Trump broke the Shiller P/E. Here is a simple fix.

For many value investors, the Shiller Price/Earnings ratio is the holy grail. There are a number of problems with the ratio which are making it look way more expensive than it is. If we fix just some of the least contentious issues, the Shiller P/E looks almost 25% cheaper.

That (still) doesn't make the market cheap now. But it does explain why the Shiller P/E (also known as the Cyclically Adjusted Price Earnings or CAPE) has spent the last five years telling all and sundry that the S&P 500 was expensive throughout a marathon bull market.

I have two easily solvable criticisms of the measure:

- Tax rates have changed. The Shiller P/E implicitly assumes tax rates will return to pre-Trump levels.

- Buybacks have become an increasing part of the investment landscape. There is a simple way to account for this.

There are other, more controversial changes, but more on them in a later post.

Shiller P/E Background

The idea of the Shiller P/E is to give us a longer-term look at actual earnings without being distorted by short term issues. Or relying on perennially optimistic analyst forecasts.

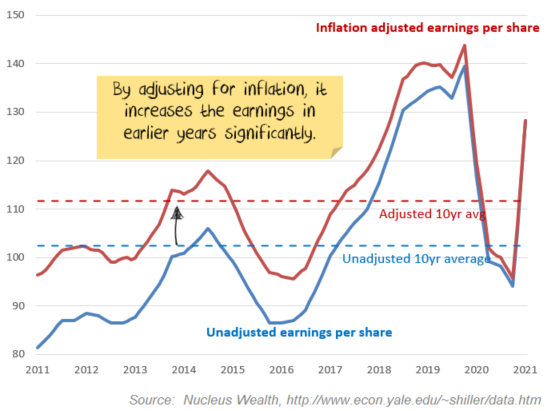

So, the Shiller P/E takes a ten year average of earnings. The trick is that earnings from ten years ago are not the same as earnings from today due to inflation. And so the measure adjusts to get the earnings in today's dollars:

Effectively, the Shiller P/E is saying ten years of inflation-adjusted earnings per share are a reasonable measure of the earnings power of the stock market.

To stay updated on the rest of this series and be notified of each part, sign up to receive email updates from us via the form below:

The number one investment problem

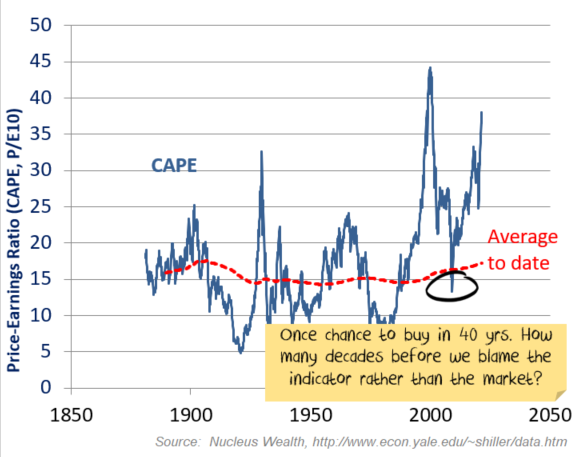

Backtests typically show the Shiller P/E does a good job of predicting long term returns, although it isn't a good timing tool.

But, the real problem with the Shiller P/E for a value investor is that it keeps saying: "don't buy now". And the S&P 500 keeps rising.

Say you are a value investor who only wanted to own stocks when the Shiller P/E was below its average. In the last forty years, you would have owned equities for seven months.

A simple change in Shiller P/E measurement

Rather than averaging real 10 year earnings per share, I'm suggesting:

- averaging 10 years of pretax earnings (not per share)

- apply today's tax rate

- apply today's number of shares

A very subtle difference in definition. But a huge difference in outcomes.

Changing tax rates

One problem with the Shiller P/E is taxes. If I look over the last ten years in the US, six of those years had a corporate tax rate of 35% and four have a tax rate of 21%. Effectively, the Shiller P/E is telling us the right tax rate to value a company is (35%x6+21%x4)/10=29.4%.

It doesn't add up. Today's investor does not expect a 29% tax rate, they expect a 21% tax rate.

It makes much more sense if we:

- Take an average of the last ten years of pretax profits per share.

- Apply the current tax rate to indicate the after-tax earnings per share an investor can expect.

Buybacks

Buybacks were illegal in the US prior to 1982. The rise in buybacks (rather than dividends) in theory creates earnings per share growth by decreasing the number of shares.

