Albert Edwards at Societe General is always worth reading.

US growth expectations have crashed in the wake of recent weaker-than-expected data.

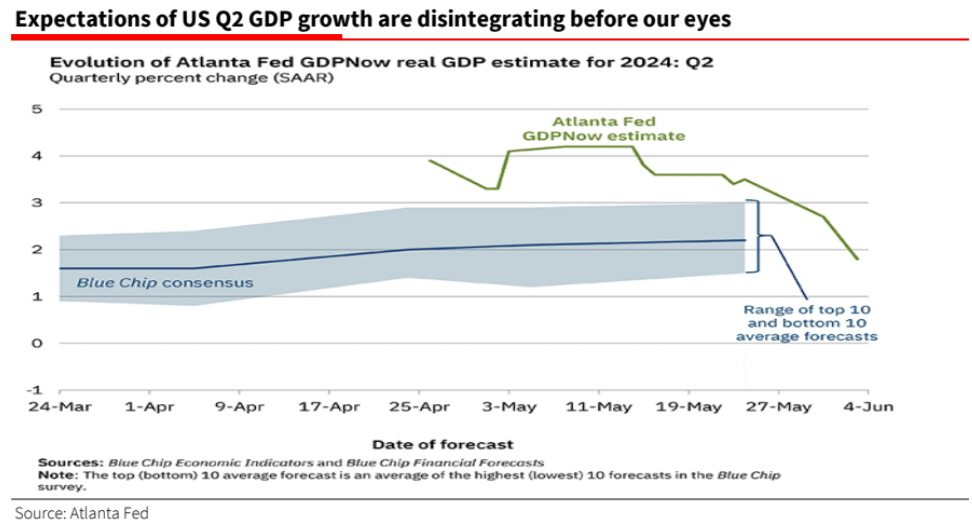

The closely watched Atlanta Fed GDPNow projection for Q2 has almost halved in a week from a heady 3.4% to a headless 1.8%.

This comes hard on the heels of downward revisions to Q1 GDP to 1.3%.

What’s going on? Surely that recession which almost everyone has given up on isn’t about to hit?

That was quite the downward revision to US Q2 growth expectations in just one week (see chart below).

Most attention was drawn to the surprise fall in May’s manufacturing ISM to 48.7 from 49.2 in April.

Many waved this data point away as either a one-off aberration and/or with the usual argument that manufacturing is only a small part of GDP.

But that weak data comes hard on the heels of weak consumption and trade deficit data, both of which chopped ½% off Q2 GDP growth estimates.

Markets do not move on outcomes alone, but on how they differ from expectations as signalled in market pricing.

In early 2023 it was almost impossible to find an economist who thought the US would avoid recession.

But to much embarrassment, the most widely predicted recession in history failed to materialise.

Hence as we moved into 2024 it was difficult to find an economist who was still willing to stick to their recessionary guns.

Certainly, the macro data looked perky to the point that anticipation of a ‘No Landing’scenario increased, whereby the Fed might even have to resume hiking rates.

Combined with increasing analyst optimism on the earnings outlook and inflation gradually sliding towards the 2% target, no wonder all-time highs were hit in the main equity indices.

‘Proper’equity bear markets (falls of 30%+) only really occur in recessions and so that is what equity investors fear most–especially against expectations of continued economic recovery.

Yes,the US authorities have proved adept at avoiding an archetypal macro triggered recession since the 2008 Global Financial Crisis (GFC), pursuing either easy money (post-GFC) or extreme fiscal expansion (last year).

But is investors’ luck about to run out?

Even if Armageddon looms, I guarantee the investment air will be filled with the sound of the bulls singing their soft-landing siren songs.

And beyond that, I can also guarantee you will hear that any recession will be shallow as the Fed have ample firepower to slash rates… just as they always did in past recessions although that never prevented a collapse in the equity market.

