Kid's Investments: not like when you were young

In recent months, I've had an influx of clients and friends asking about setting up share market investment accounts for children. Direct indexing, fractional shares, and trading with no fixed costs make it much more attractive to invest in shares than it has been in the past.

Ten years ago, needing to pay $10 or $20 every time you wanted to trade meant that progressive savings plans weren't worth the effort. There is no sense in investing $200 a month if you lose 10% on day one to trading fees! Nor was it worth investing in direct shares with smaller amounts if you couldn't even buy one share. Your $200 monthly savings would need to wait for three months just to get a solitary Microsoft share.

But that is no longer the case. Technology has changed the fee equation.

Higher risk, suits a longer timeline

Now, shares are riskier than most other assets. But over the longer term shares have almost always provided the best returns. Cash is one of the safest assets. And over the long term cash has typically provided the worst returns.

Children presumably have a much longer time horizon for investment than most of us.

So, the irony is not lost on me that the focus for children has traditionally been short-term savings accounts rather than longer-term assets like shares.

What are the tax issues?

Setting up investment accounts for children is relatively simple, but there are a few tax implications to be aware of.

1. Do you want a formal trust? These are mostly about asset protection or where there has been an inheritance or compensation for an injury. If we are talking hundreds of thousands of dollars then you might think about this. There will be significant annual costs to this option. For most, the answer to this question is no, you will just open an individual account with the adult's name.

2. How do you set up the account? For most platforms, the account will be in the name of the adult; some will allow you to tag the account "as trustee for" (often shown as ATF). It is important to have the account beneficially owned for the child to ensure that when you transfer the shares, it is not a capital gains event.

3. What tax file number can you use? From the ATO:

If the shareholder is (a) the child, quote the child's TFN (b) parent, as trustee for the child, and no formal trust exists, quote the parent's TFN.

First, you may be restricted as to which tax file number you are allowed to use.

If the adult is using the dividends or frequently adding money or making all decisions then the adult may be deemed to be the owner anyway. It can get complicated, see here for the ATO website for more. But the good news is that it doesn't make that much difference, and often it is better to use the adults tax file number anyway.

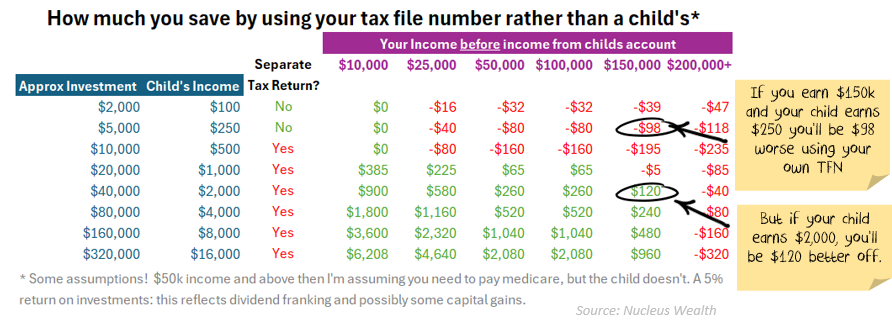

4. What tax file number should you use to keep the tax rate low?

The simple answer is that for most people you probably want the account in an adult's name in trust for the child with the adult's tax file number. That way you don't have to do an extra tax return and if your income is below $200,000 in any year you will likely end up in front over time. For the more complex answer, read on...

Keep in mind this is at 2025 tax rates and rules. They will change! And your tax circumstances might be different.

See the table below. In summary, using the child's tax file number may be better if (a) the child will always earn less than $416, or (b) the adult will typically earn more than $200,000 and (c) you either like doing extra tax returns or you can get them done cheaply. Otherwise, you are probably better off using your own tax file number or partner's.

Keep in mind that if the child earns more than $416 you need to do a tax return for them. If the child earns franking credits that you want to claim then you will need to do some form of return (it doesn't have to be a full return). Tax returns aren't free, even if the only cost is time. This means often you are better off simply leaving the investment in your name.

The other thing the table shows is that using a child's tax file number can give you small benefits under various scenarios. Using the adult's tax file number can generate much larger advantages, particular if the adult is on a lower salary or if the adult doesn't work part of a year. And finally, government tax policy has been designed to discourage people from shifting investments to kids to save money on tax. So, putting the share in the adult's name is probably the lower-risk option for changes in tax rules.

Give me an example

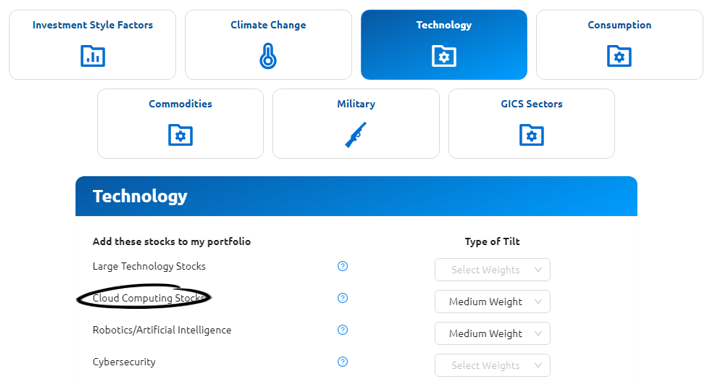

Say you want a $1,000 direct index portfolio with the top 75 stocks globally and plan to add $200 per month.