Shiller acknowledges this and offers an alternative that re-invests dividends. I think he is trying to solve a different problem. So, I disagree with his methodology. At a minimum, this adjustment should make the S&P look cheaper because there are fewer shares now. His method makes the S&P look more expensive.

It makes much more sense if we:

- Take an average of the last ten years of earnings (i.e. not per share*).

- Apply the current number of shares to indicate the earnings per share an investor can expect.

* This is a bit of an oversimplification. Basically, we adjust for shares bought back. More on this in the next post.

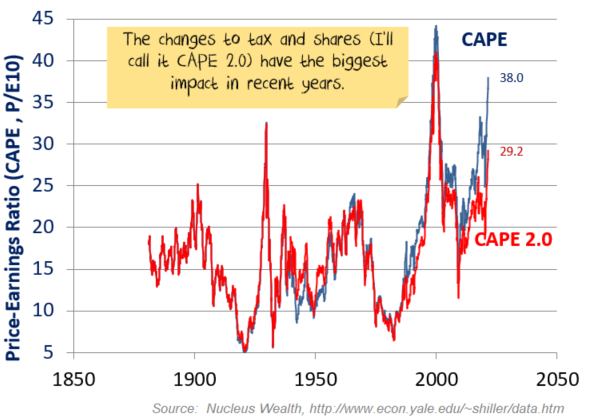

Effect on valuations: CAPE 2.0

The changes reduce the current Shiller P/E from 38x using the total return method to 29x. Still historically expensive, but 23% cheaper than the Shiller P/E currently suggests. And it gave the value investor many more chances to invest in recent years.

See ie_data_klassen_adjustments for Shiller's spreadsheet with my modifications.

Homework for advanced CAPE students

There are some other, more contentious changes that bear consideration:

- The rules around writedowns have become significantly stricter in the last 20 years, biasing toward writedowns.

- Some suggest differing re-investment rates might change the future expected returns. I disagree.

- Over the longer term, differences in inflation rates affect reported profits in ways not currently captured.

- Should you count negative earnings? For example, is portfolio A with one stock earning $100 and another earning -$50 worth the same as portfolio B with two stocks earning $25 each?

- Does the cost of trading matter? In 1970, commissions were close to 1% (one direction) and spreads were much wider. Now, both are closer to zero. Should we account for that in our measurement?

I'll cover off on these, plus more issues with tax in a second post. In the final post, I'll look at the Australian market.

To stay updated on the rest of this series and be notified of each part, sign up to receive email updates from us via the form below:

Quick postscript on earnings growth

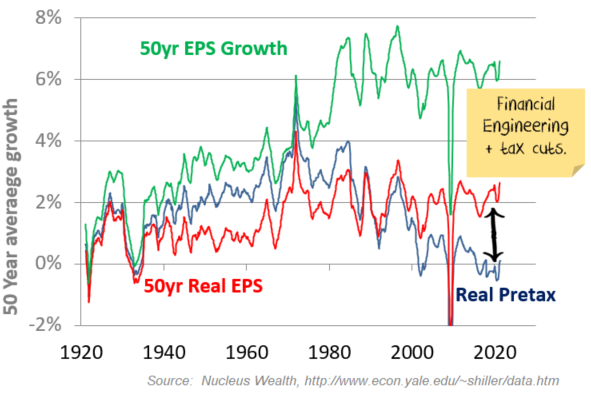

By doing the above, we generate some interesting stats on earnings.

Nominal 50-year earnings growth on the S&P to date was 6.6% per annum. Plus an average 2.9% dividend yield gives us 9.5% before valuation changes. Which sounds good.

It is actually the opposite:

- Of the 6.6% nominal growth, 3.9% is inflation. Real growth was only 2.7%.

- But, of the 2.6% real growth, 1.7% came from buybacks, leaving 0.9% of actual dollar profit growth.

- Oh, but taxes have come down from 50% to 21% over that time. Tax cuts gave another 0.9%. Which leaves pretax profit growth of 0.1%.

Stocks have had much better half-centuries. 2-3% growth was pretty common for most of the century prior to 1990:

The pessimist might build up up an earnings forecast: 0% pretax profit + 2% from buybacks + 2% from inflation means only 4% profit growth going forward. Half of which is financial engineering. And they would probably have a dig about how much worse the results would have been further without even more financial engineering in the form of increased debt, aided by falling interest rates.

The optimist might go the other way, it has been a rough 50 years for earnings, surely the next 50 will be better?

Damien Klassen is Head of Investments at Nucleus Wealth.

Follow @DamienKlassen on Twitter or Linked In

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Nucleus Advice Pty Ltd - AFSL 515796.