The Hidden Costs of High Dividend Yields in Australia

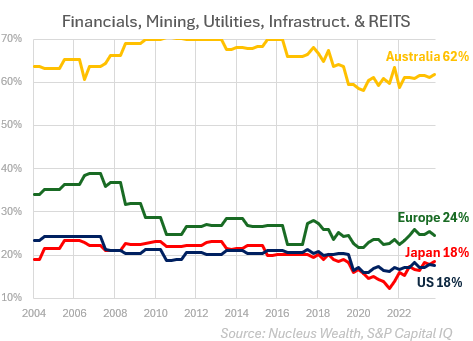

The Australian stock market is a case study of how regional nuances can shape investment outcomes. Say you were a financial advisor in the US, Japan or Europe. If you put a retail client into 50% miners and banks, and they tanked, you might lose your licence. In Australia, that is just the market:

\

\

Yet this investment composition defines the risks for Australian investors. And explains most of the reputation for high dividend yields.

Houses and Holes

The "houses and holes" economy describes how Australia digs holes to sell dirt internationally and uses the income to bid up house prices among the population.

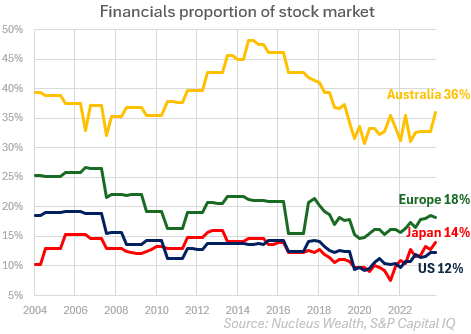

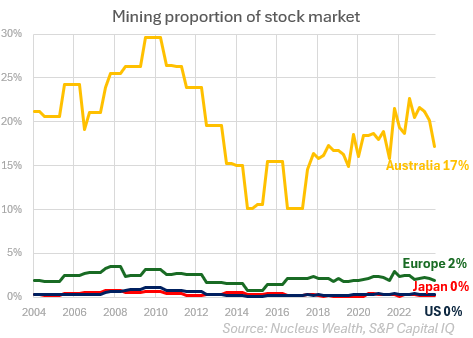

The key beneficiaries? Major banks: Commonwealth Bank, ANZ, National Australia Bank and Westpac. Plus mining giants like BHP and Rio Tinto. And so the stock market reflects this.

This contrasts sharply with the rest of the globe. Banks typically make up less than 10% of most markets. Mining is typically a rounding error, less than 1%.

Mining: volatile, low-value add

Being an efficient miner with high safety standards is a valuable role Australia plays in the global economy.

However, mining is a low-value-add sector. Its profits come from high commodity prices, a factor Australia has almost no control over.

And profitability can swing wildly from year to year. The last 20 years for the mining sector have been about the rise of China. That theme is looking increasingly cooked.

What is banking for again?

Banks are highly leveraged companies. Which makes them riskier than the typical company.

But, more importantly, the job of a bank in an economy is to provide capital to other parts of the economy. In many ways, the banking sector's profits are a cost for the rest of the economy. i.e. the more banking profits grow, the less profit other, more innovative, sectors of the economy make.

So, how much should a massive banking sector be celebrated?

Utilities, Infrastructure, and REITs: Low-growth sectors

Australia also has about twice the exposure to utilities, infrastructure, and REITs relative to Japan, Europe or the US.

These sectors play an important role. But they aren't high-growth sectors. They are toll collectors. They represent a cost to other companies.

Triple the exposure

In aggregate, these sectors make up 3x more of the Australian market than the rest of the developed world:

Which just leaves less room for those companies trying to innovate.

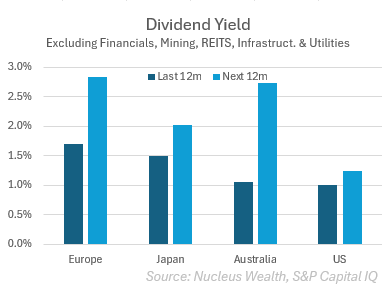

About those yields...

The Australian stock market pays a higher dividend yield than the rest of the world. This is often credited to franking credits, which do have some effect.

However, sector allocation has a bigger impact. Banks, mining companies, utilities, infrastructure entities, and REITs are known for their relatively higher dividend payouts. This means that most of Australia's higher yield is simply due to sector allocation.

