The Counterintuitive maths of CGT changes

The Australian Federal Budget has ignited a fierce debate around tax reform, with the spotlight firmly fixed on changes to negative gearing and the capital gains tax.

For property, the changes are expected to put downward pressure on prices. But for broader investment portfolios, the proposed CGT changes are opening a complex can of worms.

What are you optimising for?

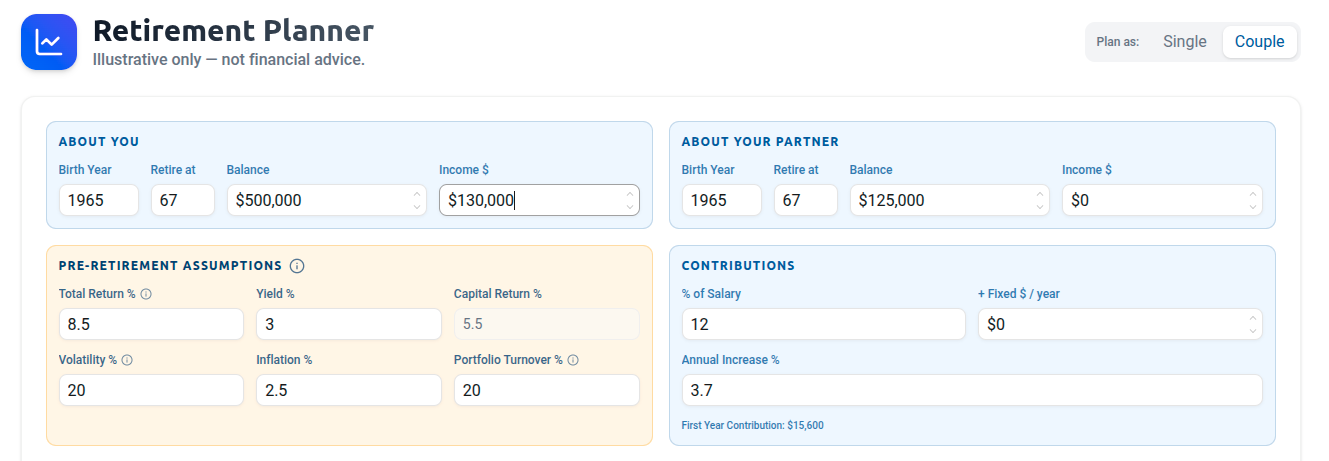

We have a new calculator to show the issues. You can enter your age, your savings, your retirement age and then see which structures are best for you.

The big issue though is tax. You should not be optimising for the lowest tax. I can easily do that for you: put all your money in transaction accounts at Australian banks. You will get a 0% return - tax problem solved.

Instead, start optimising for the highest after-tax return. Do not choose worse investments just to avoid paying tax.

Pick the appropriate asset allocation first, then work out the most effective structure.

Look beyond the political noise

When you run the numbers, a counter-intuitive reality emerges: in a high-inflation environment, the government’s proposed changes might actually raise *less* revenue than the old system.

Here is a breakdown of the mathematics of the new CGT rules, how your portfolio size dictates your tax exposure, and the strategies you can use to protect your returns.

1. The Inflation Indexing Math: Be Careful What You Wish For

Under the legacy Australian tax system, investors received a flat 50% discount on capital gains for assets held longer than 12 months.

If you bought a stock for $100 and sold it for $200, your nominal capital gain was $100, and you were taxed on $50, regardless of how much inflation occurred while you held the asset.

The proposed changes shift the goalposts by taxing real capital gains (indexing the purchase price for inflation) instead of offering a flat discount.

On paper, this sounds like a tax hike. But when you factor in inflation, the mathematics can tell a different story.

The Nominal vs. Real Calculation

Let’s look at a scenario where you achieve an 8% annual return on an equity portfolio over a long holding period. Assume 3% of that return comes from dividends (taxed annually as income) and 5% comes from capital growth.

Under the Legacy System (50% Discount): You are taxed on half of the 5% capital growth. Effectively, you pay tax on 2.5% per annum of growth when you realise the gain.

Under the Proposed System (Real Gains Taxed): Let’s assume inflation runs at 3% per year. To calculate your taxable gain, you subtract inflation (3%) from your capital growth (5%). You are taxed on the remaining 2% per annum real capital gain.

Because inflation eats up 3% of your return, your taxable capital gain under the proposed system is actually lower (2%) than it would have been under the legacy 50% discount system (2.5%).

If we enter a sustained period of higher inflation and lower real returns, the Australian government may find that these tax changes raise far less revenue than keeping the old 50% discount. For long-term, lower-risk investors holding quality equities, inflation-indexing can actually work in your favour compared to a flat discount.

The Start-up penalty

The maths flips the other way on higher-risk investments. i.e. a retiree with a diversified portfolio (particularly conservative portfolios) ends up paying far less tax.

Who bears the brunt? The most successful company owners. If you are investing in high-growth companies that double or triple, then you pay far more tax.

It doesn't sound like great tax policy to me to give retiree's even more tax benefits while punishing entrepreneurs. But that is where we are at the moment.

