Apologies for the lateness of this report, we are still getting reporting systems ironed out with our portfolio provider – you will be hearing from us much earlier for the next monthly report.

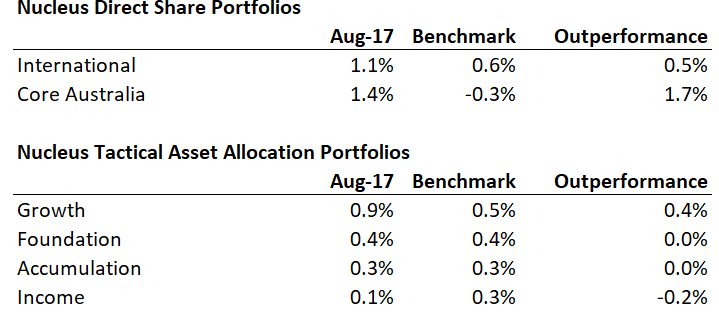

While some of the key trends that we are positioning the portfolio for moved against us last month (bonds and the Australian dollar in particular), stock selection came to the rescue, and all our portfolios outperformed their benchmarks over August except the income portfolio:

Source: Linear, Factset

The returns above include fees and trading costs on a $500,000 portfolio. The benchmark returns do not include fees. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase.

The Way Forward

Looking forward the key issues facing the portfolios at the moment are:

- China: Rebalancing is occurring, the question is how fast Chinese authorities allow it to occur

- Trump: Taxes are the next key decision point, and after failures in healthcare he is looking for a win. We are expecting there to be 2 facets – tax cuts and encouraging companies to bring back cash. Both are USD bullish.

- Europe: Grinding recovery. We are not expecting great things, but note that the number of political risks has reduced in recent months. The major long-term issue is still the significant imbalances between Germany and most of the rest of the Eurozone, but no real flashpoints at the moment.

China

Our base view remains that a rebalancing is required. China has been running capex at levels far greater than any economy has run before, and a normalisation of those capex levels is required.

Rebalancing will have significant ramifications for the Australian economy. We saw a preview of this in 2012-2015 when commodity prices declined significantly, as did the Australian dollar.

But this all changed in 2016. The rebalancing process stalled as lending increased significantly and commodity prices jumped significantly. This is not sustainable – as the latest IMF forecasts show:

It is our view that the Chinese economy will continue to slow over the coming years – Japanese style lost decades, and low inflation/deflation remain more likely than a dramatic bust, which means a grind lower for commodities and the Australian dollar.

There is considerable uncertainty over the timing, the actions following the communist party national congress in October will be key – especially growth in Chinese credit.

Our portfolio positioning on this basis remains:

- considerably underweight Australian stocks from an asset allocation perspective

- underweight resource stocks within equity portfolios

Trump Stimulus

Trump and the Republican party are having a difficult time passing legislation despite holding a majority of seats in both the House and the Senate. After a number of failures to get healthcare measures passed, tax reform is now moving to the forefront.

Our core position is that Trump is trying to engineer a boom. It will not be sustainable and will likely be followed by a bust that leaves the US economy in a worse position but that is a future problem – positioning the portfolio for the boom is the current issue.

The proposed tax cuts are badly targeted by giving most of the benefit to the rich and to companies, trickle down is unlikely to work, the tax cuts are unsustainable, and they are only a short-term “sugar hit” for the US economy, I understand all the negatives. But if it is anywhere near Trump’s promise then it’s going to be such a huge stimulus that you don’t want to stand in the way of it as an investor.

There are three parts, we don’t know which will be in the final package, but we expect at least some of the measures to pass:

- Company Tax cuts, currently proposed to be cutting the company tax rate from 35% to 20%. While this is a big change, many US companies already pay less than 35% in practice, and so we expect the effect on earnings will likely be around 5-10%% in year one and probably 1-2% stronger for a few years as companies restructure tax structures

- Personal tax cuts. Lots of simplification, the net outcome being largish tax cuts for higher income individuals, smallish tax cuts for low income. Badly targeted, but still a stimulus for the economy.

