less than $1.76m, you can use the bring-forward provision and do a one-off after-tax contribution of $360,000 ($390,000 after 30 June) and use up 3 years' worth of non-concessional contributions in one lump sum. There is a rolling 3-year period under the bring-forward provisions, and you will be unable to make any more after-tax contributions for the next 2 tax years until your after-tax contribution cap resets.

There are some age restrictions also, so please see the latest information from the ATO and always seek advice from a licensed financial adviser or tax specialist.

Final thoughts

Superannuation is the best opportunity most wage earners have to lower their tax rate substantially.

When you move into pension phase, say you have $X outside of superannuation. Any interest or dividends will be taxable, but the same amount in your superannuation has a 0% tax rate (provided you are under $2m).

The closer you are to 60, the more you should be looking to get your money into Super. The more you have, the sooner you need to start. Once you turn 60, there are ways to get the money out if you need it. After 65 there are no restrictions. Once you move your account into tax-free pension phase, the government will be forcing you to take money out.

Also, if you have a spouse and only one of you is close to the $2m limit (or likely will be when retiring), then you should consider making contributions to equalise your balances.

Will we see more tax changes to superannuation? Probably. But superannuation is designed to be attractive from a tax perspective to encourage people to save. It is unlikely to be a less attractive vehicle than a typical investment outside of super.

Just a reminder that this is general advice and doesn't take into account your personal situation. Please be aware that Superannuation is an ever-changing landscape so always seek specific tax advice for your situation or speak to your financial adviser.

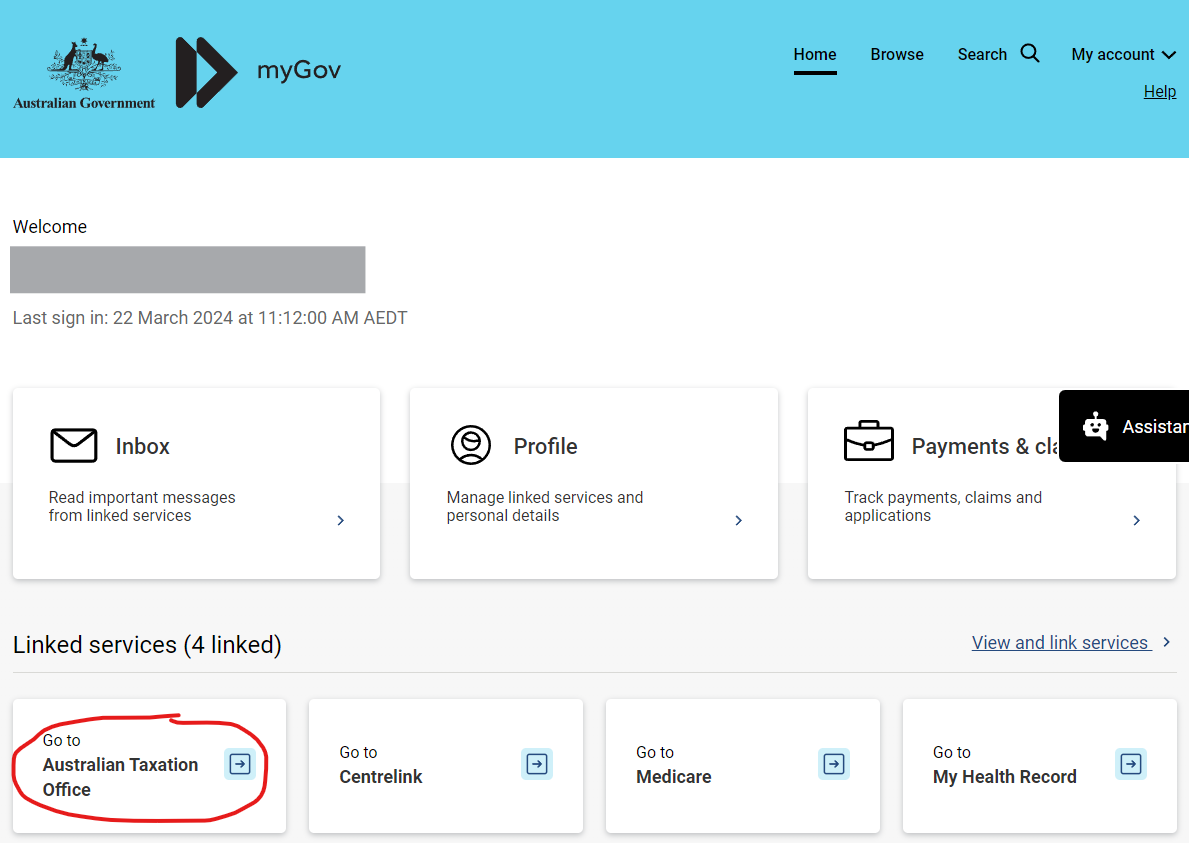

Appendix: Where to find your concessional contributions on MyGov

- Go to my.gov.au and login.

- Go to the Australian tax office

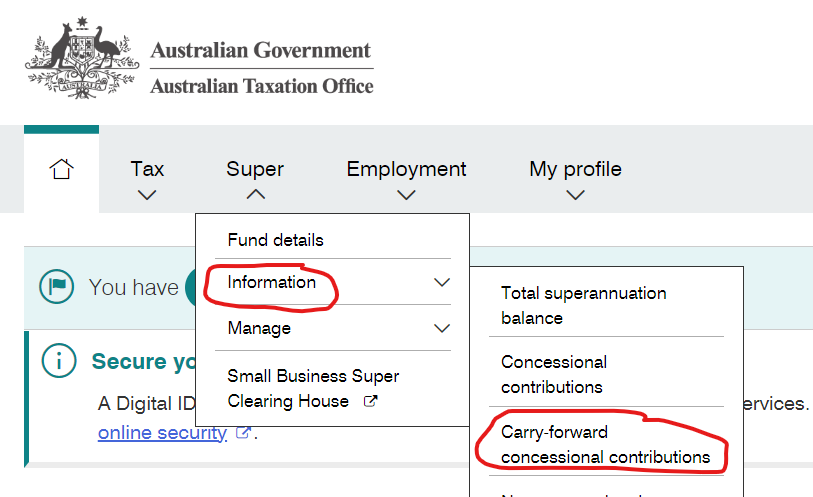

3. Select Super -> Information -> Carry forward concessional contributions

4. Select the year and see your contribution:

Note that the information may not be fully up to date and relies on your superannuation funds reporting.

It does show the calculation, but you should also maintain your own records, particularly if you have a self-managed fund or multiple superannuation accounts.