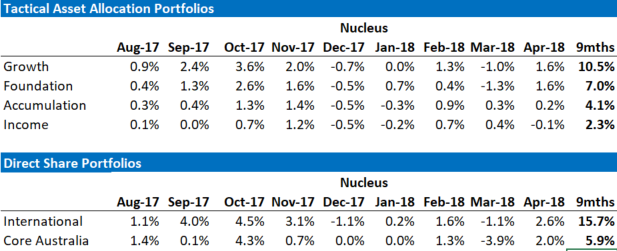

April saw markets bounce back from a poor March, and our portfolios saw healthy gains with our international portfolio up 2.6% and both our Tactical Growth and Tactical Foundation funds rising 1.6%. International shares were aided again by a falling Australian dollar – over the last 3 months the weakness in the Australian dollar has added just under 7% to our international performance.

Our April performance was driven by a diversified mix of international investments. Neste (Finland/Oil Refiner) +25%, Merck (US/Pharmaceutical) +10%, Marine Harvest (Norway/fish farming) +11%, Michael Kors (US/Fashion Retail) +12%, DBS Group (Singapore, Finance) +13% were the standout performers, Semiconductors (Skyworks, Lam, Applied Materials) were the worst performers on the back of trade war concerns.

We are sitting on a considerable cash balance in all of our Tactical portfolios – our Tactical Growth fund targets a 10% exposure to cash and bonds, our weight is currently 34%. We have even more cash in the more conservative funds. We have been holding part of that cash in a range of international currencies and so have benefitted from the falling Australian dollar.

Investment Outlook

The fundamentals for shares look good, valuations don’t. Which, despite all of the ups and downs of the last few months is largely where we have been for the past year.

There are two ways to “cure” high valuations: higher profits or lower stock prices. The pace of profit growth has managed to outstrip prices for the last few months, but in the latest quarterly results, we are starting to see some of the excitement being tempered. By this I mean that earnings growth is still very strong, but not as strong as expected last month (except in the US):

Often the last stages of a bull market can provide strong returns, however the risks are elevated and you don’t want to hold on too long. Our tactical asset allocation continues to be based on getting as much exposure as we dare to over-valued equities that continue to get even more over-valued while maintaining protection in case it all unravels.

To be clear, we don’t think that we have reached the end of the current investment cycle, especially so as the long-awaited Trump tax cuts are on the verge of triggering a late-cycle US boom.

Can this be derailed by a trade war? Yes. We are treating Trump’s trade war as mainly posturing, but there are clear dangers if it becomes something more.

March Performance

The returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees. See performance section below for relative returns.

Currency

The effect of an overvalued or undervalued currency is usually recognised when the currency makes it’s move and for a few weeks afterwards but then seems to be largely forgotten.

I take the view that undervalued or overvalued currencies for most supply chains:

- Are quickly incorporated for commodity products

- Take a lot longer to have an effect for more complex supply chains or services

For example, if Boeing uses a European supplier for a part on their planes, then the Euro rising 10% over a few weeks is unlikely to see Boeing change suppliers immediately. However, leave the Euro at the elevated level for six months or so and then Boeing will start to look at other options – the less unique the part, the more likely Boeing are to switch.

In my view that is where Europe has been for about 18 months or so, and over April the effects have become apparent with Europe showing a number of signs of slowing and the Euro beginning to fall.

We have been exiting our European positions for a little while now, and the falling Euro and weakening economic picture are suggesting that this theme has some time to run yet.

Euro / US Dollar

The Way Forward

As a reminder, we look at the key themes facing our portfolios as being:

- China: Rebalancing is occurring, the question is how fast Chinese authorities allow it to occur.

- Trump: Taxes are through as we expected. Our base case has been that trade wars will be more hot air than follow through. The pressure has eased on this front, but remains a risk. May 16 is the next flash point when the US looks at Iranian sanctions.

- Europe: Grinding recovery. We are not expecting great things, but note the political risks have reduced. We also note that the high Euro is weighing on the economy and economic statistics have turned down. The major long-term issue is still the significant imbalances between Germany and most of the rest of the Eurozone.

US

Our core position is that Trump is trying to engineer a boom. It will not be sustainable and will likely be followed by a bust that leaves the US economy in a worse position but that is a future problem – positioning the portfolio for the boom is the current issue.

The proposed tax cuts are badly targeted by giving most of the benefit to the rich and to companies, trickle down is unlikely to work, the tax cuts are unsustainable, and they are only a short-term “sugar hit” for the US economy. But it is going to be such a huge stimulus that you don’t want to stand in the way of it as an investor.

So, we want to play the boom, keeping a sharp eye on the bust. Our portfolio positioning on this basis remains:

- overweight international stocks from an asset allocation perspective

- overweight stocks with US exposures – subject to valuation. The practical implementation of this has been buying non-US stocks that are exposed to the US.

China

In China data continues to weaken, suggesting that the rebalancing is occurring. A cut in the reserve rate in March and discussion of fiscal intervention might seem to some as a sign that the authorities want to return to debt-driven growth. Our view is that these measures are more about managing the downward glide path, potentially in the face of a trade war.

Over the medium term:

- the shift to consumption-led growth rather than investment-led growth will require a greater shift than many recognize. This shift will be a significant negative for commodities/the Australian dollar

- current growth rates are unsustainably high, inflated by rapidly increasing Chinese debt. The increase in debt has been required in order to hit the growth targets, so removing the growth targets will help refocus local party officials to more sustainable policies

- activity still seems to be slowing.