Add a small tilt towards artificial intelligence and cloud computing.

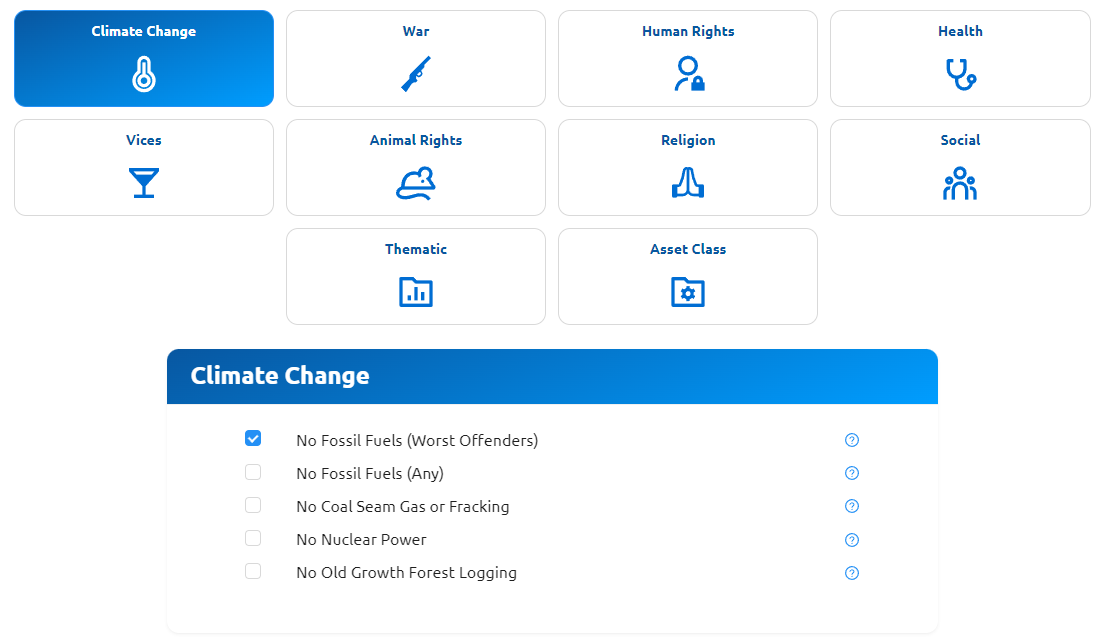

And you want to exclude the worst fossil fuel offenders:

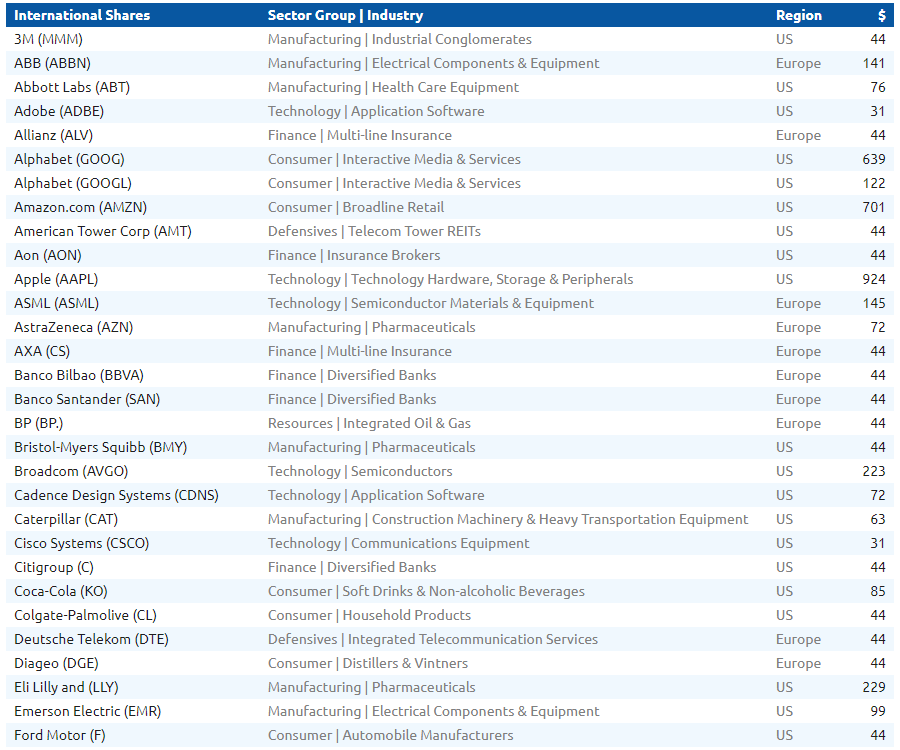

The portfolio will look something like this:

see portal.nucleuswealth.com for the full portfolio and exclusions.

Fees

- Your initial transaction cost will be 99c (0.099%).

- Adding $200 a month will cost you 20c (0.099%) in transaction costs

- Monthly admin and management fees of 0.33%p.a., decreasing as you add more.

- There are no underlying ETF or fund charges as you own all the stocks individually.

The upshot

Technology has changed. Fees have changed. The way we think about savings for kids should also change.

For most people, you probably want the account in an adult's name in trust for the child with the adult's tax file number.