What Frydenberg isn't telling you about Interest Rates and Banks

Treasurer Josh Frydenberg announced Monday an ACCC investigation into the banks not passing on interest rate cuts. I think the investigation will make a nice addition to ACCC's bookshelf. They can file it next Rudd's FuelWatch and Grocery Code of Conduct. The biggest question is whether the investigation is designed to be a distraction from looming economic problems or simply a distraction from the Royal Commission into Banking. But that doesn't mean there aren't investment consequences - a number of them affecting our "one economic question that matters" thesis.

For those with superannuation investments (where bank shares make up a large part of most funds), investments or a home loan it is important to understand the fundamentals of the banking industry.

Economics of lower interest rates

The general theory is the Reserve Bank of Australia wants to get more economic activity to decrease unemployment and lift inflation. By lowering the interest rate:

- Consumers with home loans save money. For a small proportion, this means that they can afford higher house prices and so bid up the value of existing houses. For other consumers with home loans, the cost savings and the confidence from higher house prices translate into greater consumption spending.

- It becomes cheaper for businesses to borrow to invest. The mix of more consumer spending and less expensive loans means that more firms invest.

The combination of the two is a virtuous circle that then employs more people, which creates more consumption and more business investment and so on.

However, both of these are reliant on the expectation banks will lend more money as interest rates fall. The problem is banks have different incentives in their business model: low-interest rates are not necessarily better. If interest rates are too low it can be a disincentive for banks to lend.

Bank Business Model

At the simplest level, banks are an asset/liability mismatch - banks borrow from depositors (and others) on a short term basis and lend it out for long periods.

So, banks make the most money when short term rates are low (borrowing is cheap) and long term rates are high (lending is expensive). This is called a steep yield curve. The actual level of interest is far less important than the difference between the two interest rates.

But, as many depositors know, banks stopped paying interest on most transaction accounts a few years ago. So banks can't lower interest rates on those accounts any further to reduce costs. This means lower rates don't decrease bank costs for at least part of a bank's liabilities. The other part of a bank's liabilities is more complicated. The short version of the story is yield curves are relatively "flat" (rather than the profitable steep curves), and so there isn't much relief on that front either.

The net effect: there isn't a financial incentive for banks to cut rates.

Bank Profitability Matters

Banks could, of course, reduce current profits by cutting rates more, but that means lower bonuses and lower shareholder returns. The Royal Commission into banking has shown many bankers won't even let the law get between them and a bonus.

With less cynicism, bank profitability is an important issue - we have seen this play out in other countries with low interest rates. If banks aren't profitable enough to expand lending then they won't. Regardless of how low interest rates are.

This is one of many conundrums Europe is facing. How to keep rates low enough to stimulate the economy but not send the banks bankrupt.

One more way to get banks to lend more

The Royal Commission blasted banks for lending too much to people who couldn't afford to it. The current government is urging all banks to do exactly the opposite and lend more money.

As I wrote recently:

