A Wile E Coyote moment for Aussie House Prices

For a few weeks in late January and early February, stock markets suspended belief. Pundits on every channel emerged, suggesting a small economic dip followed by a massive stimulus package meant it was time to bid expensive stocks even higher. Meanwhile, in the real world:

- Earnings growth had already stalled.

- Valuations had reached lofty heights not seen since the tech wreck of 2000

- Coronavirus was unchecked outside of China. Cases were doubling every few days.

- Lockdowns of the Chinese economy threatened supply chains around the globe.

- Travel bans on students and Chinese travellers threatened revenue in oil, tourism, restaurants and education across the world.

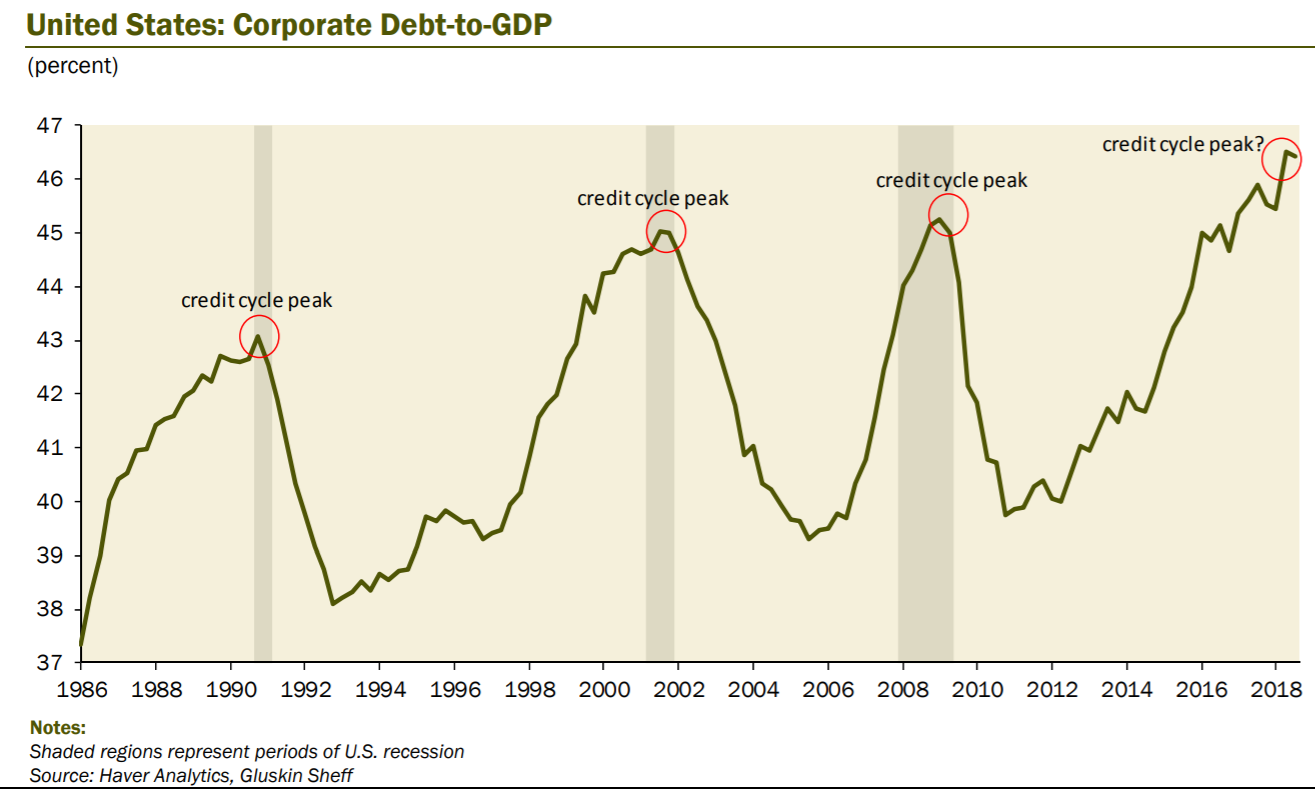

- Corporate debt, at record high levels, continued to be ignored.

The attitude was that the share market was bullet-proof, the Fed had its back and that all investors had to fear was fear itself.