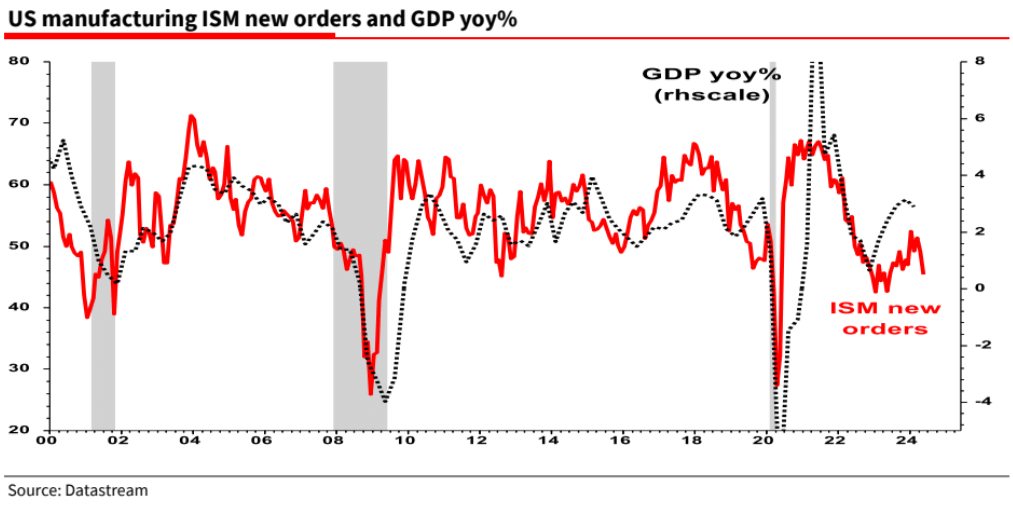

It wasn’t the 0.5pp slipin May’s headline manufacturing ISM that spooked investors, but the 3.7pp plunge in the new orders component to a lowly 45.4 (see chart below).

And although many may dismiss the importanceof the manufacturing sector for the overall economy, it is undeniable that overall GDP ebbs and flows closely with it.

No surprise then that fear of recession is resurfacing.

US GDP has recently bucked its historical relationship with ISM manufacturing new orders (seeabove),likely due to unusual rotation out of goods spending into services in the aftermath of the Covid lockdowns.

That ‘revenge spending’ has now abated and the usual relationship will likely reappear, putting the sharp rise in US growth expectations over the last year at risk of reversal.

Bond investors weren’t just buoyed by May’s weaker growth data.

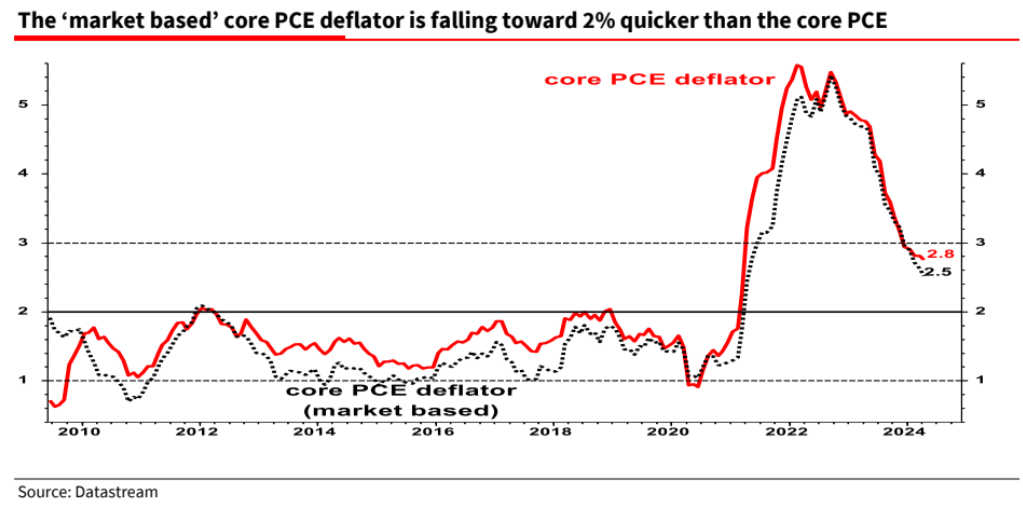

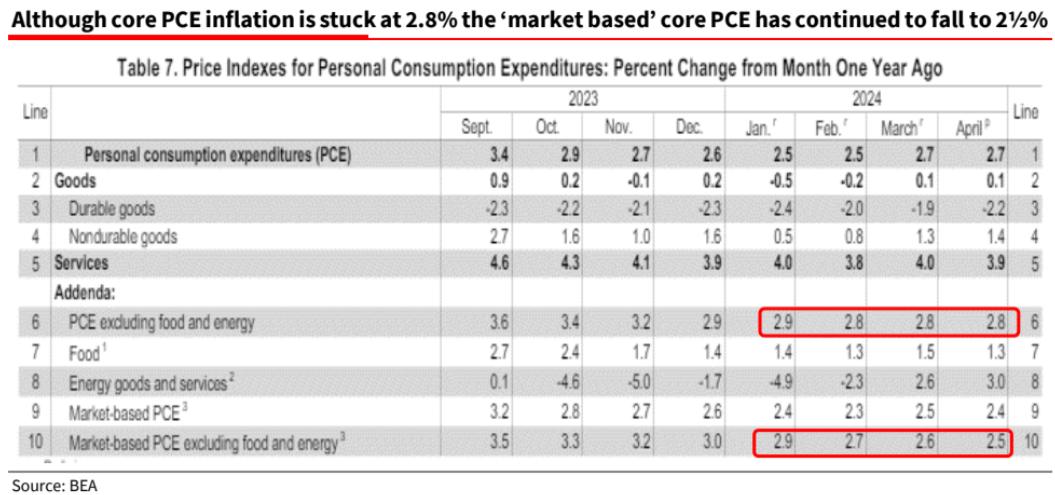

The US PCE deflator continued its drift down toward the target 2%.\

Indeed, we are already down to 2.5%on one key measure.