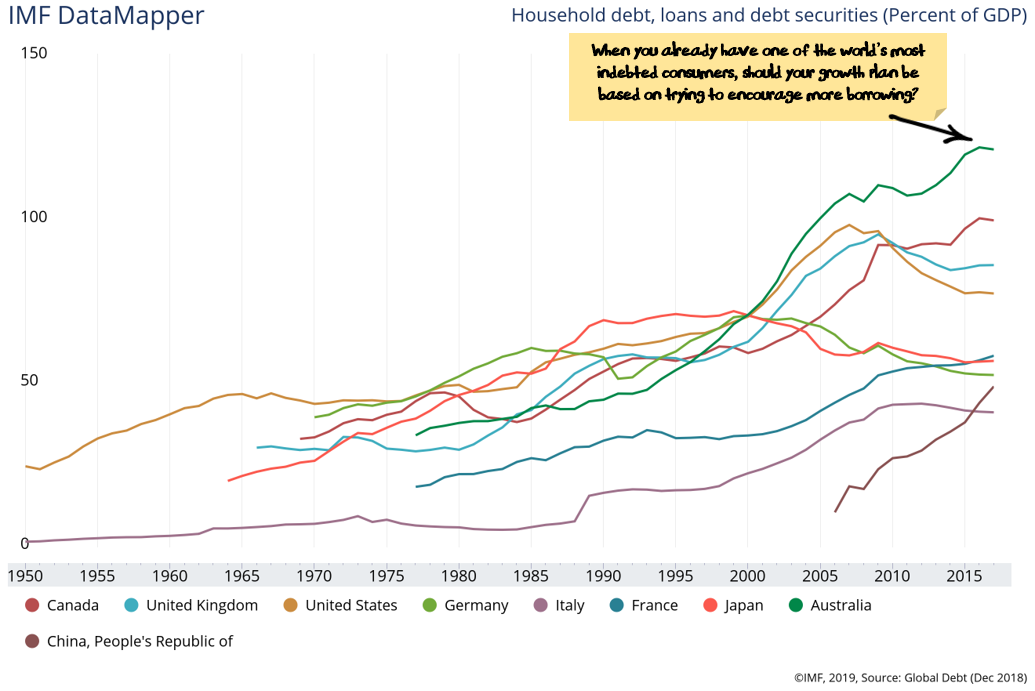

Is the Australian government really pinning it's growth hopes on getting the world's second most indebted consumer to borrow even more?

It is a (morbidly?) fascinating economic experiment that the government has launched, seemingly in concert with the regulators.

We know from examples in numerous countries over history that housing booms can occur when the regulators are asleep at the wheel. But there aren't many examples we can look at where the government are actively encouraging over-leveraged consumers to borrow more and the regulators to stay out of the way.

At the moment the plan has four parts, the first being relatively simple: target the main group not already geared to the eyeballs (first home buyers) and encourage them to borrow up to 95% of the value of a house.

The second part is more complicated. The royal commission into banking deemed the banks were breaching responsible lending rules. APRA (the regulator in charge) was pilloried for being too close to the banks and allowing banks to set their own standards. This slowed the meteoric rise in debt and saw house prices tumble. The current government's response has been:

- Three days after the election APRA announced it would loosening credit conditions and let banks calculate their own risk.

- A new five-year term was given to the head of APRA. The same head while the banks were deemed to be lending irresponsibly .

- The assistant Treasurer recently told The Australian Financial Review that he will press financial regulators to review their restrictions on bank lending to help ease a credit squeeze and to "get credit flowing" to home borrowers.

A cynical observer might think the current government's plan is to encourage banks to resume lending irresponsibly.

The third part of the plan is subtle. The Reserve Bank of Australia has been publicly begging the government to spend money on productive infrastructure in order to boost jobs and get wages to grow. The government is refusing. This effectively leaves the Reserve Bank no option but to continue to cut interest rates. And lower interest rates will presumably encourage Australia's indebted consumer to become even more indebted.

The fourth part is back to simple. When your existing citizens are too indebted to borrow more, you need to get more citizens. Budget papers are based on running record levels of immigration.

The ACCC inquiry into bank interest rates is a 5th strategy: pressure the banks to lower interest rates. I wouldn't quibble with those who argue it is more of a side dish for the 2nd strategy.

Investment Outcomes

On one hand, the ACCC inquiry into bank interest rates is simply a distraction. It is unlikely to uncover worse crimes than we have already seen through 18 months of Banking Royal Commission. And potentially it is a way to further delay the implementation of the Royal Commission's findings.

On the other hand, it is another clear indicator that finding more ways to get Australians to borrow money and stick it in the housing market is the number one agenda for the Federal Government. Regardless of the longer-term consequences.

The three main investment factors are that Australian banks:

- Earn some of the highest returns on equity in the world

- Are some of the most expensive banks in the world

- Look attractive from a yield perspective as interest rates march lower

The optimists suggest:

- You pay up for quality

- After brushing off the Royal Commission, banks are through the worst

- The housing market is now rising in Sydney and Melbourne, reducing the chance of bad debts

- Clearly the government is ready to roll out more policies to support the housing market and grow credit quickly

The pessimists suggest:

- As interest rates in Australia chase the rest of the world downward, returns will do the same

- If returns fall any further then dividends will be cut

- The housing market is vulnerable - the government and regulators are using all their bullets trying to hold house prices at high levels. In the event of an external shock, the tools to support the market will be more limited.

- There is still a rogue agency (ASIC) trying to litigate against the banks and actually enforce the Royal Commission findings. This could restrict credit once more.

- Forward indicators of construction have cratered. And there is a gap in the infrastructure pipeline over the next few years. There is the potential for job losses in this part of the economy to spread to the rest of the economy. We saw in Western Australia over the last five years that rising unemployment trumps easy credit.

In our superannuation and investment funds we are erring on the side of caution.

The return profile for Australian banks looks awfully like the return profile for houses: expensive, limited upside, considerable downside.

There are lower risk returns to be made elsewhere.