The Australian SMSF Landscape

The Australian SMSF Landscape

We recently ran a webinar entitled the SMSF Asset Allocation Master Class in which, as an introduction, I thought I might provide a snapshot of the Australian SMSF landscape. The following graphs have been be created from an ATO dataset who publish SMSF statistics quarterly, the most recent being Jun 2017 which was released a couple of weeks ago.

Fast facts from the report:

The number of Self Managed Super Funds (SMSFs) increased last year by 5% to 596,516

The number of SMSF members increased last year by 5% to 1,124,453

The estimated value of SMSF assets is $696.7 billion (up 10% over the year). Total assets over the last 5 years have risen 63%!

The top five asset types held by SMSFs by value are

- listed shares 30%

- cash and term deposits 23%

- non-residential real property 11%

- unlisted trusts 10%

- other managed investments 5%.

There appeared to be enormous drop on Windups for the FY2017 which the Australian Tax Office (ATO) have clarified is typical due to a gap in confirmed windups and will be corrected in the next few releases.

For the remaining comparisons, I will use only a couple of segments of the data, being SMSF’s with $200k - $500k net assets, versus $2M - $5M. I like to use these segments as generally you find the first segment being a ‘Mums and Dads’ typical balance. The latter segment is relevant as, at this level of assets, you would typically find some type of professional management, and can help to throw some light on where assets are invested ‘at the big end of town’.

Cash and Term Deposits

Given the ‘lower for longer’ attitudes coming from the Reserve Bank over the last couple of years, it is unsurprising to see a shift out of cash and term deposits although a 14% drop over 5 years is remarkable. Safe to say that for most SMSF’s in the lower range, holding term deposits, after SMSF costs are starting to fall out of favour. As rates stay lower for the duration, it will be interesting to see if holdings plateau or continue the decline.

Listed Shares

The listed shares class in the report is filled with intrigue, as it *may* contain international assets such as exchange-traded funds that give overseas exposure, as well as Government listed bonds etc. I have asked the ATO for comment on the actual contents of this class, and they have commented that the onus is on the person submitting the return to make the distinction. Needless to say, there has been a resurgence in the smaller SMSF’s with a continued decline in the larger ones.

Total Overseas Assets

International assets are broken into Shares, managed investments, property (residential and non-residential ) and other. For ease of understanding, I have lumped all the categories in together as a total. This might seem bold, however as you can see the percentages are very small. Overseas Shares typically makes up about half or more of all overseas assets. As mentioned above, there is some conjecture as to where all international SMSF investing is actually categorised but assuming these are true, discrete internationally held investments, it shows a glaring paucity of exposure to the remaining 98% of world markets.

Residential and Non-Residential Real Property

Unsurprisingly, in the lower valued SMSF’s there has been a marked increase (22%) in residential property holdings over the last four years. More surprisingly has been the increase in the larger valued SMSF’s – with 28%, albeit off a lower base. Also interesting as always is the difference in ownership of residential property in the two cohorts, which you might assume comes from a number of factors. A couple of obvious examples being for those ‘with means’ property could be held outside of the SMSF or have a dimmer view of the long-term prospects of residential property in Australia.

There is a significant difference however on non-residential property in the larger funds. From my experience, this may be the result of small and medium business owners with SMSFs who have purchased their commercial property within their fund and are currently leasing it back. This strategy can work well for some (although we do note that your assets are highly concentrated) but can be quite involved, meaning further evidence of a professional hand at work.

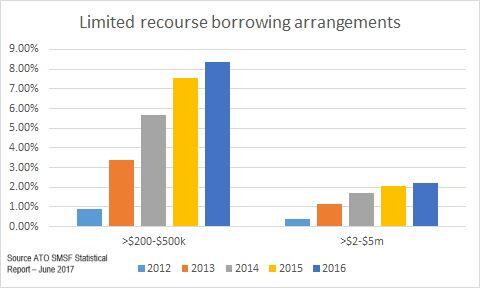

Limited Recourse Borrowing Arrangements

Now my favourite. Obviously, the money supporting the rise in the residential property needs to come from somewhere. Clearly, the stats are supporting that it comes from debt, with the smaller cohort up 11% on the year, and a staggering 843% (!) over 5 years. Once again the larger sized funds seem to also be on the move, however by a much smaller degree.

For those who have been following this year's federal budget, there were a few changes slated for Limited Recourse Borrowing Arrangements within SMSF's, however, these had less to do with obtaining them and more to do with tightening the rules around them, particularly if borrowing was not done on commercial terms. Labor went to the last election with a promise to ban borrowing in SMSFs, and I am starting to think they have a point!

How we view correct asset allocation in a portfolio

Part of the basis for naming our company stems from the fact that we see what we do as the 'nucleus' of an ideal portfolio. Large, well-researched portfolios containing great quality companies and bonds. Add to this a macroeconomic overlay for asset allocation that is reviewed daily and we see it as a perfect place for the majority of an SMSF's assets. This then leaves 'the fun part' for those who wish to spend the time researching and investing in the more volatile and specialised asset classes like micro caps, hedge funds and property.

Tim Fuller is Head of Operations at the Macrobusiness Fund, which is powered by Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Tim Fuller is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.