Take Europe, for example. Its dividend yield is 10% lower than that of the Australian market. But if you simply reweighted your European stocks to reflect the sectors in Australia (i.e., bought more banks, miners and utilities), then your dividend yield would be 15% higher than that of Australia.

When we look at the "rest of the market" then Australian yields do not look exceptional:

Implications for Investors: Risk

Diversification is important to reducing risk. But not just for its own sake. Another part of reducing risk is liability matching. I want my assets to help me pay for my future liabilities.

Suppose I am expecting to need to buy cars, phones, watch movies and take international holidays in the future. In that case, it makes sense to invest in those sectors. Which tend to be international rather than Australian.

Or maybe I am worried about the effects of Artificial Intelligence or weight-loss drugs on my earning potential. Investing in those companies makes more sense than a large exposure to the mining sector.

I'm also expecting to pay Australian tax in the future. If mining companies boom, then Australian tax receipts will also increase, and so I'll probably have a lower tax bill. My risk is that the opposite occurs, in which case, more mining shares are not going to help.

The hidden cost of dividends

The Australian market pays one of the highest dividend yields in the developed world. And franking credits add to the benefit (although international shares have their own tax benefits).

But this is not costless. It results in a higher-risk portfolio. A portfolio with a large exposure to toll-collectors and basic materials. It comes with the risk of a portfolio that does little to match an investor's future spending patterns.

I'm not saying your Australian weighting should be 0% of your stock market exposure. But it should be much less than 100%. In most of our tactical portfolios, it is less than a third of our international exposure.

International Options

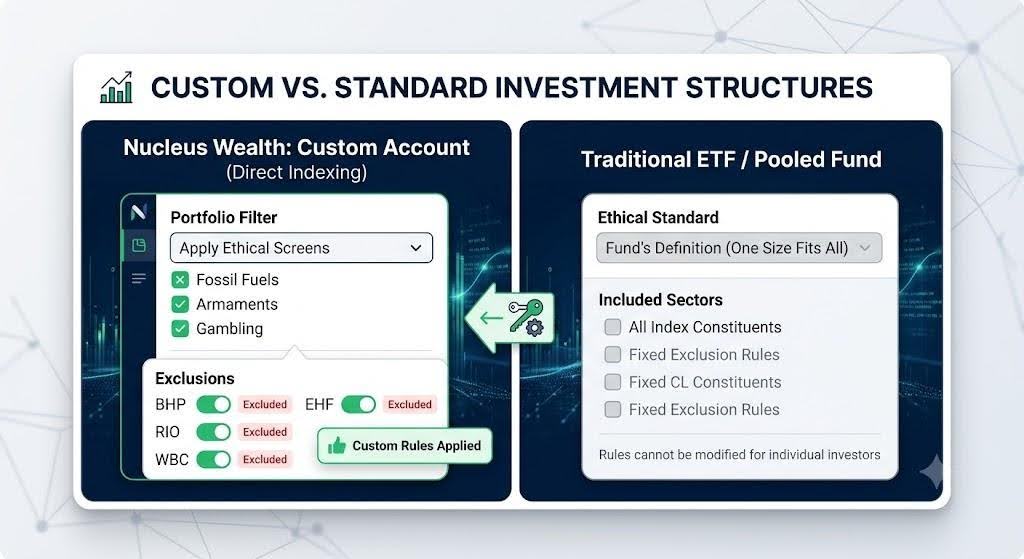

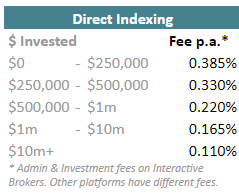

Our direct indexing portfolios let you take an index portfolio and tailor it to your investment desires. Say by adding more Artificial Intelligence or Cloud Computing and maybe adding or subtracting Nuclear Power. There are over 100 different screens and tilts, and the fees are low:

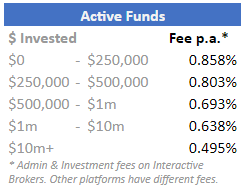

In our core international portfolio, we do the thematic selection for you. Right now, we are exposed to a host of major trends: artificial intelligence, weight loss drugs, cloud computing, and energy, to name a few:

Minimum investment amounts vary by platform. On Interactive Brokers the minimum is $2,000.

Take us on your daily commute! Nucleus Rapid Insights is available in Podcast form on iTunes and all major Android Podcast Platforms.