Ignore solar pricing at your investing peril

Australian energy policy is a mess. Investors should ignore the arguments. The antagonists are stuck in a perpetual time shift, prosecuting cases from 5-10 years ago, ignorant of the incoming change in solar economics.

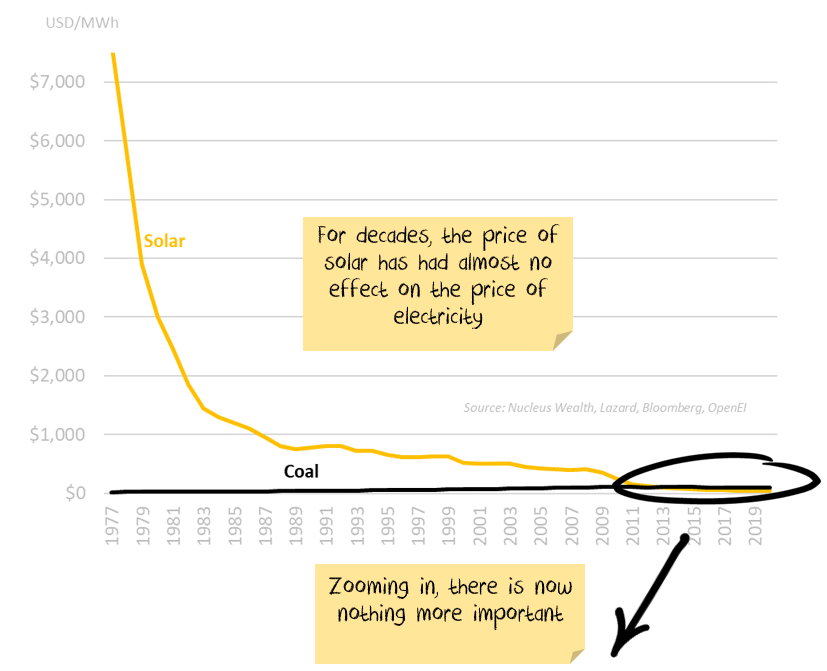

5 years ago coal and gas were the cheapest sources of energy in a majority of countries. Now wind and solar are.

"But but but, gas and solar are intermittent. YOU NEED BASELOAD!!!" cry the fossil fuel defenders.

Sure. Today battery + solar is more expensive than baseload coal. The problem is you don't have to look too far forward to see that it won't be soon. Coal, gas, oil, all have economics based on a scarcity curve: the more we use, the deeper we need to dig and more expensive to extract. Solar and battery power is on a technology curve, the more the world produces, the cheaper it becomes:

This leaves us with an energy parity where the technology curve becomes an upper bound for the scarcity curve. i.e. the price of energy won't meaningfully exceed the cost of Solar+Batteries.

Solar+Batteries are the "killer app" – extremely scalable once they reach an acceptable cost. All the current trends point to energy parity being sooner rather than later for electricity.

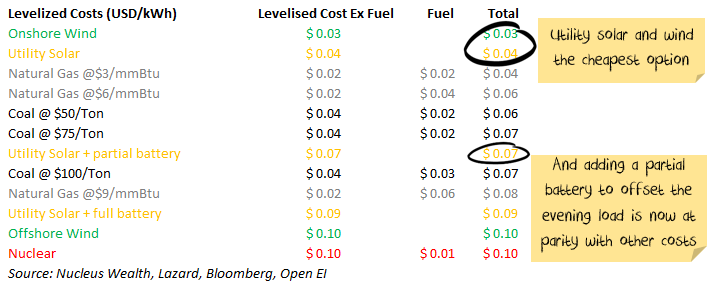

Relative cost of energy

There are a few big-picture numbers that you should be aware of. All figures are USD/kWh for international comparability. We use levelized cost of energy, which adjusts for the up-front cost of building power plants or solar arrays, asset life and tax issues. These numbers are only approximate, rely on a lot of assumptions and vary by country and region. In general, the numbers are for new installations with recent technology.

Gas is no longer a transition fuel

Solar Cost Trends

However you measure it, the cost of solar has fallen dramatically relative to other energy sources. Opponents will rightly point out that solar only supplies power during the day and wind power is intermittent. What is needed is something to store the energy, and fortunately, batteries are on the same type of price curve:

Battery prices will continue to fall because:

- governments (in some countries) are lending considerable support to fight climate change

- phone makers are spending significant research and development money on the battery problem

- electric vehicle makers are spending substantial research and development money on the battery problem

- there are a range of new, more efficient solar technologies that have been proven in the lab but haven't progressed to the real world yet

- simple scale manufacturing benefits will help as more batteries are produced

In Australia, often the argument gets confused because we typically buy systems from offshore, and so the dramatic fall in US dollar prices has been partly hidden by the falling Australian dollar.

