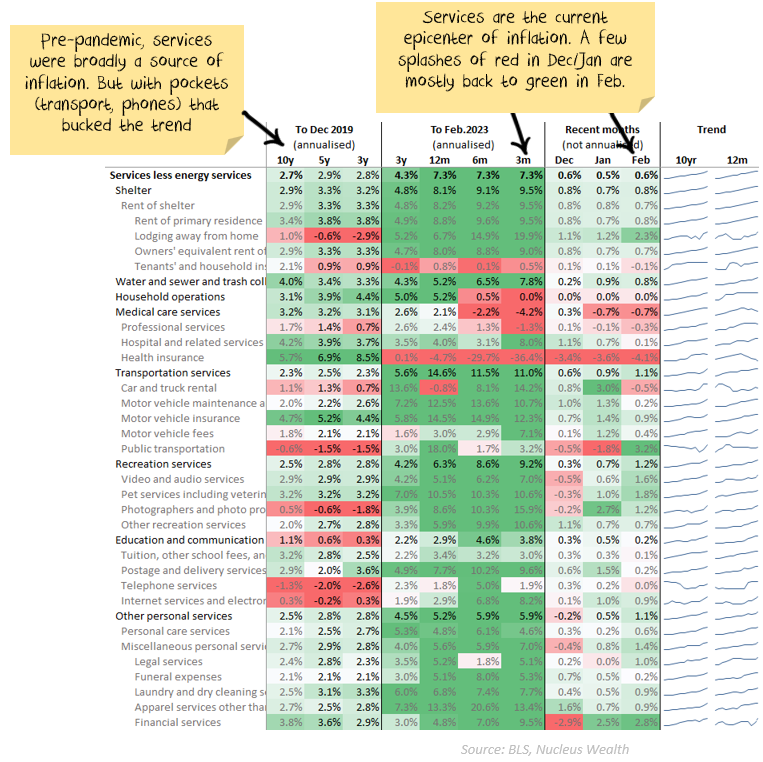

US inflation: still concerning

US inflation came in around expectations. More than a few data points in this report are reversing the recent trend of falling inflation. Based on surveys and upstream data points, I believe inflation is heading for deflation. But, this report did little to support the argument. See tables:

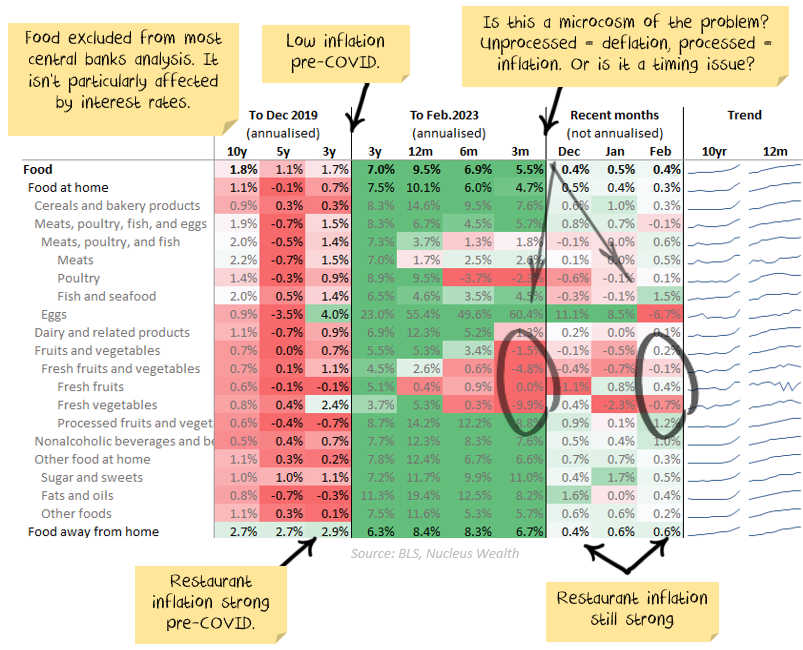

A microcosm of the problem

Fruit and vegetables are an example of a broader issue. Inflation ran hot in this category during 2022 but turned clearly deflationary in recent months. However, processed food and vegetables are still seeing rampant inflation, up 14.2% over the year, running at almost 9%p.a. over the last three months:

A few possible explanations:

- Timing. The deflationary impulse from lower input costs has not had time yet to flow through to processed food. If this is true, then we just need to wait for deflation.