- This involves incentivising US companies to bring back cash currently held internationally. In simple terms, US companies can defer tax on international profits by holding the money offshore. Trump is proposing tax incentives to bring this money back. This is a one-off increase in tax revenue, and likely a one-off increase in buybacks and dividends. Both of these are USD bullish. This is a short-termism at its best – sacrifice the future to juice current economic activity.

The playbook (subject to being able to find stocks at the right price) is:

Round 1: Buy US stocks for the sugar hit, plus exporters in non-trade pact countries

The US will go deeper into debt – a good thing for global demand.

This means the end of the rate cycle (although the upswing may not last that long). The US dollar is likely to be strong, and I suspect that the US dollar will offset a lot of the benefit for the US – i.e. US demand increases, but a decent amount of that benefits the rest of the world through increased exports to the US.

In aggregate, this is a buy US equities story, probably go light on US exporters or companies that are import exposed as the US dollar strength is going to hurt them the most. In other markets, try to avoid exporters who will be hit by trade sanctions (Mexico, Canada, China) and look for those that might fly under the radar and benefit from US demand (UK, Europe, maybe even Japan). Increased demand puts a floor under a lot of commodity prices; some will rise.

Keep in mind that some of this is already priced in.

Round 2: Reduced world trade, increased protectionism

Say hello to higher costs in the US. Net/net the average Trump voter will probably give back from a higher currency and increased inflation any gains from (increasingly unlikely) protectionism.

Will a US/China trade war break out or will it just be lots of noise and posturing while in the background the increased US demand benefits the Chinese economy? Hard to tell, but we are leaning towards noise and posturing rather than tangible measures – especially as Trump needs China to help with North Korea. Also, Republicans are generally protrade, and anti-trade measures are less likely to get support.

US companies will struggle with profit growth due to higher costs (with the higher USD), fading stimulus.

Round 3: Unsustainability become apparent

If you don’t believe in trickle down (I don’t) then at some stage the debt becomes unsustainable, and taxes need to be lifted. Hopefully, it’s not too close to the time that the Chinese debt becomes unsustainable… Anyway, that is a future problem – probably 2-3 years away at least, maybe 5 years away, at which time the US is in a worse position than today, the core problem of too much inequality/lack of demand still exists (probably gets worse).

Maybe it is the Euro falling apart, maybe it is another external shock, but the core thesis of a lack of demand largely driven by inequality remains, and in 3-5 years we are back where we started – but with a much higher US debt balance.

So, we should play the boom but keep a sharp eye on the bust.

Tactical Asset Allocation Portfolio Positioning

In our tactical portfolios, we own cash, bonds, international shares and Australian shares.

The broad sweep of our asset allocation over the last 12 months was to ride the Trump Boom, switch into Europe in March / April as the US became overvalued and then switch back into the US as the Euro rallied and the USD fell.

We remain underweight shares in aggregate, but that headline view hides the underlying exposure – we are significantly overweight international equities and significantly underweight Australian.

Over / Underweight positions by portfolio

Source: Nucleus Wealth

We made no changes to the allocation during August, the earlier this month we continued to switch European stocks for US stocks to take advantage of the rally in both the Euro and European stocks.