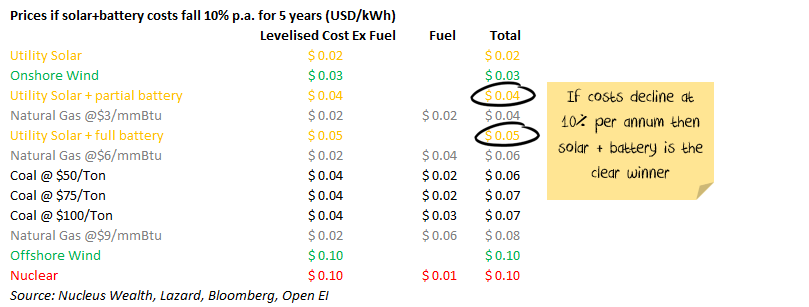

Future Prices

There is a range of different outcomes we could see for electricity prices.

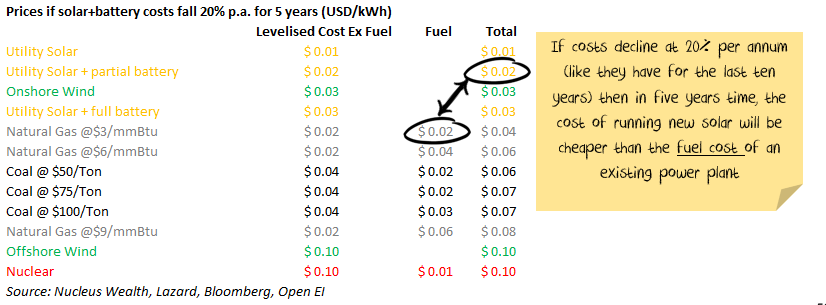

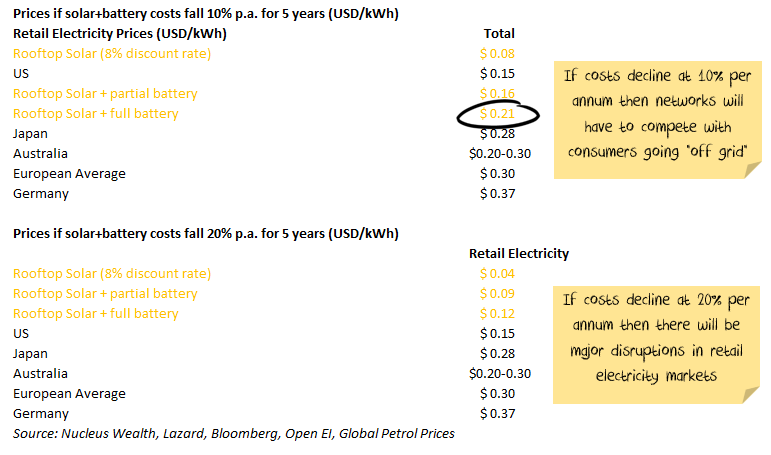

Below I have focused on two different scenarios, one where solar+battery costs fall at 10% per year for the next five years, another at 20%.

In the last ten years, costs have fallen around 20% per year. Given how low solar costs are, the critical assumption is battery prices. A 20% fall in battery prices will have a much larger impact than a 20% fall in the cost of solar.

Either way, there is very little scope for coal prices to rise. Suppose the 10% per annum cost savings are achieved. In that case, there will be no new fossil fuel power plants in even moderately sunny climates.

Existing coal-fired plants with lots of remaining life will start shutting down if 20% per annum cost savings are achieved.

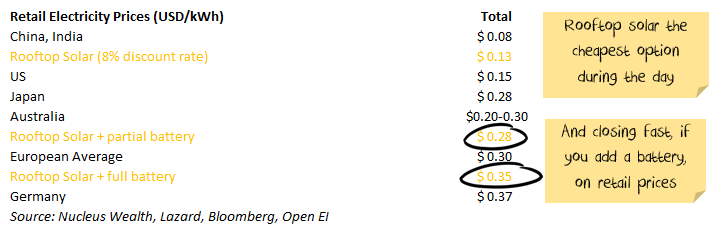

Rooftop Solar

I have deliberately left Rooftop Solar out of the above tables, as rooftop solar is less comparable than you would think. Roof-top solar has costs of around $0.13 if you assess it on the same basis as above.

But that is not important. Rooftop solar is not competing with a coal plant, or even with utility solar.

Rooftop solar is competing with grid power + grid infrastructure. It is an important distinction.