What does the Bureau of Labor Statistics (BLS) exclude to get the ‘market based’ measure of PCE inflation?

Basically, it excludes data it has to ‘make up’ like finance & insurance services and non-profit entity spending (think election campaigns)–for a comprehensive BLS explanation see here and this excellent analysis by Matthew Klein (H/T FT’s Rob Armstrong).

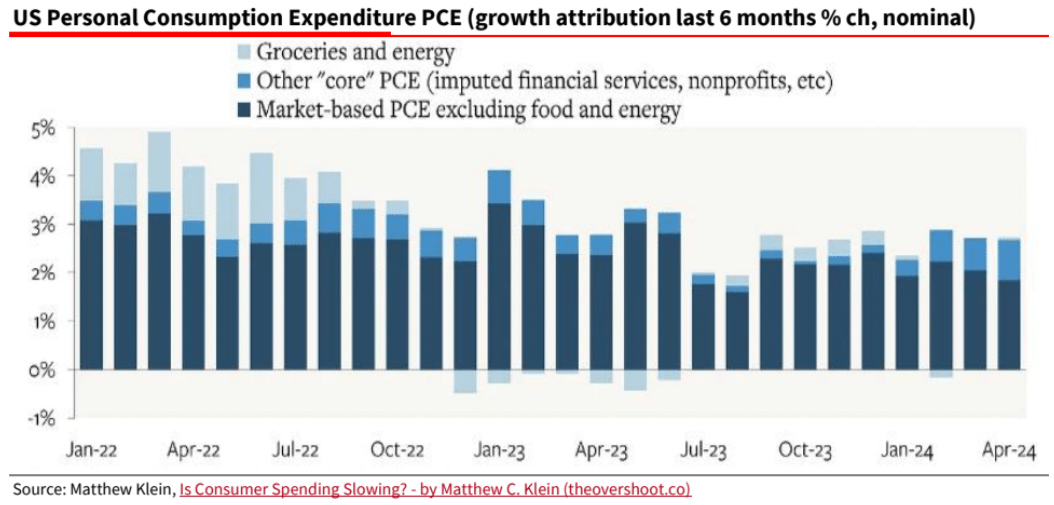

Klein also points out that much of consumer spending’s apparent strength could be ‘fake’; he explains: “Intriguingly, more than 40% of the growth in real PCE in 2024Q1 is currently attributed to finance and insurance plus net nonprofit spending.

That is the highest share coming from this subset of (mostly) imputed categories since 2011.” (see chart below).

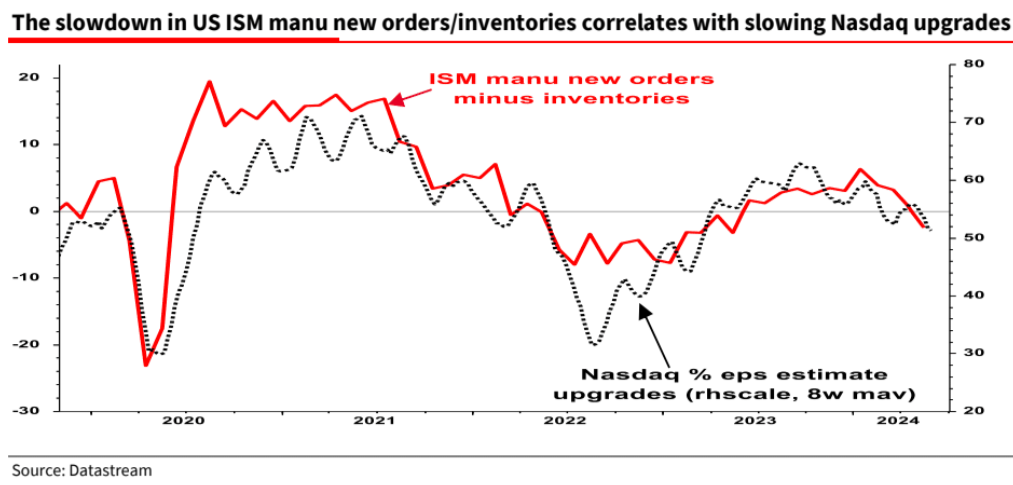

As GDP growth disintegrates, equity investors should be worried.

Equity markets had been driven higher by eps upgrades which correlates pretty well with the excess of ISM new orders relative to inventories, but this key indicator is now slowing fast.

That recession might yet arrive after all.

That last chart is a clangor. US recession is no longer my base case, but I remain long bonds on the notion that the soft landing is a material slowing and, therefore, disinflationary.