International Equities

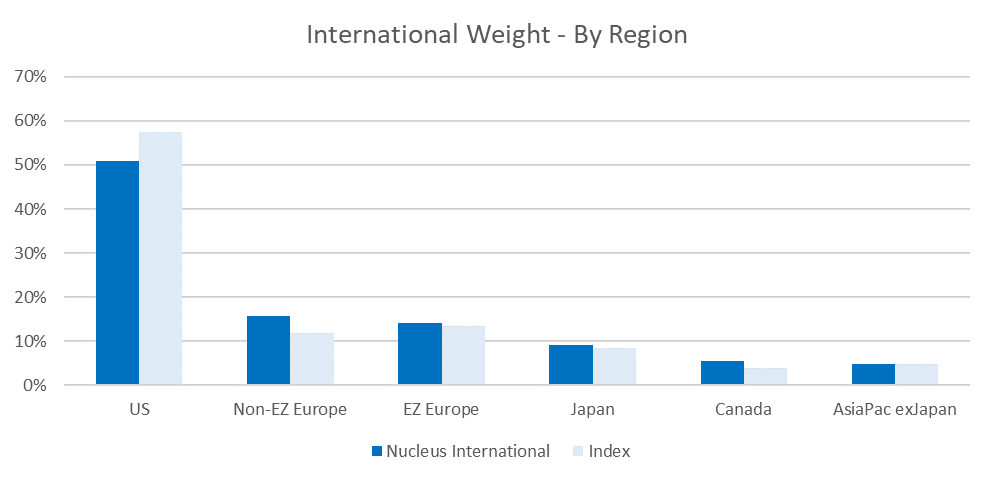

In our direct international portfolio, markets are expensive, returns look low, and risks are building. So, for the most part putting together our international portfolio, it has been about finding novel ways to get the exposure that we want.

REgion Allocation

Based on growth and relative valuations, we are country agnostic at this point, if the USD keeps falling we will be looking to pick up more US stocks – that is the market where the growth remains the highest.

While “technically” we are underweight the US, many of the stocks we own in other markets have significant exposure to the US. Basically, we are finding stocks listed in the US to be relatively expensive, and so we have been looking to other markets to find stocks that are exposed to the US at a cheaper price. For example, Unilever is a UK listed stock, but Unilever’s actual sales exposure to the UK is only a little over 5% – its biggest markets are actually the US and China. Vestas Wind is listed in Denmark, but the US is its biggest market.

We have been hunting for value in non-Euro European markets in particular.

The UK is one of the cheapest markets, burdened by Brexit fears, but we are also finding a number of quality multinationals in markets like Finland or Denmark that look better value than similar stocks listed in the US. We are mainly looking for multinationals rather than domestic stocks.

Some of the names include Unilever (household products), Imperial Brands (tobacco), Kone (Finland listed elevator manufacturer), Roche (Switzerland listed healthcare company) and Vestas Wind (Denmark listed but mainly US sales of wind turbines and parts). Most of these stocks have significant US sales, and trade at lower multiples than equivalent stocks in the US.

Industry Allocation

Defensives are expensive. REITs, Utilities, Telcos and Infrastructure are the usual places to look for defensive exposure but (just as the central banks intend) lower risk investors continue to “shuffle up the risk spectrum”, and they have bid the price of traditional defensive sectors to levels that make investment difficult.

So, again we have positioned the portfolio to benefit differently. We are looking for a mix of the more stable industrial, consumer staples and healthcare stocks to get a similar defensive exposure without having to pay the nosebleed prices in the traditional defensive portfolios. Healthcare was helpful in this regard over the month – a number of our best performers have been in the healthcare sector.

Our biggest call is underweight energy. In particular oil producers. We have blogged a lot about the oil price, (see this post, in particular) but the thumbnail sketch of the sector is that:

- the short term is not positive for the sector with oversupply and OPEC needing to cut production to try to prop up the oil price.

- the long term is not positive with increasing electrification of cars and falling battery prices limiting the upside

- the mid-term might be good if an undersupply emerges and before electric cars put a dent in oil demand and assuming US shale costs don’t keep falling

Meanwhile, oil stocks are pricing $60-$70 oil prices in perpetuity. The mid-term is going to have to be spectacular to justify current share prices, let alone getting any share price growth.

Having said that, it is a big risk to our portfolio being underweight energy. If there are geo-political ructions, particularly in the Middle East, we would probably underperform. September has seen a significant rise in the oil price, but we remain comfortable with our holding and expect much of this to be a short-term issue.