I don’t care whether my rooftop solar produces cheaper than the local coal-fired power station. I care whether it produces at a cheaper rate than I pay for power – and it does:

The issue is my panels provide power during the day when everyone else's panels are also producing electricity. So, unless I use it myself to offset the above charge, I get paid a fraction of what the power company will charge my neighbour for using my spare electricity. Also, the peak rate (in the evening) for time-of-day pricing is much higher than during the day.

At $0.28 for partial shifting, (i.e. generating enough power to get you through the evening peak), having some batteries is profitable in the right climate, but the return is low.

The big assumption is the discount rate. At current prices, partial shifting is worth it if you are prepared to accept a lower return.

But batteries aren't yet a "no brainer" cheaper option.

Looking at the 10% cost reduction and 20% cost reduction scenarios again:

There are lots of questions that the above table raises. If everyone starts going off-grid, who pays for the poles and wires? Do we end up in a "death spiral" where more people leave the grid, raising the cost for those who remain, which means more people leave and so on?

All valid questions.

My best bet is that it is going to be a battle of vested interests. Wealthier people will leave the grid when it becomes economic as they can afford the upfront cost. This leaves renters and the poor left paying higher bills to account for the transmission assets. Governments will have three options:

- Prevent retail electricity price rises, support the rights of the many over the few and make the asset owners pay the cost of their mistaken investment

- Socialise the losses and bail out the transmission asset owners

- Let the asset owners raise prices, shift the cost of adjustment onto the poor

While option 1 would be my preferred choice, the cynic notes option 3 will be the path of least resistance. The lobbyists will no doubt be hard at work on option 2 in case any government have the fortitude to explore option 1.

The Rooftop Solar pub test

In all of the tables above, we have used an 8% discount rate in order to benchmark returns. This is appropriate for companies looking for an economic return. However, for individuals, maybe the discount rate is much lower. For many people, the calculation involves increase their mortgage short term to pay for the panels with the hope of a lower mortgage in the long term based on energy cost savings.

If we used the mortgage rate instead of 8%, then you can slice 30%+ off the cost of rooftop solar in the table above.