In our portfolios, we had assumed the brace position. Then we spent four weeks peeking between our fingers wondering why we hadn't crashed yet. It was a Wile E Coyote moment for share markets:

Picture via Vox

Picture via Vox

The boom had run out of road. It was suspended in mid-air waiting to fall.

Now it is housings turn

Australian housing is contending with its own Wile E Coyote moment.

Auction clearance rates are in the 80s. Prices are rocketing upwards despite a surge in listings. Real estate agents are wondering if it is once again a sign of failure to be seen in a 5-series Beemer rather than a 7-series.

Pundits on every channel have emerged, suggesting a small economic dip followed by a massive stimulus package means that it is time to bid expensive houses even higher.

Meanwhile, in the real world:

- Central banks around the world are cutting rates to try to get in front of a looming economic shock

- Corporate debt markets are shut. Corporate debt levels are at record highs. Corporate interest rates are spiralling higher. Supply chains have been smashed for manufacturers. Demand has been smashed for services. The probability of a corporate debt crisis is high.

- Coronavirus lockdowns are circling the globe. There is no short term fix.

- Even the "economy is doing great" Australian government is preparing the biggest fiscal stimulus since the financial crisis to fight off looming increases in unemployment

The attitude is the housing market is bullet-proof, ScoMo has its back and that all investors have to fear is fear itself.

I get it. Banks had the debt hand-brake on in 2019 as a Royal Commission demanded they lend responsibly. But in 2020, egged on by the Treasurer and APRA, the banks were falling over themselves to get back to the irresponsible lending of the 2012-2017 era. The boom was back, baby!

Unemployment holds the key

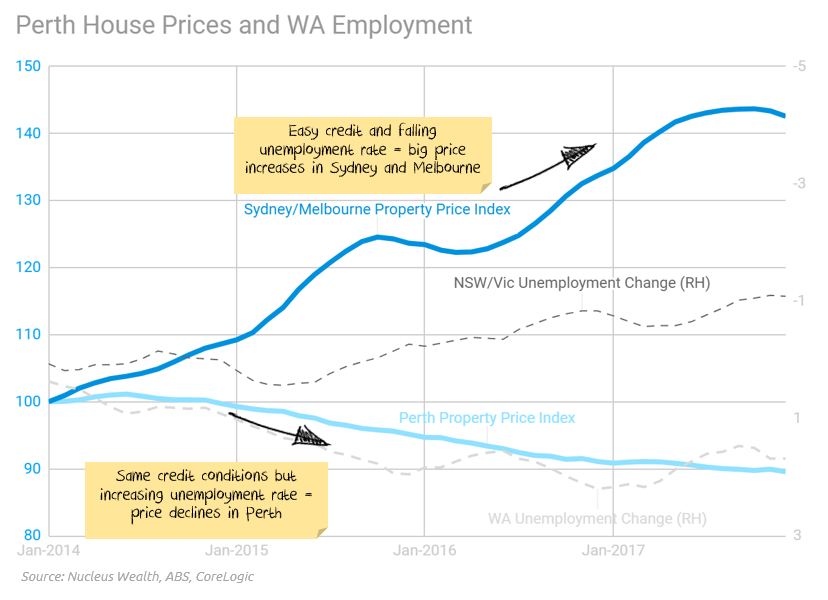

But, as much irresponsible lending as possible won't increase house prices when unemployment starts rising. Perth showed us that during the same 2012-17 period:

We posted a housing return calculator here a few months back. The overall conclusion was that after entry and exit costs, it was going to be challenging to beat the cost of debt under the best circumstances. Circumstances are not going to be the best.

They are looking awfully like the worst.

The government response

A globally co-ordinated massive fiscal stimulus might change my mind. But in the current fractured political environment, I'm going to file that under "I'll believe it when I see it".

Our regulators, governments and central bank have wasted most of the good policy options in a desperate attempt to hold and already expensive house market at high levels. Now we have a genuine external shock, most of the remaining policy options are bad ones.

I have no doubt our housing-obsessed government will try many of those policy options. But they won't work.

Housing booms don't normally finish because governments want them to. Booms usually end in spite of governments (captured by vested building interests) doing all they can to extend the boom.

The most likely outcome is the same here. The real unknown is how much longer the housing market will levitate before realising there is no solid ground underneath.