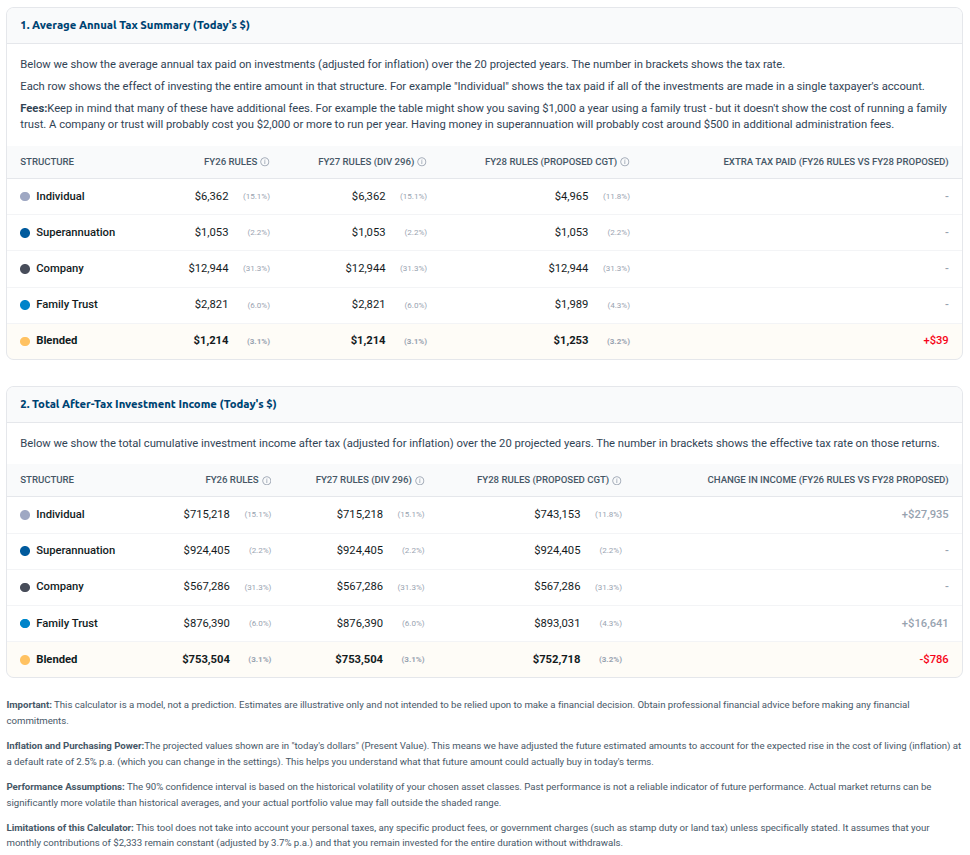

2. Portfolio Size: Who Actually Pays More?

To understand how these changes affect you, we ran multiple scenarios using the Nucleus Wealth tax engine. The results show that the impact of the new CGT and superannuation rules depends entirely on the size of your portfolio.

The Under $1 Million Portfolio

If you have a portfolio under $1 million, the CGT changes will have a negligible impact on your long-term wealth. The combination of personal tax-free thresholds and existing super concessions means your net after-tax returns remain largely unchanged.

Your tax rates (assuming you judiciously use super and individual tax-free limits) are likely <4% on total investment earnings.

The $2 Million to $5 Million Portfolio

For a couple with $2 million looking to retire, the tax changes require more careful planning, but they are far from disastrous.

If you hold all your assets in a single name or a single super fund, your average investment tax rate will rise.

However, by adopting a blended portfolio structure — for example, putting 35% in each partner's Super, 10% in a family trust, and 10% in each individual's personal name—you can keep your overall investment tax rate between 2.5% and 4.5%.

This structure allows you to split income, utilize personal tax-free thresholds, and keep your Super balances below penalty thresholds.

The $10 Million+ Portfolio

For high-net-worth investors, the biggest hit does not come from CGT directly, but from the new Division 296 rules, which tax earnings on superannuation balances above $3 million at an extra 15%.

Under the old rules, a $10 million portfolio in Super would face a 15% tax rate. Under the new rules, that tax rate rises to 26% or more.

For these balances, holding all assets in Super is no longer the default choice. A blended structure involving family trusts and companies becomes essential, reducing total tax liability by 30% to 40% compared to a single super fund.

3. Direct Indexing: The Ultimate CGT Shield

No matter your portfolio size, the investment vehicle you choose has a massive impact on your tax bill.

Instead of buying units in a fund, with Direct Indexing you own the underlying shares directly in your own name. This gives you absolute control over your tax outcomes.

Low turnover

Direct Indexes have very low turnover. Our global index is up about 250% in the last 6 years and has turned over less than 5% of holdings. If you don't sell, you don't have capital gains.

Tax benefits on rebalancing

When a new company enters the index and you need to adjust your holdings, Direct Indexing allows you to selectively sell specific parcels of shares:

1. Capital Losses: Typically, the stock that is being removed from the portfolio has gone down in value - i.e. you are realising a capital loss, which you can use to offset capital gains elsewhere in your portfolio.

2. Specific Parcels: If you must sell a stock that has grown (like Nvidia), you can choose to sell the parcels you purchased most recently (which have a higher cost base and a smaller capital gain) rather than the parcels you bought years ago.

Our tax modelling shows that shifting from a high-turnover portfolio (20% annual turnover) to a low-turnover direct indexing portfolio (3% annual turnover) can cut your total capital gains tax liability by thousands of dollars.

4. Don't Let the Tax Tail Wag the Dog

When tax rules change, the natural reaction is to call your accountant and set up complex legal structures to minimise your bill.

This is often a mistake.

You could (say) spend $5,000 to set up a complex web of family trusts and corporate beneficiaries to save $3,000 in tax, only to pay $2,500 in ongoing accounting and auditing fees. You have added administrative stress for a net benefit of $500 per year. And if the government change the tax rules in the next 10 years you could be behind.

Your goal should never be to minimise tax to zero. Your goal is to maximise your after-tax return.

Always look at the pre-tax investment case first. Make sure you are buying high-quality, productive assets that generate real returns. Once you have established a strong investment case, select the simplest, most cost-effective structure to hold those assets.

Use tools like ours to help your planning and give you big picture support. But calculating your tax rate to 4 decimal places with uncertain future tax policy is unlikely to be worth the effort:

.jpg)