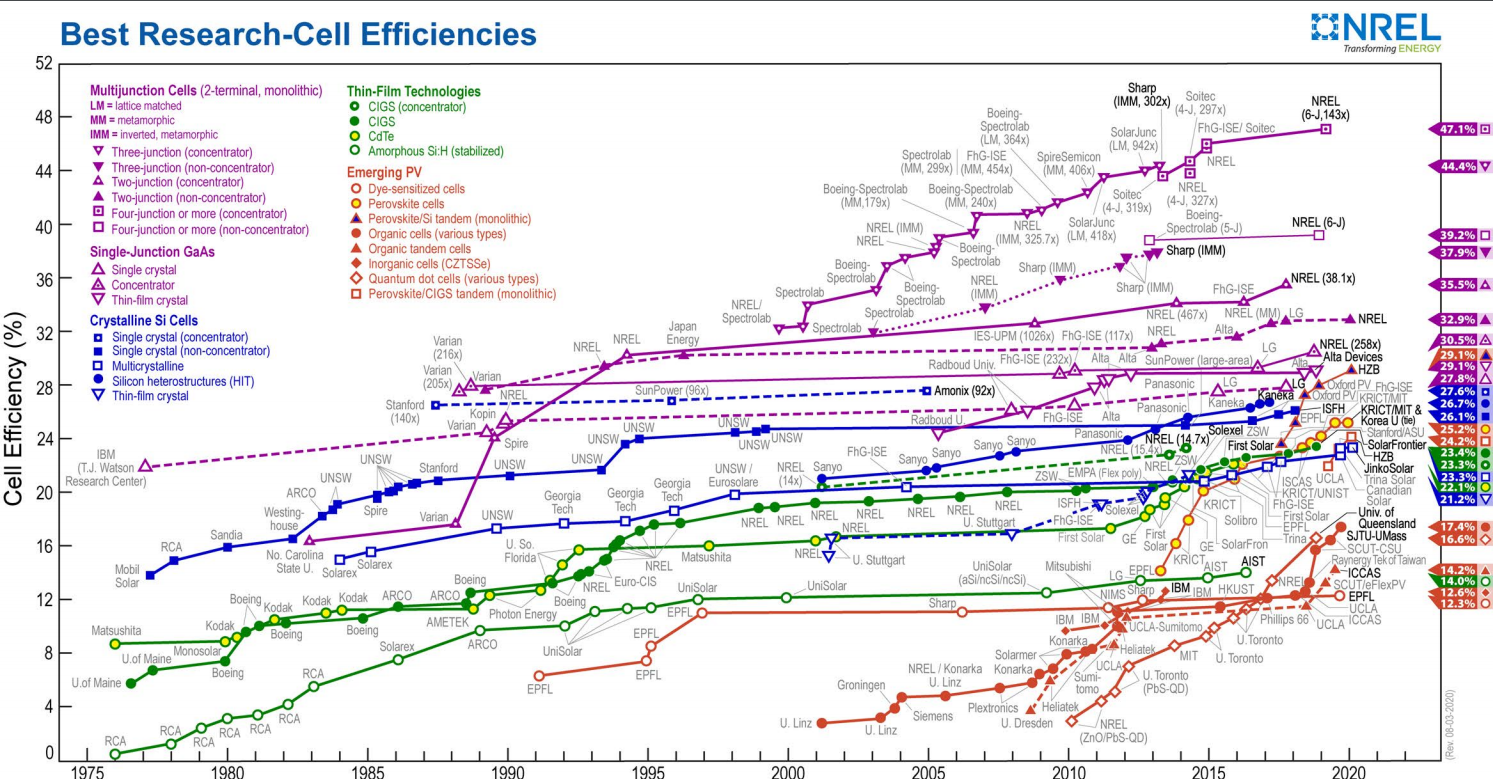

Picking solar winners will be difficult

It is hard to pick solar winners – there are so many competing technologies that are improving, all with different economics:

Keep in mind this chart is a comparison of conversion efficiency – not of economics. A 20% efficient (low cost) thin-film technology that can be painted onto structures might be much cheaper per kW than a 48% multijunction cell.

The net effect is you can try to invest in a manufacturer, but for all you know the technology will be superseded.

Maybe there will be an alternative renewable technology breakthrough which drives electricity prices lower more quickly. I'm not saying it isn't possible. However, for investors, the main game is solar – colossal potential and a history of steep cost reductions. I expect other renewable technologies will contribute to lower prices at the margin, but solar is the main issue for electricity costs.

Solar Resources

It matters whether you are in a sunny location or not.

Cities like L.A., Sydney, New Dehli will find solar costs 20% cheaper than somewhere like New York, Beijing, Tokyo as they simply get more sun. At the other end of the spectrum, London or Moscow get about half the solar resources of L.A. or Sydney:

Source: Solargis

You will also note from the above chart that solar resources are pretty good in most emerging countries. This is where most of the growth in demand is coming from.

Investment Outlook

At the moment, it looks like less than 5 years until we see significant changes in the electricity market, even if the cost reduction rate doesn't halve. And don’t ignore rooftop solar + batteries. Currently it is a lot more expensive than coal, but retail power prices are a lot more expensive than wholesale. What's more there is a decent chance these converts going off-grid start a “death spiral” for electricity transmission.

Battery costs are the primary determinant at this point – if the rate of improvement slows significantly, then it may take 10 years. My base case is that battery improvement will be sustained, but its far from a given – this is the assumption to watch.

I'm expecting power prices during the day to continue to fall over the next few years as we end up with a surplus of power from renewables. This will actually drive the pick up in batteries – the more significant the difference between the day price and the evening price, the bigger the incentive for batteries to arbitrage the difference.

The US is not the market to watch – energy costs are lower there than almost any other developed market. A better indicator of the future will be developments in Europe.

Key sectors:

- Coal/Gas: I'm in no way saying that coal and gas will cease to be used when we hit parity. However, the price will be limited to no more than solar+batteries, and that cost will fall year after year. Any investment in these companies should be made with falling commodity price expectations – i.e. value them in run-off. There may be short-term shortages/price spikes, but these are selling opportunities. Increases in electric car penetration may limit the downward trend for a few years.

- Solar companies: Solar manufacturers are difficult – the technology is moving too fast to work out if there will be a "winner takes all". Service providers to the solar industry are probably a better investment (if you can find one that's not already very expensive). We have made a few profitable investments in semi-conductor stocks that manufacture "commodity-type" parts for solar companies. It is not a sexy area of the market (and thin margins), but at the right price, some of these stocks are interesting.

- Industrials: Companies that have high electricity bills during the daytime (or can shift costs to the daytime) will benefit. There are many European materials and refining companies that have struggled to compete with US companies because of the lower-cost US energy in recent years that will benefit.

- Oil: At the margin, less diesel will be used for power generation in remote areas. Expect this to continue. It is not a large part of the oil market, but it will mean oil demand will be weaker than they would have otherwise been.

- Electricity Transmission: Will these companies get bailed out? Will increased prices to offset falling customers be allowed? Or will companies take the pain of the "death spiral"? It is a country by country decisions – lots of risk in this trade.

- Electricity Production: The toughest thing about an investment today for these companies is that the company who builds a solar array next year will have lower costs than the one who built last year. Plus the regulatory risks from the "death spiral". Another risky trade.

None of this relies on carbon taxes. Carbon taxes will only accelerate these changes.

.jpg)