We are underweight financials – mainly as we can’t find US financials that are cheap enough to justify purchasing. We have been trawling the European banks for value.

We have a reasonable tech / IT exposure. Apple isn’t too expensive, but there are growth concerns – Apple was one of our best performers in August but has given most of the gains back in September. Google we can just squeeze into our model as very high quality but expensive.

There are a number of smaller tech stocks that we own, in particular, a range of semiconductor stocks where we like the growth outlook. In particular, its worth noting that part of the reason for Apple increasing the price of its latest phone is an increase in memory and components. This is a positive for semi-conductor stocks more generally, especially if a “feature war” breaks out in the smartphone space. We current hold a range of stocks that should be helped by this trend (Lam, Applied Materials, Skyworks, and to a lesser extent Cisco).

The retail sector in the US was the greatest source of volatility in our portfolio over the month – basically, US retailers fall into one of three camps:

- Retailers that are “Amazon proof”: these are retail businesses that are high touch or heavily service driven – broadly thought to be relatively safe from competition from Amazon (or other on-line sites). They generally trade on relatively expensive multiples, 20-25 times earnings.

- Retailers that are “Amazon exposed”: these are retail businesses with weak or negative sales growth that are losing out to online competitors. They trade at multiples of about half of stocks in the above category.

- Retailers that are Amazon. Amazon is expensive trading on a P/E multiple in the hundreds. The valuation argument is that a typical retailer will make 6% margin, while Amazon makes a 2% margin. However, the expectation is that one day Amazon will stop chasing growth and charge a higher price. If Amazons margins increase to 4%, then Amazon is just really expensive, at 6% margins you can mount an argument (assuming lots of growth) that Amazon is reasonable At $450b in market cap, and with sales growth still above 20% per annum, Amazon is the sector behemoth that everyone is worried about.

We have a few retail stocks in the low P/E category where we believe the downside has been overestimated. The holdings included:

- Signet Jewelers: with the view that many jewellery purchases will need to be done in person

- Footlocker: constantly changing designs will mean that many people will still want to try on athletic shoes

- Michael Kors and Christian Dior: status purchases we suspect are more likely to be made in person.

Footlocker was the biggest detractor (-25%) from our portfolio falling on the back of concerns about online competition from Nike/Adidas. This was counter-balanced by increases in Michael Kors & Christian Dior (up 16% & 10%) and the “there and back again” performance of Signet which fell 15% intramonth but finished up 4% for the month.

(click for full chart)

Australian Shares

Our best performing portfolio for the month was ironically Australia Shares where our weights are the lowest. The Australian market fell in August, but our underweights to resources and banks and our overweights to internationally exposed industrials saw the portfolio up 1.4% vs a market that fell 0.3%.

We are underweight both banks and resources, and given the highly concentrated characteristics of the Australian market, we are overweight just about everything else.

We are only just managing to keep a number of the international stocks in our portfolio – on a valuation basis Treasury Wines, CSL, Cochlear are all getting expensive after performing well in August, and we sold half of our Amcor holding after it rose 5% over the month. We are struggling to find viable replacements.

(click for full chart)

Epilogue

In summary, our view continues to be that Australian investors are better off holding international investments at this point in the cycle.

Our intention is that our portfolio is positioned to take advantage of our key themes but minimise risk in the event that our themes take longer than expected to resolve themselves.

We usually find that big picture macro themes take a long time to resolve themselves in financial markets, but when macro theme resolve themselves they do so quickly – usually too quickly to reposition your portfolio if you are not already invested.

As an example, September month to date has been more friendly to our core themes, and the international portfolio and the growth portfolio have reflected that.

Note that these are indicative performance numbers only on our portfolios and don’t yet include investment fees for the month – official numbers to come out after month end::

International:

Tactical Growth:

Source: Linear Damien Klassen is Head of Investments at Nucleus Wealth. The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.