- the Chinese housing market appears headed into a soft landing thanks to macroprudential tightening so a possible path ahead for rebalancing is a muted not busting housing cycle that supports consumption while weighing on investment;

Our expectation is that China is going to continue to “glide” lower to try to normalize the capital expenditure to consumption in-balance that we discussed in our recent webinar.

It is our view that the Chinese economy will continue to slow over the coming years – Japanese style lost decades, and low inflation/deflation remain more likely than a dramatic bust, which means a grind lower for commodities and the Australian dollar.

Our portfolio positioning on this basis remains:

- considerably underweight Australian stocks from an asset allocation perspective

- underweight resource stocks within equity portfolios

Tactical Asset Allocation Portfolio Positioning

In our tactical portfolios, we own cash, bonds, international shares and Australian shares. We tend to blend these portfolios for clients so that each investor receives an exposure tailored to their own risk and income requirements.

The broad sweep of our asset allocation over the last 18 months was to ride the Trump Boom, switch into Europe in March / April last year as the US became overvalued and then switch back into the US as the Euro rallied and the USD fell.

We have been using rallies in stock markets to reduce our holdings.

We remain underweight shares in aggregate, overweight international shares and significantly underweight Australian shares.

Tactical Foundation Portfolio

Our tactical foundation portfolio is designed for investors with lower balances, it uses exchange-traded funds for its international exposure rather than direct shares. The reason for this is parcel sizes, you can’t buy half a Google (Alphabet) share directly and so we use exchange-traded funds which buy baskets of stocks instead. The tactical portfolio is a balanced fund, not as aggressive in its holdings as the growth fund nor as conservative as our income fund.

In February this fund increased by 1.6%. The fund continues to be underweight Australian stocks.

Equities

Our biggest call is underweight energy. In particular oil producers. This has not been a good call over the last six months, and our outperformance has been despite the underweight to oil rather than because of it.

We have been doing a lot of soul-searching on this call over the month. The broad overview is:

- Oil demand remains strong, and with (relatively) synchronized global growth we expect this to continue.

- The supply side is stronger. US production continues to reach new highs, Libya and Nigeria’s production recovered from interruptions. The lone negative is Venezuela continuing to decline. The ability of US shale oil to react quickly to higher prices means that supply is much more responsive than its been in the past. The US has now become an exporter of oil.

- On the political side is where we see most of the action. OPEC and Russia are withholding supply to keep the price high, and US bombing in Syria plus Trump threats raise the spectre of sanctions returning to Iranian production.

- On the trading side, speculators hold record balances. This can be read two ways: (1) everyone else is going long, the oil price is going higher (2) the oil price has been pushed to current levels by speculators and will fall when they unwind their positions.

So, the question from here is whether we hedge our risk to political events by buying oil stocks in the face of fundamentals that suggest the oil price should be materially lower. If the risk were greater or the oil price lower, I would probably hedge. Given the current situation and current prices, we are going to stay underweight oil. But the debate rages on.

Our sole holding in the energy sector, Neste Energy is up around 70% over the past few months, which has shielded our portfolio from the rising oil price. Neste is a Finnish oil refiner, making a significant investment in green technologies and is well regarded by a number of sustainable rating firms including being in the Global 100 most sustainable companies, the Dow Jones Sustainability index and CDP.

We are underweight financials – mainly as we can’t find US financials that are cheap enough to justify purchasing. A number of financials performed well this month – Bank of New York Mellon and DBS group were the stand-outs. Insurance continues to be a sore spot, but we are looking to continue to build holdings in the sector with the view that after such severe losses in 2017 that insurance premiums will rise significantly.

We have a reasonable tech / IT exposure. The rising spectre of a potential trade war saw some significant price falls in this sector. We are using to opportunity to buy some more. There are a number of smaller tech stocks that we own, in particular, a range of semiconductor stocks where we like the growth outlook. It is worth noting that part of the reason for Apple increasing the price of its latest phone is an increase in memory and components. This is a positive for semi-conductor stocks more generally, especially if a “feature war” breaks out in the smartphone space. We current hold a range of stocks that should be helped by this trend (Lam, Applied Materials, Skyworks, and to a lesser extent Cisco). We recently bought Alphabet (Google), Western Digital and Micron following recent price falls.

Performance to date

Portfolio performance can be cut a number of different ways. At its most basic level, you should care about the total return. At the next level, you should care about the total return relative to some sort of benchmark.

As you dig deeper, you should also be interested how the return was achieved – for example if your fund manager is taking lots of risk but only performing slightly better than the market then you should be concerned. Similarly, if you can get market returns but at a much lower risk then that may be an appropriate trade-off.

Our portfolios to date have been both out-performing benchmarks, and taking less risk. The disclaimer is that they have only been running for nine months, and that is not enough time to make definitive judgements.

The returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees.

Epilogue

In summary, our view continues to be that Australian investors are better off holding international investments at this point in the cycle.

We retain relatively large cash balances to hedge against volatility and to look for a cheaper entry point. If markets continue to be weak then we will look to buy more equities. We are concerned about the potential for trade wars, which will be a key focus for us over the next few months.

Our intention is that our portfolio is positioned to take advantage of our key themes but minimise risk in the event that our themes take longer than expected to resolve themselves.

We usually find that big picture macro themes take a long time to resolve themselves in financial markets, but when macro theme resolve themselves they do so quickly – usually too quickly to reposition your portfolio if you are not already invested.

Damien Klassen is Head of Investments at Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.