There is a battle going on in the financial press for the hearts and wallets of retail investors.

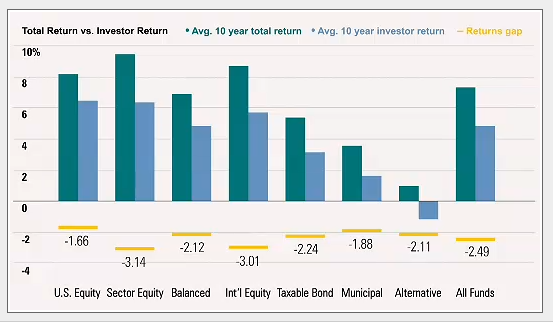

On one side is research houses Morningstar and DALBAR who both regularly publish studies showing that retail investors underperform – DALBAR’s most recent report thinks retail investors do 3.5% worse per year than the market, Morningstar think 2%:

Morningstar Returns Gap

For both of these, the main factor is investor behavior. When markets wobble, investors tend to sell or sit on their cash. When markets have been performing well, investors tend to invest their cash. i.e. they buy high, sell low.

On the other side is S&P SPIVA who come out with headlines about the number of active investors that underperform their indices:

Over the 10-year period ending June 30, 2017, more than 85% of international equity and Australian bond funds and more than 70% of Australian general equity and A-REIT funds underperformed their respective benchmarks on an absolute basis.

Something doesn’t add up

Obviously, there is something not connecting with the above. If retail investors are underperforming and professional investors are also underperforming, who is actually winning?

Disclaimer: I am an active investor and so clearly biased.

My broad brush is that:

- Professional managers as a group (there are big differences in individual funds) tend to outperform. Then, (as a group) they extract most of the outperformance back in fees.

- Index funds slightly underperform (due to fees)

- Individual investors underperform (although there are big differences in individual investors).

- The guys taking the fees win every time…

So, Active or Passive?

I personally prefer active, as long as the fees are reasonable and the strategy is sound I think you will win in the long run – and in more conservative strategies like Quality or Value investing you will usually find that there are benefits, the biggest being lower volatility.

For example, our International fund was only up 0.2% in January while the market was up 1.5%, but then in February so far it is up 0.6% while the market is down 1.4%. The net effect is similar, but the ride is a lot smoother.

I also think there are benefits from tailoring the active share allocations with the asset allocation.

But, are there active fund managers who will take any outperformance in fees? Absolutely. If you are paying your investment manager 2 and 20 (a 2% fee and 20% of any outperformance) then the odds of you underperforming are good unless your manager is exceptional.

Choosing to stick with passive or index funds is not a terrible option. You will never do better than average, but you won’t do worse either – and the fees are low.

Asset Allocation is really, really important

Regardless of whether you choose active or passive, the bigger decision is asset allocation.

There is no passive option here. There isn’t an index that takes the decision away from choosing whether to invest in cash, bonds, domestic shares or international shares.

The closest you can get is a “strategic” asset allocation, which basically looks at long-term averages. You will find this in most robo-advisors. But you may have to wait a long time to get average returns – strategic asset allocation doesn’t consider currency or bond rates and the risk of investing at the wrong point in the cycle. It could be 10 or 20 years before the averages revert.

And that’s the key place I think a good professional manager can add value to retail investors.

Your brain is actively working against you

What is clear from the studies is that the average investor in the heat of the moment makes poor investment decisions.

The media doesn’t help – they generally only report two things: (1) the markets are up a lot and you should have bought last week, get in quick before you miss out (2) the markets are down a lot and you should have sold last week, sell now before you lose the lot

Getting perspective is difficult, especially if you rely on newspapers.

So, if you are choosing to do it yourself, make sure that you have a plan and stick to it. Most investors don’t, and get carried away in the good times, and become overly fearful in the bad times.

Damien Klassen is Head of Investments at Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.