- Opportunity. After years of deflation, processed food makers are using the cover of broad inflation to get through price increases. If this is true, companies will try to hold onto these price rises unless competition becomes so fierce, or demand drops due to a recession, and they are forced to cut. This is an argument for prices holding high for an extended period, then the trapdoor opening and prices plummeting.

- Costs. The cost of equipment and servicing has increased due to shortages. Labour costs are also higher. And so prices need to be higher to cover this. This is an argument for the rate of price increases to slow but not turn into deflation.

- Expectations. Higher price expectations are embedded into suppliers, workers and customers, and companies are merely responding. This is an argument for continued price rises.

Now each one of these arguments has some truth to it. Different sectors will have different characteristics, which will make one or other of the arguments stronger.

In the food category, with pretty low barriers to entry, I would expect timing and opportunity to play the largest part. In sectors with less competition, price falls become less likely.

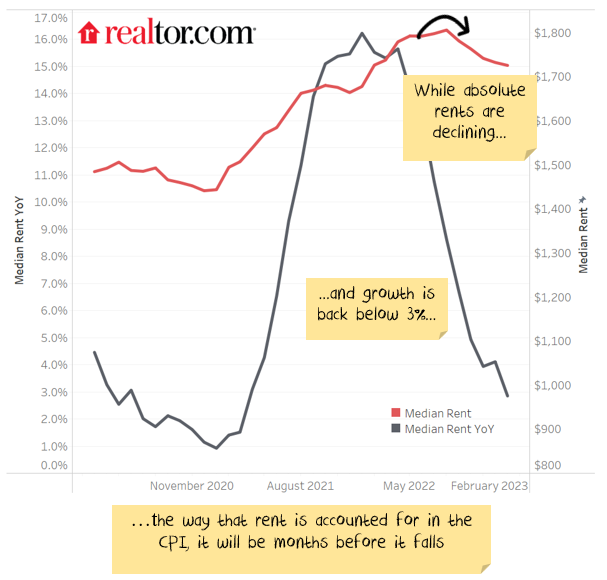

Calculation/reporting issues

Rental inflation, the largest part of services inflation, is still running hot in the report. This is at odds with what participants are reporting:

It is a factor of how rents are calculated in the inflation numbers, reflecting that rental contracts don't all expire each month and so increase gradually.

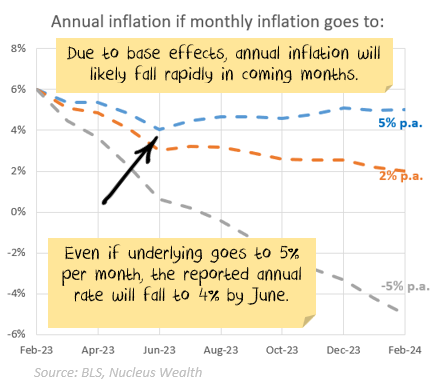

Going forward

The way the maths are at the moment, annual inflation is going to start falling rapidly over the coming months:

My expectation is that:

- central banks want to ensure inflation is truly dead before reversing course

- headline annual inflation figure will stay high until April, but will fall rapidly after that due to base effects. It will be important to look through this to the underlying numbers.

- interest rates will stay high until it is too late and inflation turns into very low inflation or deflation. Or until the US central bank breaks something it can't fix.

This report doesn't preclude a continued fall in inflation, but it doesn't support it either.

.jpg)