Superannuation Strategies for End of Financial Year (EOFY)

With the end of the 2020/21 financial year fast approaching, it is time to speak to your accountant regarding strategies to grow your long-term wealth within superannuation, to allow enough time to have them fully executed well before the June 30 cutoff.

Annual Superannuation Limits

Before considering any superannuation strategies, you should be aware of annual limits for superannuation contributions, and how much you've already contributed, to know which strategies can work for you.

Superannuation Contributions more than the annual limits attract penalties (such as additional taxes).

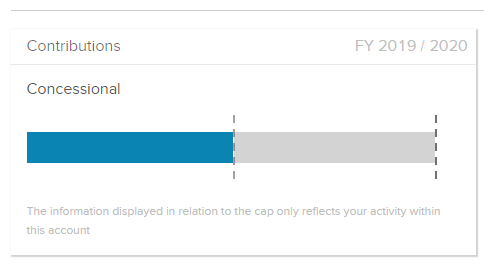

Existing superannuation clients should log in, then click on Accounts on the left, then super on the right, to see a breakdown of their superannuation Concessional (Before-Tax) Contributions so far this financial year, which will look something like this (hover over the section to know how much you have contributed, and what your “remainder” Concessional Contribution is):

Your personal situation

It is important to speak to your accountant regarding your personal situation as your eligibility can be affected by your age, sources of income, level of salary sacrifice, level of Superannuation Guarantee (SG) contributions (by your employer) and certain other employer contributions made for you, just to name a few.

Remember that in most cases you will not be able to access your superannuation until a Condition of Release (such as retirement) is reached, with few exceptions. So, you need to be sure of what you are doing before you start the process.

7 superannuation strategies you may want to consider for EOFY:

Click on each of the following to jump to that section for further details

- Tax-deductible super contributions

- Salary sacrificed super top ups

- One-off superannuation contribution

- Government Co-Contribution

- Spouse super contribution tax offset

- First home Super Saver Scheme

- Downsizer contributions

1. Tax-deductible super contributions:

The impact could be paying less tax (or a larger tax return), while saving more for your future inside superannuation. Personal tax-deductible contributions count towards your annual Concessional (Before-Tax) Contributions cap of $25,000 per financial year, with contributions made above these limits attracting additional tax.

You may be eligible to claim a tax deduction for your personal super contributions if you give a notice to the Trustee of your super fund that you intend to do so (either before the end of the financial year that you make the contribution, or before you do your tax return for that financial year), and have that notice acknowledged (the notice is required by your accountant when doing your tax return in order to claim a tax deduction).

2. Salary sacrificed super top ups:

This is where part of your before-tax wage or salary is paid into your super account instead of being received as take-home pay. The benefits include boosting your super to help you your retirement saving with the tax advantages depending on how much you earn.

To consider this option, talk to your employer to know whether they have this as an option, and if your salary sacrificed contributions will affect how much they are contributing as part of the 9.5% Superannuation Guarantee. Also, think about how much you can afford to take out of your pay packet. Remember, once you have committed the funds to Superannuation, under normal circumstances, you will not be able to access this money until you have met a Condition of Release- i.e. retirement.

NOTE: Salary sacrifice contributions, personal deductible contributions and employer contributions all count towards the same annual before-tax contributions cap of $25,000 per financial year. In the 2021/22 financial year, the cap is being lifted to $27,500.

From 1 July 2018, members can make 'carry-forward' concessional super contributions if they have a total superannuation balance of less than $500,000. Members can access their unused concessional contributions caps on a rolling basis for five years. Amounts carried forward that have not been used after five years will expire.

The first year in which you can access unused concessional contributions is the 2019–20 financial year.

3. One-off superannuation contribution:

Non-Concessional (After-Tax) Contributions are made from money you have already paid income tax on (e.g. cash you have in your bank account), and you won't be claiming a tax deduction for the contribution. Investment earnings within your super accumulation account are taxed at up to 15%. This compares to being taxed at your Marginal Tax Rate, which ordinarily applies to investments you may hold outside of superannuation. If your marginal tax rate is greater than 15%, this may be tax effective way to make investments for your superannuation.

The annual limit for Non-Concessional (After-Tax) Contributions is $100,000 per financial year (if your total superannuation balance is below $1.6 million at the start of the financial year). You may be able to bring forward three years of Non-Concessional (After-Tax) Contributions into one year (i.e. contributing up to $300,000) if you haven't triggered the “Bring-Forward” rule in the previous two years and your total superannuation balance is below $1.4 million at the start of the financial year. See your accountant for details.

4. Government Co-Contribution:

Middle to low income earners (with salaries less than $39,837 to a maximum of $54,837 in the 2020/21 financial year) can make contributions of $1000 or more of their after-tax salary (i.e. claiming no tax deduction for the contribution), with the government Super Co-Contributing of $500 if your salary was $39,837 or less. The co-contribution figure gradually diminishes as your salary approaches $54,837.

Age limits and maximum superannuation balances apply to qualify for the co-contribution.

5. Spouse super contribution tax offset:

You may be able to claim a tax offset for yourself if your spouse/partner’s assessable income is less than $40,000 in a financial year and you make a Spouse (or de facto) Super Contribution on their behalf. You can contribute a maximum of $3,000. If your spouse/partner’s assessable income is less than $37,000, you may be eligible for the maximum tax offset of $540. The tax offset is progressively reduced until it reaches zero when their income approaches $40,000. Your spouse’s superannuation balance needs to be under $1.6 million at the start of the financial year to qualify. Check here for further conditions.

6. First home Super Saver Scheme:

Starting from 1 July 2017 first home buyers have been able to make voluntary superannuation contributions to use towards a deposit for your first home under the First Home Super Saver Scheme (FHSSS). The total amount of either concessional or non-concessional contributions you can make and then later claim under this scheme is capped at $15,000 a year, to a maximum of $30,000 in total over multiple years. Only voluntary (Concessional or Non-Concessional) contributions, plus their associated earnings, can be released (subject to meeting eligibility criteria) from superannuation from 1 July 2018 under FHSSS.

7. Downsizer contributions:

From 1 July 2018, if you are 65 or over and planning on downsizing your family home of 10+ years, you and your spouse may be able to contribute up to $300,000 from the sale proceeds to superannuation as a downsizer contribution. Downsizer contributions do not count towards either your concessional or non-concessional contribution caps and your total superannuation balance is not a criteria to qualify. Check the eligibility criteria to make sure you qualify.

Visit the ATO website for information on criteria that qualifies you for the strategies discussed above, or the MoneySmart website for the latest information and for further ideas on how to grow your superannuation.

Considering switching your super? View our Superannuation offerings here